Das könnte Ihnen auch gefallen

- Salenga v. NLRC GR 174941 February 1, 2012Dokument1 SeiteSalenga v. NLRC GR 174941 February 1, 2012James WilliamNoch keine Bewertungen

- Annulment, Divorce and Legal Separation in The PhilsDokument5 SeitenAnnulment, Divorce and Legal Separation in The PhilsJocelyn HerreraNoch keine Bewertungen

- G.R. No. L-12790Dokument2 SeitenG.R. No. L-12790David Jayson Barcelona OquendoNoch keine Bewertungen

- ME Holding Corp vs. CADokument2 SeitenME Holding Corp vs. CAJeremae Ann CeriacoNoch keine Bewertungen

- Deutsche Bank V CIR DigestDokument2 SeitenDeutsche Bank V CIR DigestJImlan Sahipa IsmaelNoch keine Bewertungen

- TX Cs041119Dokument11 SeitenTX Cs041119Morphues100% (1)

- 3y1s Tax F 1 FullshemDokument38 Seiten3y1s Tax F 1 FullshemWolf DenNoch keine Bewertungen

- Xii. The Constitutional Commissions 2. Civil Service Commissions D. (Ii) Jacinto V Court of AppealsDokument2 SeitenXii. The Constitutional Commissions 2. Civil Service Commissions D. (Ii) Jacinto V Court of AppealsYoo Si JinNoch keine Bewertungen

- Francisco I. Chavez V Jaime B. OngpinDokument2 SeitenFrancisco I. Chavez V Jaime B. OngpinJohn YeungNoch keine Bewertungen

- The Hague Service Convention Judge Myra QuiambaoDokument8 SeitenThe Hague Service Convention Judge Myra QuiambaoAngelineNoch keine Bewertungen

- (Labor 2 - Atty. Nolasco) : G.R. No. 201595, January 25, 2016 Justice Del Castillo Digest By: BERNALDokument2 Seiten(Labor 2 - Atty. Nolasco) : G.R. No. 201595, January 25, 2016 Justice Del Castillo Digest By: BERNALRalph Deric EspirituNoch keine Bewertungen

- 61-Northwest V CADokument15 Seiten61-Northwest V CAJesus Angelo DiosanaNoch keine Bewertungen

- Torts and Damages CasesDokument51 SeitenTorts and Damages Casescrazzy foryou100% (2)

- Municipal Council of Iloilo Vs Evangelista (1930)Dokument1 SeiteMunicipal Council of Iloilo Vs Evangelista (1930)Tin NavarroNoch keine Bewertungen

- 2I2J-Nego CaseDigest TemplateDokument1 Seite2I2J-Nego CaseDigest TemplatekarlNoch keine Bewertungen

- University of The Philippines College of Law: Case Name Topic Case No. - Date PonenteDokument5 SeitenUniversity of The Philippines College of Law: Case Name Topic Case No. - Date PonenteJB GuevarraNoch keine Bewertungen

- Bpi Investment Corporation Vs CADokument2 SeitenBpi Investment Corporation Vs CAJillian AsdalaNoch keine Bewertungen

- #5 Silkair v. Cir (2008) - PelayoDokument2 Seiten#5 Silkair v. Cir (2008) - PelayoJrPelayoNoch keine Bewertungen

- Commissioner of Internal Revenue Vs Central Luzon Drug Corporation GR No 159647Dokument36 SeitenCommissioner of Internal Revenue Vs Central Luzon Drug Corporation GR No 159647Tamara Bianca Chingcuangco Ernacio-TabiosNoch keine Bewertungen

- Philippine Acetylen v. CIRDokument2 SeitenPhilippine Acetylen v. CIRJemima FalinchaoNoch keine Bewertungen

- CIR V AcesiteDokument2 SeitenCIR V AcesiteAleli Joyce BucuNoch keine Bewertungen

- 88 CIR v. Tours Specialists, IncDokument3 Seiten88 CIR v. Tours Specialists, IncGain DeeNoch keine Bewertungen

- Omictin Vs Ca PDFDokument17 SeitenOmictin Vs Ca PDFLarssen IbarraNoch keine Bewertungen

- Pecson v. Ca (Batch 3)Dokument1 SeitePecson v. Ca (Batch 3)Joseph FernandezNoch keine Bewertungen

- VALUE ADDED TAX and EXCISE TAXDokument18 SeitenVALUE ADDED TAX and EXCISE TAXTrisha Nicole Flores0% (1)

- 67 CIR V Procter GambleDokument2 Seiten67 CIR V Procter GambleNaomi QuimpoNoch keine Bewertungen

- Case Digest Statcon3Dokument4 SeitenCase Digest Statcon3dezNoch keine Bewertungen

- H. Taxation Other Inherent To Escape From Taxation CasesDokument36 SeitenH. Taxation Other Inherent To Escape From Taxation CasesErwin April MidsapakNoch keine Bewertungen

- TAX Week 9 DigestsDokument12 SeitenTAX Week 9 Digestskrisipsaloquitur0% (1)

- Negotiable Instruments Reviewer For FinalsDokument10 SeitenNegotiable Instruments Reviewer For FinalsAireen Villahermosa PiniliNoch keine Bewertungen

- Securities Regulations Code ("SRC") - Ra 8799Dokument25 SeitenSecurities Regulations Code ("SRC") - Ra 8799Shiela MarieNoch keine Bewertungen

- Human Relations (Arts. 19-36, NCC) PDFDokument511 SeitenHuman Relations (Arts. 19-36, NCC) PDFYan AringNoch keine Bewertungen

- 212 Scra 448 RGFMDokument2 Seiten212 Scra 448 RGFMRhuejane Gay MaquilingNoch keine Bewertungen

- Tax SparingDokument5 SeitenTax Sparingfrancis_asd2003Noch keine Bewertungen

- 21) ALLIANCE OF QC HOMEOWNERS' Vs QC Government - J. Perlas-BernabeDokument6 Seiten21) ALLIANCE OF QC HOMEOWNERS' Vs QC Government - J. Perlas-BernabeStalin LeningradNoch keine Bewertungen

- 7 Eastern Shipping Lines vs. CA, 234 SCRA 78Dokument21 Seiten7 Eastern Shipping Lines vs. CA, 234 SCRA 78blessaraynesNoch keine Bewertungen

- 250 Philippine Reports Annotated: Conde vs. AbayaDokument8 Seiten250 Philippine Reports Annotated: Conde vs. AbayaKenmar NoganNoch keine Bewertungen

- Tax Review Specific ItemsDokument2 SeitenTax Review Specific ItemsAllana NacinoNoch keine Bewertungen

- Specpro Vs Ordinary Civil ActionDokument2 SeitenSpecpro Vs Ordinary Civil ActionAnthony ReandelarNoch keine Bewertungen

- Corpo Exam 1Dokument14 SeitenCorpo Exam 1Hannah Cris Echavez100% (1)

- Form14-Simple Voting Trust AgreementDokument3 SeitenForm14-Simple Voting Trust Agreementiris galecio100% (1)

- Escheats - Guardianship - AdoptionDokument9 SeitenEscheats - Guardianship - AdoptionIrish AnnNoch keine Bewertungen

- 16 - Villanueva vs. Domingo PDFDokument2 Seiten16 - Villanueva vs. Domingo PDFJm SantosNoch keine Bewertungen

- Republic vs. Hon. Jose R. HernandezDokument3 SeitenRepublic vs. Hon. Jose R. Hernandezmerren bloomNoch keine Bewertungen

- Nego Case Diges1Dokument12 SeitenNego Case Diges1Arnel MangilimanNoch keine Bewertungen

- Corpo Midterm CoverageeeeDokument30 SeitenCorpo Midterm CoverageeeeRedd ClosaNoch keine Bewertungen

- AFP-RSBS vs. RP, G.R. 180086, July 2, 2014Dokument2 SeitenAFP-RSBS vs. RP, G.R. 180086, July 2, 2014Ron Christian EupeñaNoch keine Bewertungen

- 4 CIR v. Gotamco & SonsDokument3 Seiten4 CIR v. Gotamco & SonsMarvic AmazonaNoch keine Bewertungen

- Rojas vs. MaglanaDokument2 SeitenRojas vs. MaglanaFranzMordenoNoch keine Bewertungen

- NPC Vs NamercoDokument5 SeitenNPC Vs NamercoMa. Princess CongzonNoch keine Bewertungen

- (Commissioner of Internal Revenue vs. Pineda, 21 SCRA 105 (1967) ) PDFDokument6 Seiten(Commissioner of Internal Revenue vs. Pineda, 21 SCRA 105 (1967) ) PDFJillian BatacNoch keine Bewertungen

- 76 Crisostomo v. CADokument3 Seiten76 Crisostomo v. CAJul A.Noch keine Bewertungen

- Train Law 2018Dokument55 SeitenTrain Law 2018Mira Mendoza100% (1)

- SURIGAO ELECTRIC vs. CIRDokument3 SeitenSURIGAO ELECTRIC vs. CIRMichelle Jude TinioNoch keine Bewertungen

- CIR v. CTA and PetronDokument15 SeitenCIR v. CTA and PetronJennylyn Biltz AlbanoNoch keine Bewertungen

- Financial Rehabilitation and Insolvency ActDokument6 SeitenFinancial Rehabilitation and Insolvency ActEliyah JhonsonNoch keine Bewertungen

- Judicial Jurisdiction and Forum Non ConviniensDokument3 SeitenJudicial Jurisdiction and Forum Non ConviniensDave OcampoNoch keine Bewertungen

- REMEDIES OF THE TAXPAYER and GOVERNMENTDokument7 SeitenREMEDIES OF THE TAXPAYER and GOVERNMENTChrisMartinNoch keine Bewertungen

- A. Individuals:: 1. Citizens of The PhilippinesDokument5 SeitenA. Individuals:: 1. Citizens of The PhilippinesRaymond FaeldoñaNoch keine Bewertungen

- 2020 Reme TPDokument24 Seiten2020 Reme TPManuel VillanuevaNoch keine Bewertungen

- Sps Mamaril Vs BSP (Obli)Dokument2 SeitenSps Mamaril Vs BSP (Obli)Haze Q.Noch keine Bewertungen

- David Fornilda Vs RTC (1989)Dokument4 SeitenDavid Fornilda Vs RTC (1989)Haze Q.Noch keine Bewertungen

- Beltran Vs PeopleDokument4 SeitenBeltran Vs PeopleHaze Q.Noch keine Bewertungen

- Mea Builders Vs CADokument1 SeiteMea Builders Vs CAHaze Q.Noch keine Bewertungen

- S. Guy Vs Gilbert Guy - Corpo DigestDokument2 SeitenS. Guy Vs Gilbert Guy - Corpo DigestHaze Q.Noch keine Bewertungen

- Guy Vs CAlo FullDokument11 SeitenGuy Vs CAlo FullHaze Q.Noch keine Bewertungen

- Tax 2 Maniego NotesDokument32 SeitenTax 2 Maniego NotesHaze Q.Noch keine Bewertungen

- Penalty For QTDokument2 SeitenPenalty For QTHaze Q.Noch keine Bewertungen

- Weight of EvidenceDokument1 SeiteWeight of EvidenceHaze Q.Noch keine Bewertungen

- 1) Defective Definition of The Contract of Agency: Par., Civil CodeDokument2 Seiten1) Defective Definition of The Contract of Agency: Par., Civil CodeHaze Q.Noch keine Bewertungen

- Opulencia Vs CADokument1 SeiteOpulencia Vs CAHaze Q.Noch keine Bewertungen

- Ultra Vires - BERNAS V CINCODokument6 SeitenUltra Vires - BERNAS V CINCOValiant Aragon DayagbilNoch keine Bewertungen

- 102 Rule 71 Trinidad V Fama RealtyDokument1 Seite102 Rule 71 Trinidad V Fama RealtyHaze Q.Noch keine Bewertungen

- Revised Rules On Summary ProcedureDokument6 SeitenRevised Rules On Summary ProcedureHaze Q.Noch keine Bewertungen

- 101 Rule 71 Ladano Vs NeriDokument5 Seiten101 Rule 71 Ladano Vs NeriHaze Q.Noch keine Bewertungen

- Llorente vs. Rodriguez, Et. Al. G.R. No. L-3339, March 26, 1908Dokument1 SeiteLlorente vs. Rodriguez, Et. Al. G.R. No. L-3339, March 26, 1908Haze Q.Noch keine Bewertungen

- People Vs GAlvezDokument3 SeitenPeople Vs GAlvezHaze Q.Noch keine Bewertungen

- 91 Heirs of Rogelio Isip, Sr. vs. QuintosDokument4 Seiten91 Heirs of Rogelio Isip, Sr. vs. QuintosHaze Q.Noch keine Bewertungen

- Republic Act No. 10951: - Grave Felonies Are Those To Which The Law Attaches The CapitalDokument45 SeitenRepublic Act No. 10951: - Grave Felonies Are Those To Which The Law Attaches The CapitalHaze Q.Noch keine Bewertungen

- PEOPLE OF THE PHILIPPINES, Plaintiff-Appellee, ALEXANDER SACABIN at "ROMEO", DefendantDokument2 SeitenPEOPLE OF THE PHILIPPINES, Plaintiff-Appellee, ALEXANDER SACABIN at "ROMEO", DefendantHaze Q.Noch keine Bewertungen

- Samalio Vs CADokument1 SeiteSamalio Vs CAHaze Q.Noch keine Bewertungen

- Testate Estate of Joseph G. Brimo, JUAN MICIANO, Administrator vs. Andre BrimoDokument12 SeitenTestate Estate of Joseph G. Brimo, JUAN MICIANO, Administrator vs. Andre BrimoHaze Q.Noch keine Bewertungen

- Insurance Week 1Dokument26 SeitenInsurance Week 1Haze Q.Noch keine Bewertungen

- Verifone User Guide: VX 820 and VX 680Dokument32 SeitenVerifone User Guide: VX 820 and VX 680serradajaviNoch keine Bewertungen

- Ebook PDF Canadian Income Taxation 2018 2019 by William Buckwold PDFDokument41 SeitenEbook PDF Canadian Income Taxation 2018 2019 by William Buckwold PDFdaniel.blakenship846100% (42)

- ACCT 3061 Asignación Cap 4 y 5Dokument4 SeitenACCT 3061 Asignación Cap 4 y 5gpm-81Noch keine Bewertungen

- Goods and Services Tax/harmonized Sales Tax Credit (GST/HSTC) NoticeDokument3 SeitenGoods and Services Tax/harmonized Sales Tax Credit (GST/HSTC) NoticeSam StormeNoch keine Bewertungen

- Answer Problem Chapter 6Dokument2 SeitenAnswer Problem Chapter 6Phạm Minh TâmNoch keine Bewertungen

- 3Dokument2 Seiten3Carlo ParasNoch keine Bewertungen

- Double TaxationDokument8 SeitenDouble TaxationArun KumarNoch keine Bewertungen

- Cir vs. Seagate TechnologyDokument1 SeiteCir vs. Seagate Technologygeorge almedaNoch keine Bewertungen

- TR 17 ReverseDokument1 SeiteTR 17 ReverseAbdul Rehman CheemaNoch keine Bewertungen

- Medical InsuranceDokument1 SeiteMedical Insurancesunil dinodiyaNoch keine Bewertungen

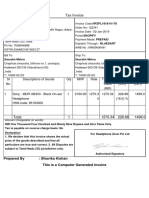

- Tax Invoice: SI No. Descriptions of Goods Qty MRP Rate Taxable Value (INR) Igst (INR) Amount (INR)Dokument1 SeiteTax Invoice: SI No. Descriptions of Goods Qty MRP Rate Taxable Value (INR) Igst (INR) Amount (INR)Saurabh MehraNoch keine Bewertungen

- Order 1649224782857Dokument1 SeiteOrder 1649224782857Deep ChoudharyNoch keine Bewertungen

- Income Taxation: Classification of Individual TaxpayersDokument3 SeitenIncome Taxation: Classification of Individual TaxpayersALMA MORENANoch keine Bewertungen

- E-Way Bill System-22110616-ERODE-DETAILEDDokument1 SeiteE-Way Bill System-22110616-ERODE-DETAILEDvragavhNoch keine Bewertungen

- BOB WorldDokument49 SeitenBOB WorldSanjeev GuptaNoch keine Bewertungen

- Img 20200125 0001 PDFDokument1 SeiteImg 20200125 0001 PDFballav sarkarNoch keine Bewertungen

- Chapter 3Dokument12 SeitenChapter 3HuyNguyễnQuangHuỳnhNoch keine Bewertungen

- Clubbing of IncomeDokument2 SeitenClubbing of IncomeNoopur BhandariNoch keine Bewertungen

- Invoice TVDokument1 SeiteInvoice TVpradip v khandareNoch keine Bewertungen

- CIR v. Manila Jockey ClubDokument2 SeitenCIR v. Manila Jockey ClubKeila Garcia100% (2)

- AltrozDokument1 SeiteAltrozSubhasishNoch keine Bewertungen

- Business Research Methods ReportDokument5 SeitenBusiness Research Methods Reportvijay choudhariNoch keine Bewertungen

- East Penn Anticipated Budget Revenues 2023-2024Dokument14 SeitenEast Penn Anticipated Budget Revenues 2023-2024Jay BradleyNoch keine Bewertungen

- ICGAB New Tax Syllabus (Sep-19)Dokument9 SeitenICGAB New Tax Syllabus (Sep-19)Aminul HaqNoch keine Bewertungen

- Tax Free Exchange v3Dokument2 SeitenTax Free Exchange v3Lara YuloNoch keine Bewertungen

- Rmo 38-83Dokument1 SeiteRmo 38-83saintkarriNoch keine Bewertungen

- Custom Declaration: (Postal Administration)Dokument6 SeitenCustom Declaration: (Postal Administration)Malau JuanNoch keine Bewertungen

- Account Closure/ Fixed Deposit Premature Withdrawal FormDokument1 SeiteAccount Closure/ Fixed Deposit Premature Withdrawal Formrony1346100% (1)

- The Wealth-Tax Act, 1957Dokument16 SeitenThe Wealth-Tax Act, 1957abhishek_ruiaNoch keine Bewertungen

- Wise and Co. Vs MeerDokument3 SeitenWise and Co. Vs MeerNatasha MilitarNoch keine Bewertungen