Das könnte Ihnen auch gefallen

- Tax Particulars National Internal Revenue Code of 1997 R. A. No. 10963Dokument4 SeitenTax Particulars National Internal Revenue Code of 1997 R. A. No. 10963blackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 12, 14, 16, 17Dokument4 SeitenTRAIN (Changes) ???? Pages 12, 14, 16, 17blackmail1Noch keine Bewertungen

- Tax Particulars National Internal Revenue Code of 1997 R. A. No. 10963Dokument5 SeitenTax Particulars National Internal Revenue Code of 1997 R. A. No. 10963blackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 11, 13, 14Dokument3 SeitenTRAIN (Changes) ???? Pages 11, 13, 14blackmail1Noch keine Bewertungen

- Value Added Tax 3Dokument8 SeitenValue Added Tax 3Nerish PlazaNoch keine Bewertungen

- 1) 7.22.19 VAT DiscussionsDokument30 Seiten1) 7.22.19 VAT DiscussionsJanarie Bosco OrofilNoch keine Bewertungen

- PH Tax in A Dot Implementing Rules Regulations Train Law 21mar2018 PDFDokument6 SeitenPH Tax in A Dot Implementing Rules Regulations Train Law 21mar2018 PDFWilmar AbriolNoch keine Bewertungen

- RR No. 13-2018 (VAT Refund)Dokument23 SeitenRR No. 13-2018 (VAT Refund)Hailin QuintosNoch keine Bewertungen

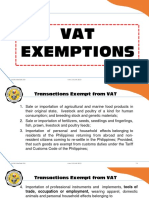

- 4 VAT ExemptionsDokument28 Seiten4 VAT ExemptionsMobile LegendsNoch keine Bewertungen

- Value Added TaxDokument13 SeitenValue Added TaxRyan AgcaoiliNoch keine Bewertungen

- Estate Tax Returns: Tax Particulars National Internal Revenue Code of 1997 R. A. No. 10963Dokument5 SeitenEstate Tax Returns: Tax Particulars National Internal Revenue Code of 1997 R. A. No. 10963blackmail1Noch keine Bewertungen

- Bir Train Vat 20180418Dokument54 SeitenBir Train Vat 20180418DanaNoch keine Bewertungen

- Zero-Rated Sales PDFDokument24 SeitenZero-Rated Sales PDFNEstandaNoch keine Bewertungen

- CIR V BurmeisterDokument3 SeitenCIR V BurmeisterGenevieve Kristine Manalac100% (1)

- TRAIN (Changes) ???? Pages 2, 5 - 7Dokument4 SeitenTRAIN (Changes) ???? Pages 2, 5 - 7blackmail1Noch keine Bewertungen

- Revenue Regulations No. 13-18: CD Technologies Asia, Inc. © 2019Dokument17 SeitenRevenue Regulations No. 13-18: CD Technologies Asia, Inc. © 2019Lance MorilloNoch keine Bewertungen

- RR 13-2018Dokument20 SeitenRR 13-2018Nikka Bianca Remulla-IcallaNoch keine Bewertungen

- 4 Cir V BurmeisterDokument4 Seiten4 Cir V BurmeisterRamon EldonoNoch keine Bewertungen

- 94-12 OPT - HandoutDokument14 Seiten94-12 OPT - HandoutMj BauaNoch keine Bewertungen

- Business Taxes: Certified Accounting Technician NIAT Office 2015Dokument33 SeitenBusiness Taxes: Certified Accounting Technician NIAT Office 2015Anonymous Lz2qH7Noch keine Bewertungen

- VatDokument7 SeitenVatCharla SuanNoch keine Bewertungen

- Value Added TaxDokument14 SeitenValue Added TaxWyndell AlajenoNoch keine Bewertungen

- Vat HandoutsDokument7 SeitenVat HandoutsjulsNoch keine Bewertungen

- DomondonDokument40 SeitenDomondonCharles TamNoch keine Bewertungen

- VAT Group 3Dokument39 SeitenVAT Group 3Andrea GranilNoch keine Bewertungen

- Other Percentage TaxesDokument11 SeitenOther Percentage TaxesmavslastimozaNoch keine Bewertungen

- RR No. 13-2018 CorrectedDokument20 SeitenRR No. 13-2018 CorrectedRap BaguioNoch keine Bewertungen

- PT, Excise and DST NotesDokument10 SeitenPT, Excise and DST NotesFayie De LunaNoch keine Bewertungen

- Other Percentage Taxes ("Opt") : 1) Section 116: Tax On Persons Exempt From VATDokument14 SeitenOther Percentage Taxes ("Opt") : 1) Section 116: Tax On Persons Exempt From VATJana Trina LibatiqueNoch keine Bewertungen

- Vat With TrainDokument16 SeitenVat With TrainElla QuiNoch keine Bewertungen

- BUSTAXADokument9 SeitenBUSTAXATitania ErzaNoch keine Bewertungen

- Vat Exempt Transactions Under TRAIN LawDokument12 SeitenVat Exempt Transactions Under TRAIN LawSamantha TayoneNoch keine Bewertungen

- Digest RR 13-2018Dokument9 SeitenDigest RR 13-2018Maria Rose Ann BacilloteNoch keine Bewertungen

- Cases in Taxation 2Dokument145 SeitenCases in Taxation 2MACNoch keine Bewertungen

- Tax 2 ReviewerDokument21 SeitenTax 2 ReviewerLouis MalaybalayNoch keine Bewertungen

- CIR v. American Express International G.R. No. 152609, June 29, 2005Dokument2 SeitenCIR v. American Express International G.R. No. 152609, June 29, 2005Susannie AcainNoch keine Bewertungen

- Export Sale of Goods (Sec. 106 (A) (2) (B) ) : Effectively Zero-Rated SalesDokument13 SeitenExport Sale of Goods (Sec. 106 (A) (2) (B) ) : Effectively Zero-Rated SalesTricia Rozl PimentelNoch keine Bewertungen

- Cabria Cpa Review Center: Tel. Nos. (043) 980-6659Dokument12 SeitenCabria Cpa Review Center: Tel. Nos. (043) 980-6659MaeNoch keine Bewertungen

- Tax Feb 17Dokument103 SeitenTax Feb 17Lolit CarlosNoch keine Bewertungen

- Chapter 8 - TaxationDokument20 SeitenChapter 8 - TaxationKaila Mae Tan DuNoch keine Bewertungen

- Reviewer BTTDokument14 SeitenReviewer BTTAlthea Frances VasalloNoch keine Bewertungen

- Title VDokument5 SeitenTitle VErica Mae GuzmanNoch keine Bewertungen

- Mid-Term-Day 1-Other Percentage Taxes (Opt)Dokument52 SeitenMid-Term-Day 1-Other Percentage Taxes (Opt)Christine Joyce MagoteNoch keine Bewertungen

- OPT - HandoutDokument16 SeitenOPT - HandoutGrant Kenneth D. FloresNoch keine Bewertungen

- Part 4Dokument17 SeitenPart 4Marc Lester Hernandez-Sta AnaNoch keine Bewertungen

- Business TaxationDokument33 SeitenBusiness Taxationrose querubinNoch keine Bewertungen

- Module Part 2 - Business Taxation Dec. 14Dokument60 SeitenModule Part 2 - Business Taxation Dec. 14Maybelyn PaalaNoch keine Bewertungen

- RMC 42-99 VAT On OECFDokument4 SeitenRMC 42-99 VAT On OECFLeizlyn Ann De OcampoNoch keine Bewertungen

- Value Added TaxDokument13 SeitenValue Added TaxKatrina FregillanaNoch keine Bewertungen

- Type Who / What Are Subject RA TE TAX Basis Additional NotesDokument7 SeitenType Who / What Are Subject RA TE TAX Basis Additional NotesSavage KongNoch keine Bewertungen

- Async 2022 VAT UPDATEDokument8 SeitenAsync 2022 VAT UPDATEBogs QuitainNoch keine Bewertungen

- Tax Revalida NotesDokument36 SeitenTax Revalida NotesRehina DaligdigNoch keine Bewertungen

- Feb 23 Class VATDokument58 SeitenFeb 23 Class VATybun100% (1)

- Material 9 OPTDokument14 SeitenMaterial 9 OPTnodnel salonNoch keine Bewertungen

- Percentage TaxDokument7 SeitenPercentage TaxArielle CabritoNoch keine Bewertungen

- Tax Booklet As of 10 November 2016Dokument20 SeitenTax Booklet As of 10 November 2016Trixy ComiaNoch keine Bewertungen

- Rmo 19-2007Dokument22 SeitenRmo 19-2007ACVGNoch keine Bewertungen

- Unknown Pages 8 - 10Dokument3 SeitenUnknown Pages 8 - 10blackmail1Noch keine Bewertungen

- Unknown Pages 2 - 4Dokument3 SeitenUnknown Pages 2 - 4blackmail1Noch keine Bewertungen

- Unknown Pages 7 - 9Dokument3 SeitenUnknown Pages 7 - 9blackmail1Noch keine Bewertungen

- Unknown Pages 6 - 8Dokument3 SeitenUnknown Pages 6 - 8blackmail1Noch keine Bewertungen

- Version of The Prosecution: Decision - 3 - G.R. No. 231989Dokument3 SeitenVersion of The Prosecution: Decision - 3 - G.R. No. 231989blackmail1Noch keine Bewertungen

- Unknown Pages 1 - 3Dokument3 SeitenUnknown Pages 1 - 3blackmail1Noch keine Bewertungen

- Unknown Pages 5 - 7Dokument3 SeitenUnknown Pages 5 - 7blackmail1Noch keine Bewertungen

- Decision - 4 - G.R. No. 231989Dokument3 SeitenDecision - 4 - G.R. No. 231989blackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 1, 8, 9, 16 PDFDokument4 SeitenTRAIN (Changes) ???? Pages 1, 8, 9, 16 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 4, 8, 12, 16 PDFDokument4 SeitenTRAIN (Changes) ???? Pages 4, 8, 12, 16 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFDokument5 SeitenTRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFDokument5 SeitenTRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 7, 15, 19 PDFDokument3 SeitenTRAIN (Changes) ???? Pages 7, 15, 19 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 7, 15, 19 PDFDokument3 SeitenTRAIN (Changes) ???? Pages 7, 15, 19 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 2, 3, 14, 15 PDFDokument4 SeitenTRAIN (Changes) ???? Pages 2, 3, 14, 15 PDFblackmail1Noch keine Bewertungen

- Affidavit of Undertaking PDFDokument1 SeiteAffidavit of Undertaking PDFblackmail1Noch keine Bewertungen

- Merged Intellectual Property Syllabus With Cases ? Pages 1 - 15 Pages 2, 3, 7 PDFDokument3 SeitenMerged Intellectual Property Syllabus With Cases ? Pages 1 - 15 Pages 2, 3, 7 PDFblackmail1Noch keine Bewertungen

- How To Replace A Pen Sac PDFDokument11 SeitenHow To Replace A Pen Sac PDFblackmail1Noch keine Bewertungen

- Merged Intellectual Property Syllabus With Cases ? Pages 15 - 17 PDFDokument3 SeitenMerged Intellectual Property Syllabus With Cases ? Pages 15 - 17 PDFblackmail1Noch keine Bewertungen

- Merged Intellectual Property Syllabus With Cases ? Pages 1 - 15 Pages 3, 4 PDFDokument2 SeitenMerged Intellectual Property Syllabus With Cases ? Pages 1 - 15 Pages 3, 4 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 14, 17 - 20, 24 PDFDokument6 SeitenTRAIN (Changes) ???? Pages 14, 17 - 20, 24 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 15, 17 - 20, 22, 24 PDFDokument7 SeitenTRAIN (Changes) ???? Pages 15, 17 - 20, 22, 24 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 15, 18 - 20, 22 PDFDokument5 SeitenTRAIN (Changes) ???? Pages 15, 18 - 20, 22 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 14, 17, 18, 20, 23, 24 PDFDokument6 SeitenTRAIN (Changes) ???? Pages 14, 17, 18, 20, 23, 24 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 13 - 17, 19 PDFDokument6 SeitenTRAIN (Changes) ???? Pages 13 - 17, 19 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 14, 16 - 20 PDFDokument6 SeitenTRAIN (Changes) ???? Pages 14, 16 - 20 PDFblackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 14, 17, 20, 21, 23, 24 PDFDokument6 SeitenTRAIN (Changes) ???? Pages 14, 17, 20, 21, 23, 24 PDFblackmail1Noch keine Bewertungen

- Tax Particulars National Internal Revenue Code of 1997 R. A. No. 10963Dokument8 SeitenTax Particulars National Internal Revenue Code of 1997 R. A. No. 10963blackmail1Noch keine Bewertungen

- TRAIN (Changes) ???? Pages 13, 15 - 21, 23 PDFDokument9 SeitenTRAIN (Changes) ???? Pages 13, 15 - 21, 23 PDFblackmail1Noch keine Bewertungen

- Summary Corporation Law Pages 2 - 4, 6 - 8 PDFDokument6 SeitenSummary Corporation Law Pages 2 - 4, 6 - 8 PDFblackmail1Noch keine Bewertungen

- Teel Industrial Series Water Circulating Pumps Operating Instructions and Parts ManualDokument12 SeitenTeel Industrial Series Water Circulating Pumps Operating Instructions and Parts Manualedwinprun12Noch keine Bewertungen

- Physical and Chemical Properties Analysis of Jatropha Curcas Seed Oil For Industrial ApplicationsDokument6 SeitenPhysical and Chemical Properties Analysis of Jatropha Curcas Seed Oil For Industrial ApplicationsAmr TarekNoch keine Bewertungen

- Poulan Chainsaw ManualDokument20 SeitenPoulan Chainsaw ManualAlyssa Sweeney SiebeNoch keine Bewertungen

- Misc-220-Draft Policy Petrol Pump-F1-18.12.2012Dokument5 SeitenMisc-220-Draft Policy Petrol Pump-F1-18.12.2012Nitin AhlawatNoch keine Bewertungen

- Basic Mechanical EngineeringDokument13 SeitenBasic Mechanical EngineeringJaysun Lanario PacrisNoch keine Bewertungen

- CPCL Training Part TwoDokument359 SeitenCPCL Training Part TwoAlex LeeNoch keine Bewertungen

- Lube and Bleed Operation KLS-1 Rig Less Feb 2017Dokument19 SeitenLube and Bleed Operation KLS-1 Rig Less Feb 2017Ali Boubenia100% (1)

- Manual Powerflame C PDFDokument56 SeitenManual Powerflame C PDFRoberto MnedezNoch keine Bewertungen

- DistillengDokument2 SeitenDistillengFraz AhmadNoch keine Bewertungen

- Reservoir Engineering 1 (Introduction)Dokument15 SeitenReservoir Engineering 1 (Introduction)okpaire lawsonNoch keine Bewertungen

- Mostuf CatalogDokument10 SeitenMostuf CatalogHamed MemarianNoch keine Bewertungen

- Tank Farm OperationsDokument77 SeitenTank Farm OperationsAnyarogbu Uchenna87% (23)

- Physics EEDokument4 SeitenPhysics EEEjaz AhmadNoch keine Bewertungen

- GMA Garnet™ SpeedBlast 2013Dokument2 SeitenGMA Garnet™ SpeedBlast 2013Srinivasan RNoch keine Bewertungen

- Wood Gasifier ManualDokument12 SeitenWood Gasifier ManualEvan AV90% (10)

- What Is Pyrolysis Process - BiogreenDokument2 SeitenWhat Is Pyrolysis Process - BiogreendenisebonemerNoch keine Bewertungen

- Heat Treatment of Thin Wall Tanks by Internal Oil Firing MethodDokument7 SeitenHeat Treatment of Thin Wall Tanks by Internal Oil Firing MethodKrishna VachaNoch keine Bewertungen

- Joint Coating Application & Pipe Coating ProcedureDokument7 SeitenJoint Coating Application & Pipe Coating Proceduregst ajahNoch keine Bewertungen

- Eko Boiler ManualDokument30 SeitenEko Boiler ManualglynisNoch keine Bewertungen

- Burn Safety and PreventionDokument7 SeitenBurn Safety and PreventionTaufan Arif ZulkarnainNoch keine Bewertungen

- Final Report NDT PDFDokument8 SeitenFinal Report NDT PDFAbhay Shankar MishraNoch keine Bewertungen

- 01 Refinery BasicsDokument94 Seiten01 Refinery BasicsjtichemicalNoch keine Bewertungen

- Crude TBP Country Nigeria Distillation: Akpo BlendDokument2 SeitenCrude TBP Country Nigeria Distillation: Akpo Blendeke23Noch keine Bewertungen

- Slip Form PaverDokument183 SeitenSlip Form PaverAlejandro PeowichNoch keine Bewertungen

- Yamaha SHO Service Manual PDFDokument433 SeitenYamaha SHO Service Manual PDFDernica Mandy100% (2)

- Which Part of The Mechanical Governor Is Manipulated by The ServoDokument8 SeitenWhich Part of The Mechanical Governor Is Manipulated by The ServoYanaNoch keine Bewertungen

- (AAPGndx - Sonnenberg) - Unconventional Tight Petroleum Systems Oil and GasDokument8 Seiten(AAPGndx - Sonnenberg) - Unconventional Tight Petroleum Systems Oil and GasAl MartinNoch keine Bewertungen

- Petroleum Services Division: Reservoir Fluid Study For Vetra Group Cohembi-1Dokument32 SeitenPetroleum Services Division: Reservoir Fluid Study For Vetra Group Cohembi-1CamiHoyosBetancourtNoch keine Bewertungen

- Kopr Kote Oilfield TdsDokument1 SeiteKopr Kote Oilfield TdsobryjefaNoch keine Bewertungen

- Boeing 727 - 71 (Gen Fam)Dokument15 SeitenBoeing 727 - 71 (Gen Fam)ElLoko Martines100% (2)