Das könnte Ihnen auch gefallen

- Understanding DSGE models: Theory and ApplicationsVon EverandUnderstanding DSGE models: Theory and ApplicationsNoch keine Bewertungen

- Business Plan PresentationDokument17 SeitenBusiness Plan Presentationbsmskr0% (1)

- Qns Sec 222Dokument8 SeitenQns Sec 222Haggai SimbayaNoch keine Bewertungen

- # # Macroeconomics Chapter 3Dokument106 Seiten# # Macroeconomics Chapter 3Getaneh ZewuduNoch keine Bewertungen

- Addis Ababa University College of Business and Economics Department of Economics Macroeconomics I (Econ 2031) WorksheetDokument4 SeitenAddis Ababa University College of Business and Economics Department of Economics Macroeconomics I (Econ 2031) WorksheetProveedor Iptv España100% (3)

- Chapter ThreeDokument99 SeitenChapter Threehaile girmaNoch keine Bewertungen

- Unemployment RateDokument11 SeitenUnemployment RateLuis LeeNoch keine Bewertungen

- Chapter Three Aggregate Demand & Aggregate SupplyDokument44 SeitenChapter Three Aggregate Demand & Aggregate SupplyHasbiyallah Weni'imal WakiilNoch keine Bewertungen

- Chapter 3 - Determination of National IncomeDokument54 SeitenChapter 3 - Determination of National IncomeHafizul Akmal100% (4)

- Equity, Efficiency, and The Structure of Indirect Taxation Angus DeatonDokument14 SeitenEquity, Efficiency, and The Structure of Indirect Taxation Angus DeatonGerman RiNoch keine Bewertungen

- Final FileDokument10 SeitenFinal FileMinza JahangirNoch keine Bewertungen

- Unit I-VDokument143 SeitenUnit I-VPrashant KumarNoch keine Bewertungen

- Assignment of Macroeconomics (Summary)Dokument5 SeitenAssignment of Macroeconomics (Summary)Ilham Anugraha PramudityaNoch keine Bewertungen

- Measuring Global Economic ActivityDokument21 SeitenMeasuring Global Economic ActivitysdfghNoch keine Bewertungen

- Monetary Economics Lecture Notes: Ecole Polythechnique - HECDokument84 SeitenMonetary Economics Lecture Notes: Ecole Polythechnique - HECvinarNoch keine Bewertungen

- P T D Δ M P G X D T is real tax revenue, M is money supply, X is transfers. From this structureDokument7 SeitenP T D Δ M P G X D T is real tax revenue, M is money supply, X is transfers. From this structureGökhan DüzüNoch keine Bewertungen

- The Suntory and Toyota International Centres For Economics and Related Disciplines, The London School of Economics and Political Science, Wiley EconomicaDokument16 SeitenThe Suntory and Toyota International Centres For Economics and Related Disciplines, The London School of Economics and Political Science, Wiley EconomicaAdyCastilloNoch keine Bewertungen

- MacroeconomicsDokument19 SeitenMacroeconomicsIlker Sevki InanNoch keine Bewertungen

- 004 Reading2 Carlin Soskice PDFDokument40 Seiten004 Reading2 Carlin Soskice PDFclaudionemeloNoch keine Bewertungen

- 581 ProjDokument11 Seiten581 ProjKeenaLiNoch keine Bewertungen

- The Keynesian ModelDokument13 SeitenThe Keynesian ModelNick GrzebienikNoch keine Bewertungen

- Consumption and Income: Paneleconometric Evidence For West GermanyDokument17 SeitenConsumption and Income: Paneleconometric Evidence For West GermanyMiGz ShiinaNoch keine Bewertungen

- Is and LM ModelDokument36 SeitenIs and LM ModelSyed Ali Zain100% (1)

- Macro WK 9Dokument2 SeitenMacro WK 9Cedric Shi Han SimNoch keine Bewertungen

- Growth Model: Part II: The Growth Model With Taxes and Government ConsumptionDokument4 SeitenGrowth Model: Part II: The Growth Model With Taxes and Government Consumptionz_k_j_vNoch keine Bewertungen

- Review Questions 3 For Advanced Macroeconomics-1Dokument4 SeitenReview Questions 3 For Advanced Macroeconomics-1jared demissieNoch keine Bewertungen

- Macroeconomics 1 Chapter ThreeDokument52 SeitenMacroeconomics 1 Chapter ThreeBiruk YidnekachewNoch keine Bewertungen

- PS01Dokument4 SeitenPS01Manooch GholmoradiNoch keine Bewertungen

- Vamvoukas 1997Dokument11 SeitenVamvoukas 1997wa.hamza88Noch keine Bewertungen

- Final Exam MACRO Jan 21 2019Dokument4 SeitenFinal Exam MACRO Jan 21 2019benrjebfatma18Noch keine Bewertungen

- M. A. (Economics) Part-I Paper Ii Semester-Ii Macroeconomic Analysis Lesson No. 2.2 Author: Dr. ManishaDokument31 SeitenM. A. (Economics) Part-I Paper Ii Semester-Ii Macroeconomic Analysis Lesson No. 2.2 Author: Dr. ManishaM31 Lubna AslamNoch keine Bewertungen

- Why Is Indonesia A High Inflation Country?: - Real and Monetary FactorsDokument17 SeitenWhy Is Indonesia A High Inflation Country?: - Real and Monetary FactorseviewsNoch keine Bewertungen

- Discussion Paper Series: Combining Microsimulation and Optimization To Identify Optimal Flexible Tax-Transfer RulesDokument39 SeitenDiscussion Paper Series: Combining Microsimulation and Optimization To Identify Optimal Flexible Tax-Transfer RulesgotoxicNoch keine Bewertungen

- Chapter 4 Open Economic SystemDokument65 SeitenChapter 4 Open Economic Systemtigabuyeshiber034Noch keine Bewertungen

- Tugas 03 - Kunci JawabanDokument5 SeitenTugas 03 - Kunci JawabanMantraDebosaNoch keine Bewertungen

- Chapter 9Dokument18 SeitenChapter 9Karen ReasonNoch keine Bewertungen

- Poly MacroMass N2Dokument10 SeitenPoly MacroMass N2simao_sabrosa7794Noch keine Bewertungen

- Ec 201 Assignment Sem 2 2019Dokument5 SeitenEc 201 Assignment Sem 2 2019musuotaNoch keine Bewertungen

- Anexo 2 - C4 - David RicardoDokument4 SeitenAnexo 2 - C4 - David RicardoHeller Paternina HernándezNoch keine Bewertungen

- ChapterDokument42 SeitenChapterIf'idatur rosyidahNoch keine Bewertungen

- Module 3 Aggregate Exp SKMDokument78 SeitenModule 3 Aggregate Exp SKMVrinda RajoriaNoch keine Bewertungen

- Seigniorage and The Welfare Cost of Inflation in Colombia: Martha LópezDokument16 SeitenSeigniorage and The Welfare Cost of Inflation in Colombia: Martha LópezNurita HtgNoch keine Bewertungen

- MacroeconomicsDokument38 SeitenMacroeconomicselinevere17Noch keine Bewertungen

- National Income Determination in Four Sector EconomyDokument32 SeitenNational Income Determination in Four Sector Economyutsav100% (1)

- Problem Set - 2015 MACRODokument3 SeitenProblem Set - 2015 MACRODuge GaltsaNoch keine Bewertungen

- Chapter Three Aggregate DemandDokument19 SeitenChapter Three Aggregate DemandLee HailuNoch keine Bewertungen

- ConsumDokument25 SeitenConsumalemu ayeneNoch keine Bewertungen

- Macroeconomics 20181220 180426275Dokument4 SeitenMacroeconomics 20181220 180426275Honelign ZenebeNoch keine Bewertungen

- Permanent and Transitory Components of European Business CycleDokument17 SeitenPermanent and Transitory Components of European Business CycleDeborah KimNoch keine Bewertungen

- SELECTED PROBLEMS AND SOLUTIONS For Economics GrowthDokument21 SeitenSELECTED PROBLEMS AND SOLUTIONS For Economics GrowthDarrelNoch keine Bewertungen

- Applied Economics Letters: Please Scroll Down For ArticleDokument9 SeitenApplied Economics Letters: Please Scroll Down For ArticleLarissa Hashimoto MartinsNoch keine Bewertungen

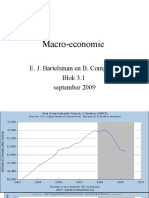

- Macro-Economie: E. J. Bartelsman en B. Compaijen Blok 3.1 September 2009Dokument40 SeitenMacro-Economie: E. J. Bartelsman en B. Compaijen Blok 3.1 September 2009Ravinder_Noch keine Bewertungen

- C OnsumsiDokument45 SeitenC OnsumsiDwiMariaUlfahNoch keine Bewertungen

- Real Financial Interaction: Integrating Supply Side Wage-Price Dynamics and The Stock MarketDokument24 SeitenReal Financial Interaction: Integrating Supply Side Wage-Price Dynamics and The Stock MarketrrrrrrrrNoch keine Bewertungen

- 1 ModelsDokument30 Seiten1 Modelssara alshNoch keine Bewertungen

- Fei2123PS4 PDFDokument4 SeitenFei2123PS4 PDFMarco ChanNoch keine Bewertungen

- Revised Supplementary Material Semester 2 2013Dokument98 SeitenRevised Supplementary Material Semester 2 2013HeoHamHốNoch keine Bewertungen

- ps2 2021 SolutionsDokument5 Seitenps2 2021 SolutionsALBA RUS HIDALGONoch keine Bewertungen

- PQ 3Dokument3 SeitenPQ 3tony345Noch keine Bewertungen

- Kynes Multiplier1Dokument22 SeitenKynes Multiplier1the superstarNoch keine Bewertungen

- Your Personal Flower PDFDokument1 SeiteYour Personal Flower PDFAisyah Fahma ArdianaNoch keine Bewertungen

- Your Personal Flower PDFDokument1 SeiteYour Personal Flower PDFAisyah Fahma ArdianaNoch keine Bewertungen

- Naïve Bayes + Neural NetworkDokument10 SeitenNaïve Bayes + Neural NetworkAisyah Fahma ArdianaNoch keine Bewertungen

- Compile DataDokument3 SeitenCompile DataAisyah Fahma ArdianaNoch keine Bewertungen

- Long Name Special Not 2-Alpha Cod WB-2 Code Table Name Short NameDokument3 SeitenLong Name Special Not 2-Alpha Cod WB-2 Code Table Name Short NameAisyah Fahma ArdianaNoch keine Bewertungen

- pc1 Resuelta PDFDokument15 Seitenpc1 Resuelta PDFWilliam Vasquez SanchezNoch keine Bewertungen

- ECO2101 Microeconomics CA1 Individual Report: Running Head: MICROECONOMICDokument14 SeitenECO2101 Microeconomics CA1 Individual Report: Running Head: MICROECONOMICSwarnali Dutta ChatterjeeNoch keine Bewertungen

- Someone Said Comparing Real and Nominal GDPDokument6 SeitenSomeone Said Comparing Real and Nominal GDPbachir awaydaNoch keine Bewertungen

- Marginal & Differential CostingDokument11 SeitenMarginal & Differential CostingShahenaNoch keine Bewertungen

- Advantages of Branch BankingDokument2 SeitenAdvantages of Branch BankingAnand Shankar RajaNoch keine Bewertungen

- What Is Corporate Restructuring?: Any Change in A Company's:,, or That Is Outside Its Ordinary Course of BusinessDokument22 SeitenWhat Is Corporate Restructuring?: Any Change in A Company's:,, or That Is Outside Its Ordinary Course of BusinessRidhima SharmaNoch keine Bewertungen

- Ch. Charan Singh University Meerut: Regular & Self-Financed CoursesDokument88 SeitenCh. Charan Singh University Meerut: Regular & Self-Financed CoursesAmit KumarNoch keine Bewertungen

- Essay About GlobalizationDokument5 SeitenEssay About GlobalizationJackelin Salguedo FernandezNoch keine Bewertungen

- Qus 303 Construction EconomicsDokument21 SeitenQus 303 Construction Economicsjudexnams1on1Noch keine Bewertungen

- ECOXII201920Dokument70 SeitenECOXII201920Payal SinghNoch keine Bewertungen

- ECON 203 Midterm 2012W AncaAlecsandru SolutionDokument8 SeitenECON 203 Midterm 2012W AncaAlecsandru SolutionexamkillerNoch keine Bewertungen

- Literature Study-Transportation CostDokument22 SeitenLiterature Study-Transportation CostsulthanhakimNoch keine Bewertungen

- 831 2Dokument18 Seiten831 2Ayesha AishNoch keine Bewertungen

- Barth & Sen On Freedom!Dokument29 SeitenBarth & Sen On Freedom!Ryan HayesNoch keine Bewertungen

- Practitioner's Guide To Cost of Capital & WACC Calculation: EY Switzerland Valuation Best PracticeDokument25 SeitenPractitioner's Guide To Cost of Capital & WACC Calculation: EY Switzerland Valuation Best PracticeМаксим ЧернышевNoch keine Bewertungen

- Quiz 3 - Answers PDFDokument2 SeitenQuiz 3 - Answers PDFShiying ZhangNoch keine Bewertungen

- Chapter 5 Summary - Catharina ChrisidaputriDokument3 SeitenChapter 5 Summary - Catharina ChrisidaputriCatharina CBNoch keine Bewertungen

- Demand Supply and Market EquilibriumDokument74 SeitenDemand Supply and Market EquilibriumWilliam Kano100% (2)

- The IMF and The World Bank How Do They Differ?: David D. DriscollDokument15 SeitenThe IMF and The World Bank How Do They Differ?: David D. DriscollNeil NeilsonNoch keine Bewertungen

- Mutually Exclusive AlternativesDokument1 SeiteMutually Exclusive AlternativesAnonymous eaqtQbmNoch keine Bewertungen

- KMBN Mk02: UNIT 1-Marketing Analytics: Meaning and CharacteristicsDokument9 SeitenKMBN Mk02: UNIT 1-Marketing Analytics: Meaning and CharacteristicsSudhanshu SinghNoch keine Bewertungen

- CHPT 12-1 2019 PDFDokument9 SeitenCHPT 12-1 2019 PDFOctavio HerreraNoch keine Bewertungen

- The Recovery of Nehru EraDokument12 SeitenThe Recovery of Nehru EratanyaNoch keine Bewertungen

- International Corporate Finance Solution ManualDokument44 SeitenInternational Corporate Finance Solution ManualPetraNoch keine Bewertungen

- Chapter 10 Capital-Budgeting Techniques and Practice: Foundations of Finance, 9e (Keown/Martin/Petty)Dokument4 SeitenChapter 10 Capital-Budgeting Techniques and Practice: Foundations of Finance, 9e (Keown/Martin/Petty)Meghna CmNoch keine Bewertungen

- The Eco-Toursim Value of A National Park A Case From The PhilippinesDokument32 SeitenThe Eco-Toursim Value of A National Park A Case From The PhilippinesIsmael CortezNoch keine Bewertungen

- Chapter 1 - Introduction To Economic TheoryDokument7 SeitenChapter 1 - Introduction To Economic TheoryKate AlvarezNoch keine Bewertungen

- CRM Project Pramila Final 1Dokument81 SeitenCRM Project Pramila Final 1Anonymous r9cNvGymNoch keine Bewertungen

- Capacitated Plant Location ModelDokument12 SeitenCapacitated Plant Location ModelManu Kaushik0% (1)