Das könnte Ihnen auch gefallen

- Case Solution Titanium DioxideDokument4 SeitenCase Solution Titanium Dioxideanmolsaini01Noch keine Bewertungen

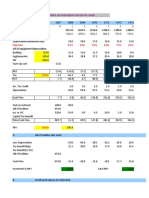

- Gross Profit Ad Expenses Depreciation (Dedicated Inv) Jell-O Equipment DepreciationDokument11 SeitenGross Profit Ad Expenses Depreciation (Dedicated Inv) Jell-O Equipment Depreciationanmolsaini01Noch keine Bewertungen

- Technical Analysis: Online Training Program OnDokument4 SeitenTechnical Analysis: Online Training Program Onanmolsaini01Noch keine Bewertungen

- Agri Morris V AidDokument19 SeitenAgri Morris V Aidanmolsaini01Noch keine Bewertungen

- Exhibit 4 (B) : Volatility of Foreign Exchange Ratesa (1/86-9/95)Dokument5 SeitenExhibit 4 (B) : Volatility of Foreign Exchange Ratesa (1/86-9/95)anmolsaini01Noch keine Bewertungen

- Agricultural Development Role of State - AgriComp - 09Dokument6 SeitenAgricultural Development Role of State - AgriComp - 09anmolsaini01Noch keine Bewertungen

- Prelims Special: Current AffairsDokument52 SeitenPrelims Special: Current Affairsanmolsaini01Noch keine Bewertungen

- Marriott Cost of CapitalDokument3 SeitenMarriott Cost of Capitalanmolsaini01Noch keine Bewertungen

- 28marchindia Year Book 2018 - Volume II Binder PDFDokument128 Seiten28marchindia Year Book 2018 - Volume II Binder PDFBijay Kumar SwainNoch keine Bewertungen

- March Prelims Special Current Affairs Binder-IiiDokument60 SeitenMarch Prelims Special Current Affairs Binder-IiiPradeep EthanNoch keine Bewertungen

- Book Building ProcessDokument17 SeitenBook Building Processmukesha.kr100% (9)

- Grammer RuleDokument104 SeitenGrammer Rulegourav rakshitNoch keine Bewertungen

- Gears and NomenclatureDokument27 SeitenGears and NomenclatureJJNoch keine Bewertungen

- CSP GS Paper1 PDFDokument40 SeitenCSP GS Paper1 PDFSumit MishraNoch keine Bewertungen

- Memory Based Sbi (English) PDFDokument13 SeitenMemory Based Sbi (English) PDFdragonbourneNoch keine Bewertungen

- SBI PO MAINS Data Analysis Interpretation Memory Based 1Dokument4 SeitenSBI PO MAINS Data Analysis Interpretation Memory Based 1Binay TripathyNoch keine Bewertungen

- G8 (Forum) - Wikipedia, The Free EncyclopediaDokument25 SeitenG8 (Forum) - Wikipedia, The Free Encyclopediaanmolsaini01Noch keine Bewertungen

- Compression Ignition Engine CombustionDokument81 SeitenCompression Ignition Engine CombustionHarish Reddy Singamala100% (1)

- Banking Quiz PDFDokument37 SeitenBanking Quiz PDFmonamiNoch keine Bewertungen

- One Liners Geography Final PDFDokument10 SeitenOne Liners Geography Final PDFanmolsaini01Noch keine Bewertungen

- Strategy Adopted For Financial InclusionDokument7 SeitenStrategy Adopted For Financial Inclusionanmolsaini01Noch keine Bewertungen

- Financial Terms A-ZDokument6 SeitenFinancial Terms A-ZHarish NagamaniNoch keine Bewertungen

- Article 4Dokument9 SeitenArticle 4anmolsaini01Noch keine Bewertungen

- Uid and Financial InclusionDokument15 SeitenUid and Financial Inclusionanmolsaini01Noch keine Bewertungen

- Bod CeoDokument43 SeitenBod Ceoanmolsaini01Noch keine Bewertungen

- Used Cars - Cam Huifenfkehfuoehnjlewnvoihepfn Euwfioenfq Efvuiqenf QefbqefiofnpusDokument2 SeitenUsed Cars - Cam Huifenfkehfuoehnjlewnvoihepfn Euwfioenfq Efvuiqenf Qefbqefiofnpusanmolsaini01Noch keine Bewertungen

- Risk Analysis in InvestmentDokument39 SeitenRisk Analysis in Investmentanmolsaini01Noch keine Bewertungen

- 00chapter 3 Hhkukuh Nugigjlk NKNKLNG VTTVHJ HJTFTDokument136 Seiten00chapter 3 Hhkukuh Nugigjlk NKNKLNG VTTVHJ HJTFTanmolsaini01Noch keine Bewertungen

- Interview Checklist QJQQB UIQ UIWBJ WB W 8Q3YGUI 7 EE G U QVYQ9GUQGU G7QGY 9Q BFBWEDokument1 SeiteInterview Checklist QJQQB UIQ UIWBJ WB W 8Q3YGUI 7 EE G U QVYQ9GUQGU G7QGY 9Q BFBWEanmolsaini01Noch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Jolly Phonics Teaching Reading and WritingDokument6 SeitenJolly Phonics Teaching Reading and Writingmarcela33j5086100% (1)

- Ais 301w Resume AssignmentDokument3 SeitenAis 301w Resume Assignmentapi-532849829Noch keine Bewertungen

- 2200SRM0724 (04 2005) Us en PDFDokument98 Seiten2200SRM0724 (04 2005) Us en PDFMayerson AlmaoNoch keine Bewertungen

- 2018 World Traumatic Dental Injury Prevalence and IncidenceDokument16 Seiten2018 World Traumatic Dental Injury Prevalence and IncidencebaridinoNoch keine Bewertungen

- Paul Daugerdas IndictmentDokument79 SeitenPaul Daugerdas IndictmentBrian Willingham100% (2)

- I Will Call Upon The Lord - ACYM - NewestDokument1 SeiteI Will Call Upon The Lord - ACYM - NewestGerd SteveNoch keine Bewertungen

- Guide To Djent ToneDokument6 SeitenGuide To Djent ToneCristiana MusellaNoch keine Bewertungen

- Word Formation - ExercisesDokument4 SeitenWord Formation - ExercisesAna CiocanNoch keine Bewertungen

- What's The Line Between Middle Class, Upper Middle Class, and Upper Class in Britain - QuoraDokument11 SeitenWhat's The Line Between Middle Class, Upper Middle Class, and Upper Class in Britain - QuoraFaizan ButtNoch keine Bewertungen

- (Cambridge Series in Statistical and Probabilistic Mathematics) Gerhard Tutz, Ludwig-Maximilians-Universität Munchen - Regression For Categorical Data-Cambridge University Press (2012)Dokument574 Seiten(Cambridge Series in Statistical and Probabilistic Mathematics) Gerhard Tutz, Ludwig-Maximilians-Universität Munchen - Regression For Categorical Data-Cambridge University Press (2012)shu100% (2)

- Reconsidering Puerto Rico's Status After 116 Years of Colonial RuleDokument3 SeitenReconsidering Puerto Rico's Status After 116 Years of Colonial RuleHéctor Iván Arroyo-SierraNoch keine Bewertungen

- The Human Element is Critical in Personal SellingDokument18 SeitenThe Human Element is Critical in Personal SellingArsalan AhmedNoch keine Bewertungen

- Twin-Field Quantum Key Distribution Without Optical Frequency DisseminationDokument8 SeitenTwin-Field Quantum Key Distribution Without Optical Frequency DisseminationHareesh PanakkalNoch keine Bewertungen

- Lung BiopsyDokument8 SeitenLung BiopsySiya PatilNoch keine Bewertungen

- Numl Lahore Campus Break Up of Fee (From 1St To 8Th Semester) Spring-Fall 2016Dokument1 SeiteNuml Lahore Campus Break Up of Fee (From 1St To 8Th Semester) Spring-Fall 2016sajeeNoch keine Bewertungen

- The Research TeamDokument4 SeitenThe Research Teamapi-272078177Noch keine Bewertungen

- Assisting A Tracheostomy ProcedureDokument2 SeitenAssisting A Tracheostomy ProcedureMIKKI100% (2)

- 6 - English-How I Taught My Grandmother To Read and Grammar-Notes&VLDokument11 Seiten6 - English-How I Taught My Grandmother To Read and Grammar-Notes&VLManav100% (2)

- Ororbia Maze LearningDokument10 SeitenOrorbia Maze LearningTom WestNoch keine Bewertungen

- Telesure Mock 8Dokument13 SeitenTelesure Mock 8Letlhogonolo RatselaneNoch keine Bewertungen

- Aiatsoymeo2016t06 SolutionDokument29 SeitenAiatsoymeo2016t06 Solutionsanthosh7kumar-24Noch keine Bewertungen

- Discrete Mathematics - Logical EquivalenceDokument9 SeitenDiscrete Mathematics - Logical EquivalenceEisha IslamNoch keine Bewertungen

- Comparative Ethnographies: State and Its MarginsDokument31 SeitenComparative Ethnographies: State and Its MarginsJuan ManuelNoch keine Bewertungen

- Speed of Sound and its Relationship with TemperatureDokument2 SeitenSpeed of Sound and its Relationship with TemperatureBENNY CALLONoch keine Bewertungen

- 3B Adverbial PhrasesDokument1 Seite3B Adverbial PhrasesSarah INoch keine Bewertungen

- Chapter 1. Introduction To TCPIP NetworkingDokument15 SeitenChapter 1. Introduction To TCPIP NetworkingPoojitha NagarajaNoch keine Bewertungen

- Gcse English Literature Coursework Grade BoundariesDokument8 SeitenGcse English Literature Coursework Grade Boundariesafjwfealtsielb100% (1)

- Foundation of Special and Inclusive EducationDokument25 SeitenFoundation of Special and Inclusive Educationmarjory empredoNoch keine Bewertungen

- Ns5e rw3 SB Ak HyeDokument24 SeitenNs5e rw3 SB Ak HyeKeys Shield JoshuaNoch keine Bewertungen

- Debt Recovery Management of SBIDokument128 SeitenDebt Recovery Management of SBIpranjalamishra100% (6)