Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Shine To Inspire Newsletter Nov2013 - Vol 1Dokument19 SeitenShine To Inspire Newsletter Nov2013 - Vol 1imran_nazir448687Noch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- What Is Fuel TrimDokument8 SeitenWhat Is Fuel Trimimran_nazir448687Noch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- DBMSDokument58 SeitenDBMSimran_nazir448687Noch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- SOP For TRX Upgrade-DowngradeDokument1 SeiteSOP For TRX Upgrade-Downgradeimran_nazir448687Noch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Philips BDP 9600 Service ManualDokument45 SeitenPhilips BDP 9600 Service Manualimran_nazir448687Noch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- BBS Parameter Settings RBS-TMRDokument3 SeitenBBS Parameter Settings RBS-TMRimran_nazir448687Noch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Benefits of Carbon Cleaning!: Technology That We Can Trust! Motor Clean Oxy-Hydrogen Carbon Cleaning System!Dokument2 SeitenBenefits of Carbon Cleaning!: Technology That We Can Trust! Motor Clean Oxy-Hydrogen Carbon Cleaning System!imran_nazir448687Noch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Case Study: BG Tunisia Boosts Offshore Communications CapacityDokument2 SeitenCase Study: BG Tunisia Boosts Offshore Communications Capacityimran_nazir448687Noch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Chapt 2 Financial Market EnvironmentDokument20 SeitenChapt 2 Financial Market Environmentimran_nazir448687Noch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Relationship Between TPSDokument3 SeitenThe Relationship Between TPSimran_nazir448687Noch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- 2 - SDLC - Adaptive and PredictiveDokument3 Seiten2 - SDLC - Adaptive and Predictiveimran_nazir44868767% (3)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Assignment For MBAEDokument1 SeiteAssignment For MBAEimran_nazir448687Noch keine Bewertungen

- Timewise GRE Analytical Writing StrategiesDokument6 SeitenTimewise GRE Analytical Writing StrategiesrfmaniaNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- BEGP2 OutDokument28 SeitenBEGP2 OutSainadha Reddy PonnapureddyNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Chapter 5Dokument2 SeitenChapter 5Ynna RaymondNoch keine Bewertungen

- 2012 DMO Unified System of AccountsDokument30 Seiten2012 DMO Unified System of AccountshungrynicetiesNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Chap 001Dokument40 SeitenChap 001AhmedNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Decentralize Smart Contract PlatformDokument12 SeitenDecentralize Smart Contract PlatformSindhu ThomasNoch keine Bewertungen

- Form ITR-6Dokument35 SeitenForm ITR-6Accounting & TaxationNoch keine Bewertungen

- Overpriced Jeans, Inc. - Transactions - Additional InformationDokument11 SeitenOverpriced Jeans, Inc. - Transactions - Additional InformationKeshav TayalNoch keine Bewertungen

- UNEP GEF Project Document: Energy For Sustainable Development in Caribbean Buildings, 7-2012Dokument235 SeitenUNEP GEF Project Document: Energy For Sustainable Development in Caribbean Buildings, 7-2012Detlef LoyNoch keine Bewertungen

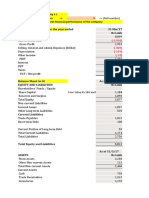

- All Numbers Are in INR and in x10MDokument6 SeitenAll Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- APM Assignment 2 - by SameeraDokument18 SeitenAPM Assignment 2 - by SameeraRahull GurnaniNoch keine Bewertungen

- Online Quiz 8 Performance Evaluation Q&ADokument5 SeitenOnline Quiz 8 Performance Evaluation Q&AjonNoch keine Bewertungen

- FordDokument97 SeitenFordbhaktishah117Noch keine Bewertungen

- Secretary of The Department of Finance vs. Court of Tax Appeals (Second Division)Dokument12 SeitenSecretary of The Department of Finance vs. Court of Tax Appeals (Second Division)KeiNoch keine Bewertungen

- Hsslive Xii Accountancy CA Focus Notes Binoy 2022Dokument166 SeitenHsslive Xii Accountancy CA Focus Notes Binoy 2022Manu BabuNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The 5Ms of ManagementDokument2 SeitenThe 5Ms of Managementhani5275% (8)

- BTS Accounting Firm Trial Balance December 31, 2014Dokument4 SeitenBTS Accounting Firm Trial Balance December 31, 2014Trisha AlaNoch keine Bewertungen

- GOvernance Test QuestionsDokument1 SeiteGOvernance Test QuestionsChristine Leal100% (1)

- Periyar University: Periyar Palkalai Nagar SALEM - 636011Dokument48 SeitenPeriyar University: Periyar Palkalai Nagar SALEM - 636011sureshkumarNoch keine Bewertungen

- Chapter 1 - Introduction To Managerial AccountingDokument22 SeitenChapter 1 - Introduction To Managerial AccountingviraNoch keine Bewertungen

- Books in Finance AreaDokument2 SeitenBooks in Finance AreaAanchal SinghalNoch keine Bewertungen

- Chapter 12 The Income StatementDokument26 SeitenChapter 12 The Income StatementNurul FaizahNoch keine Bewertungen

- 2nd CPC - CCS RP Rules 1960 - 02.8.1960Dokument178 Seiten2nd CPC - CCS RP Rules 1960 - 02.8.1960No NameNoch keine Bewertungen

- OpbyccDokument1 SeiteOpbyccUNoch keine Bewertungen

- The Institute of Bankers, Bangladesh: DaibbDokument1 SeiteThe Institute of Bankers, Bangladesh: DaibbAdhayon Joseph DasNoch keine Bewertungen

- The Factors That Affects The Investment Behavior (PPT c1)Dokument24 SeitenThe Factors That Affects The Investment Behavior (PPT c1)Jiezle JavierNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Global Dominion APPLICATION FORM May 4, 2021Dokument2 SeitenGlobal Dominion APPLICATION FORM May 4, 2021Erwin Dela CruzNoch keine Bewertungen

- Winner Team Memorial Respondent Gnlu International Law MootDokument18 SeitenWinner Team Memorial Respondent Gnlu International Law Mootsanikasunil1552Noch keine Bewertungen

- Valuation Under CertaintyDokument11 SeitenValuation Under CertaintyMusadiq_Elahi_7941Noch keine Bewertungen

- Absolute Deed of SaleDokument3 SeitenAbsolute Deed of SaleNN DDL67% (3)