Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Glio CoverageDokument53 SeitenGlio Coveragevictor xiangNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Fact SheetDokument2 SeitenFact Sheetvictor xiangNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- LazardGlobalListedInfrastructurePortfolio FactCard 2Dokument4 SeitenLazardGlobalListedInfrastructurePortfolio FactCard 2victor xiangNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Why Infrastructure NowDokument8 SeitenWhy Infrastructure Nowvictor xiangNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Fact SheetDokument2 SeitenFact Sheetvictor xiangNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- LazardGlobalListedInfrastructurePortfolio FactCard 2Dokument4 SeitenLazardGlobalListedInfrastructurePortfolio FactCard 2victor xiangNoch keine Bewertungen

- Icf LCF A BookletDokument20 SeitenIcf LCF A BookletDhwanik DoshiNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Invoice - 622 #1Dokument2 SeitenInvoice - 622 #1Serena GothNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Time Value ProblemDokument8 SeitenTime Value ProblemPrantik RayNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Microstructure Invariance in U.S. Stock Market TradesDokument36 SeitenMicrostructure Invariance in U.S. Stock Market TradesRolf ScheiderNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Marketing Grewal 4th Edition Solutions ManualDokument26 SeitenMarketing Grewal 4th Edition Solutions ManualPeterThomasizbjf100% (77)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- 2014 Opportunistic Deep Value Investing A Multi Asset Class Approach WPDokument13 Seiten2014 Opportunistic Deep Value Investing A Multi Asset Class Approach WPMeester KewpieNoch keine Bewertungen

- 10 1016@j Iedeen 2020 08 002Dokument10 Seiten10 1016@j Iedeen 2020 08 002HgoglezNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Practice Problem Set #1: Time Value of Money I Theoretical and Conceptual Questions: (See Notes or Textbook For Solutions)Dokument15 SeitenPractice Problem Set #1: Time Value of Money I Theoretical and Conceptual Questions: (See Notes or Textbook For Solutions)raymondNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- CF Risk ReturnDokument13 SeitenCF Risk Return979044775Noch keine Bewertungen

- Brockhaus-Long ApproximationDokument8 SeitenBrockhaus-Long Approximationmainak.chatterjee03Noch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Eric Speron Pages From Oddball - Newsletter - Issue - 36Dokument7 SeitenEric Speron Pages From Oddball - Newsletter - Issue - 36Nate Tobik100% (1)

- North South University: Mr. Hasan A. Mamun Senior LecturerDokument7 SeitenNorth South University: Mr. Hasan A. Mamun Senior Lecturerফারজানা মিমুNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Global Capital Market: International BusinessDokument15 SeitenThe Global Capital Market: International Businesssonia_hun885443Noch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- ReportDokument3 SeitenReportnancysinglaNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

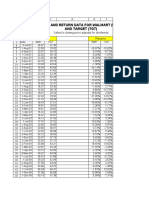

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDokument19 SeitenPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNoch keine Bewertungen

- IA 3 - BVPS and EPS - SolutionsDokument22 SeitenIA 3 - BVPS and EPS - SolutionsPatríck LouieNoch keine Bewertungen

- Project Report On Portfolio Management Services-An Investment Option atDokument31 SeitenProject Report On Portfolio Management Services-An Investment Option atsurya4searchNoch keine Bewertungen

- Tokenisation of Alternative InvestmentsDokument68 SeitenTokenisation of Alternative InvestmentsHari Sandeep ReddyNoch keine Bewertungen

- WK 4 SA Financial Market Shareholder AnalysisDokument7 SeitenWK 4 SA Financial Market Shareholder AnalysisShirley HaynesNoch keine Bewertungen

- Return and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)Dokument52 SeitenReturn and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)anna_alwanNoch keine Bewertungen

- Al MT 202101 BBCF2013 AnswersDokument11 SeitenAl MT 202101 BBCF2013 AnswersNabila Abu BakarNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Oligopoly - Practice Questions With Solutions - OligopolyDokument2 SeitenOligopoly - Practice Questions With Solutions - OligopolyLavNoch keine Bewertungen

- VUL MOck 2Dokument10 SeitenVUL MOck 2Franz JosephNoch keine Bewertungen

- IBP S7 Market AnalysisDokument36 SeitenIBP S7 Market Analysisjose vergarayNoch keine Bewertungen

- Supplemental Information Fourth Quarter 2009Dokument66 SeitenSupplemental Information Fourth Quarter 2009ariw99Noch keine Bewertungen

- 43-Interview-Tips-Asset ManagementDokument2 Seiten43-Interview-Tips-Asset ManagementAdnan NaboulsyNoch keine Bewertungen

- NFX-Scalper Pro V5 TutorialDokument6 SeitenNFX-Scalper Pro V5 TutorialBrandon SanjayaNoch keine Bewertungen

- Commerce Term-End ExaminationDokument4 SeitenCommerce Term-End ExaminationTushar SharmaNoch keine Bewertungen

- Synopsis On: Submitted in Partial Fulfilment of The Award of The Degree ofDokument7 SeitenSynopsis On: Submitted in Partial Fulfilment of The Award of The Degree ofMahaveer ChoudharyNoch keine Bewertungen

- What Is A Mutual Fund?Dokument35 SeitenWhat Is A Mutual Fund?Azaan KhanNoch keine Bewertungen

- 2022 ICT Mentorship Episode 6Dokument46 Seiten2022 ICT Mentorship Episode 6Jérôme Schaad100% (4)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)