Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- List of DeseasesDokument1 SeiteList of DeseasesMohammed MushtahaNoch keine Bewertungen

- GDP Per Capita Per Turkish ProvinceDokument2 SeitenGDP Per Capita Per Turkish ProvinceMohammed MushtahaNoch keine Bewertungen

- Battery NiCad Vs VRLADokument3 SeitenBattery NiCad Vs VRLAdaniel_silabanNoch keine Bewertungen

- Software Implementation of The Duval TriangleDokument5 SeitenSoftware Implementation of The Duval TriangleMohammed MushtahaNoch keine Bewertungen

- Transformer Oil PurificationDokument7 SeitenTransformer Oil PurificationAther AliNoch keine Bewertungen

- CMRP Candidate Guide For Certification and Recertification 10-25-16Dokument42 SeitenCMRP Candidate Guide For Certification and Recertification 10-25-16Mohammed MushtahaNoch keine Bewertungen

- Developer Android Com 4Dokument3 SeitenDeveloper Android Com 4Mohammed MushtahaNoch keine Bewertungen

- ADokument18 SeitenAMohammed MushtahaNoch keine Bewertungen

- 400v StandardDokument8 Seiten400v StandardboltgingerkoppyNoch keine Bewertungen

- Android Custom Navigation DrawerDokument36 SeitenAndroid Custom Navigation DrawerMohammed MushtahaNoch keine Bewertungen

- Battery TypesDokument9 SeitenBattery TypesMohammed MushtahaNoch keine Bewertungen

- Bs en 60085-2004 电气绝缘 耐热性分类Dokument12 SeitenBs en 60085-2004 电气绝缘 耐热性分类Mohammed Mushtaha100% (1)

- BUS Ele Tech Lib Circuit Breakers Instantaneous Trip RegionDokument5 SeitenBUS Ele Tech Lib Circuit Breakers Instantaneous Trip RegionBrenda Naranjo MorenoNoch keine Bewertungen

- Engineer's Guide To Selective CoordinationDokument24 SeitenEngineer's Guide To Selective CoordinationintoisrNoch keine Bewertungen

- CP SB1 Switch Box: Accessory To CPC 100Dokument2 SeitenCP SB1 Switch Box: Accessory To CPC 100Mohammed MushtahaNoch keine Bewertungen

- Exam2 s12 Solutions PhysicsDokument11 SeitenExam2 s12 Solutions PhysicsMohammed MushtahaNoch keine Bewertungen

- Calculus I - Final AnswerDokument2 SeitenCalculus I - Final AnswerMohammed MushtahaNoch keine Bewertungen

- TF3080 RefDokument7 SeitenTF3080 RefJavierNoch keine Bewertungen

- Secure Microcontroller For Smart Cards AT90SC 4818RT: FeaturesDokument3 SeitenSecure Microcontroller For Smart Cards AT90SC 4818RT: FeaturesMohammed MushtahaNoch keine Bewertungen

- Stm32f4 Discovery - Tbi TH LTNCBDokument3 SeitenStm32f4 Discovery - Tbi TH LTNCBJoseph KimNoch keine Bewertungen

- CEE InfoDokument8 SeitenCEE InfoMohammed MushtahaNoch keine Bewertungen

- Microcontroller Based Single Phase Digital Prepaid Energy Meter For Improved Metering and Billing SystemDokument9 SeitenMicrocontroller Based Single Phase Digital Prepaid Energy Meter For Improved Metering and Billing SystemVennilaNoch keine Bewertungen

- PM0081 Programming Manual: STM32F40xxx and STM32F41xxx Flash Programming ManualDokument27 SeitenPM0081 Programming Manual: STM32F40xxx and STM32F41xxx Flash Programming ManualMohammed MushtahaNoch keine Bewertungen

- Roadmap To Your Graduation: Mechanical Engineering ProgramDokument1 SeiteRoadmap To Your Graduation: Mechanical Engineering ProgramMohammed MushtahaNoch keine Bewertungen

- LIS302DL MEMS AccelerometerDokument42 SeitenLIS302DL MEMS AccelerometerMohammed Mushtaha100% (1)

- Jeas 0710 362Dokument14 SeitenJeas 0710 362Mohammed MushtahaNoch keine Bewertungen

- LIS302DL MEMS AccelerometerDokument42 SeitenLIS302DL MEMS AccelerometerMohammed Mushtaha100% (1)

- Smart Card Communication Using PIC Mcus: Author: Abhay Deshmukh Microchip Technology IncDokument18 SeitenSmart Card Communication Using PIC Mcus: Author: Abhay Deshmukh Microchip Technology IncJunim LeNoch keine Bewertungen

- Artificial Bee Colony AlgorithmDokument32 SeitenArtificial Bee Colony AlgorithmrajmehaNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Design and Implemention of Computerized Hotel Management SystemDokument21 SeitenDesign and Implemention of Computerized Hotel Management SystemSamuel AdeyemiNoch keine Bewertungen

- Report of The Committee Constituted To Review The List of Major and Minor Heads of Accounts (LMMHA) of Union and StatesDokument74 SeitenReport of The Committee Constituted To Review The List of Major and Minor Heads of Accounts (LMMHA) of Union and Statesmanish sukhijaNoch keine Bewertungen

- Responsibility Centres: Nature of Responsibility CentersDokument13 SeitenResponsibility Centres: Nature of Responsibility Centersmahesh19689Noch keine Bewertungen

- 1 - FINANCE - ACS2021-FSD-FIN-0025 - 2022 Budget Tabling Presentation - ENDokument25 Seiten1 - FINANCE - ACS2021-FSD-FIN-0025 - 2022 Budget Tabling Presentation - ENJon WillingNoch keine Bewertungen

- Public Sector Accounting Tutorial (Ain)Dokument2 SeitenPublic Sector Accounting Tutorial (Ain)Ain FatihahNoch keine Bewertungen

- Role of Government in Economic PolicyDokument22 SeitenRole of Government in Economic PolicyMiss PauNoch keine Bewertungen

- UNION BUDGET 2023 - Graphs, Trends & Detailed AnalysisDokument16 SeitenUNION BUDGET 2023 - Graphs, Trends & Detailed AnalysisappuNoch keine Bewertungen

- Planning: IMSE-3 Year 2015 Dr. Abdulghani Al-NakeebDokument59 SeitenPlanning: IMSE-3 Year 2015 Dr. Abdulghani Al-NakeebTahaNoch keine Bewertungen

- Revision Module 6Dokument7 SeitenRevision Module 6avineshNoch keine Bewertungen

- Lawyers Against Monopoly and Poverty Vs Sec of DBM G.R. No. 164987Dokument15 SeitenLawyers Against Monopoly and Poverty Vs Sec of DBM G.R. No. 164987Charmaine Valientes CayabanNoch keine Bewertungen

- 1.introduction Financial AdministrationDokument19 Seiten1.introduction Financial AdministrationshanaaNoch keine Bewertungen

- 12.2 Marketing Information Systems (Figure 12.2 & Figure 12.3)Dokument7 Seiten12.2 Marketing Information Systems (Figure 12.2 & Figure 12.3)Premendra SahuNoch keine Bewertungen

- Accounting For Governmental & Nonprofit Entities: Jacqueline L. Reck Suzanne L. LowensohnDokument27 SeitenAccounting For Governmental & Nonprofit Entities: Jacqueline L. Reck Suzanne L. LowensohnRoite BeteroNoch keine Bewertungen

- Lesson 4 HND in Business Unit 5 Management AccountingDokument32 SeitenLesson 4 HND in Business Unit 5 Management AccountingShan Wikoon LLB LLM90% (10)

- PS With Defined Fields For WBS ElementsDokument14 SeitenPS With Defined Fields For WBS ElementsDon DonNoch keine Bewertungen

- Economic and Political Weekly Economic and Political WeeklyDokument10 SeitenEconomic and Political Weekly Economic and Political WeeklyMig TigNoch keine Bewertungen

- Government BudgetDokument13 SeitenGovernment BudgetsarikaNoch keine Bewertungen

- Chapter 1 Overview of Government AccountingDokument4 SeitenChapter 1 Overview of Government AccountingSteffany Roque100% (1)

- Sukhvinder SinghDokument2 SeitenSukhvinder SinghBhavesh PopatNoch keine Bewertungen

- Intosai PDFDokument21 SeitenIntosai PDFsukandeNoch keine Bewertungen

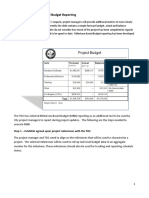

- Guide To Milestone Based Budget ReportingDokument4 SeitenGuide To Milestone Based Budget ReportingRiz DeenNoch keine Bewertungen

- Daily RoutineDokument82 SeitenDaily RoutineKailash Chandra PradhanNoch keine Bewertungen

- Kerala Budget Manual Preparation of Budget Part I and II - Revised EstimatesDokument17 SeitenKerala Budget Manual Preparation of Budget Part I and II - Revised EstimatesSmitha SreehariNoch keine Bewertungen

- 1.office of The MayorDokument29 Seiten1.office of The MayorVIRGILIO OCOY IIINoch keine Bewertungen

- Martin Packing Company Case AnalysisDokument2 SeitenMartin Packing Company Case AnalysisShambhawi SinhaNoch keine Bewertungen

- Finance Director CV TemplateDokument2 SeitenFinance Director CV TemplatesarmaelectricalNoch keine Bewertungen

- Chap 17Dokument34 SeitenChap 17ridaNoch keine Bewertungen

- Standard Cost and Components and Variance AnalysisDokument7 SeitenStandard Cost and Components and Variance AnalysisNaveen RajputNoch keine Bewertungen

- Financial Planning Tools and Concepts - and andDokument25 SeitenFinancial Planning Tools and Concepts - and andChristian ZebuaNoch keine Bewertungen

- Maths Project: Planning A Home BudgetDokument10 SeitenMaths Project: Planning A Home BudgetFaiz100% (8)