Das könnte Ihnen auch gefallen

- COA & COMELEC R4A - APMT 2017 ML SAOR With DetailsDokument8 SeitenCOA & COMELEC R4A - APMT 2017 ML SAOR With DetailsVicky Danila AlbanoNoch keine Bewertungen

- Action Plan Monitoring Tool COA and COMELECDokument7 SeitenAction Plan Monitoring Tool COA and COMELECVicky Danila Albano100% (1)

- 10-CalapanCity2019 Part3-Status of PYs RecommDokument24 Seiten10-CalapanCity2019 Part3-Status of PYs RecommkQy267BdTKNoch keine Bewertungen

- Finance & Budget User Guide-ExpenditureDokument47 SeitenFinance & Budget User Guide-ExpenditureAnne-Marie OyugaNoch keine Bewertungen

- Format of Project Proposal For Grant Under CSR: Annexure-1Dokument5 SeitenFormat of Project Proposal For Grant Under CSR: Annexure-1Ko LabNoch keine Bewertungen

- IPCR JAN-JUN 2018-Inventory SectionDokument143 SeitenIPCR JAN-JUN 2018-Inventory SectionMathan LuceroNoch keine Bewertungen

- Checklist 3-Documentary Requirements For Budgetary Requests-Lgu, Lwds-Rev. 5.0 (As of June 2022)Dokument2 SeitenChecklist 3-Documentary Requirements For Budgetary Requests-Lgu, Lwds-Rev. 5.0 (As of June 2022)Genesis ArsuloNoch keine Bewertungen

- Changamka Economic and Social Dev.Dokument50 SeitenChangamka Economic and Social Dev.Erustus Festus OukoNoch keine Bewertungen

- Action Plans For COA Audit Observations 2019 and Prior YearsDokument6 SeitenAction Plans For COA Audit Observations 2019 and Prior YearsJebs KwanNoch keine Bewertungen

- Planning, Budgeting and Defense of Plan and Budget ProposalDokument11 SeitenPlanning, Budgeting and Defense of Plan and Budget ProposalZyreen Kate BCNoch keine Bewertungen

- Commonwealth Avenue, Quezon City, Philippines: Republic of The Philippines Commission On AuditDokument4 SeitenCommonwealth Avenue, Quezon City, Philippines: Republic of The Philippines Commission On AuditMJ BajaNoch keine Bewertungen

- Aapsi 2020Dokument9 SeitenAapsi 2020Ragnar LothbrokNoch keine Bewertungen

- Recio, Angelic ADokument18 SeitenRecio, Angelic AAngelic RecioNoch keine Bewertungen

- AOM Draft 23-11 (NLPSC - Interim)Dokument2 SeitenAOM Draft 23-11 (NLPSC - Interim)Jasmine Kay ReyesNoch keine Bewertungen

- Audit Objections RulesDokument164 SeitenAudit Objections Rulesramancs19850% (1)

- Recio, Angelic A-IpcrDokument18 SeitenRecio, Angelic A-IpcrAngelic RecioNoch keine Bewertungen

- Coa C97-002Dokument4 SeitenCoa C97-002Hoven MacasinagNoch keine Bewertungen

- Form 7 Fund Transfers To Non-Government or People - S OrganizationsDokument1 SeiteForm 7 Fund Transfers To Non-Government or People - S Organizationsarfica zainal abidinNoch keine Bewertungen

- National Privacy Commission Executive Summary 2017Dokument6 SeitenNational Privacy Commission Executive Summary 2017Sheena Mae KitongNoch keine Bewertungen

- 6.05.2020.ETDD Weekley Accomplishment Report Covering The Period June 1 To 5, 2020Dokument4 Seiten6.05.2020.ETDD Weekley Accomplishment Report Covering The Period June 1 To 5, 2020Maria Lira JalandoniNoch keine Bewertungen

- Tanza2020 Audit ReportDokument168 SeitenTanza2020 Audit ReportmAmei DiwataNoch keine Bewertungen

- RA Bill Part-III Bill No 3Dokument1 SeiteRA Bill Part-III Bill No 3Lambodar NaikNoch keine Bewertungen

- Report PAO16Dokument48 SeitenReport PAO16sandeep pahalNoch keine Bewertungen

- Contoh Action Plan Penerapan - English VersionDokument2 SeitenContoh Action Plan Penerapan - English VersionDiah NurJulianaNoch keine Bewertungen

- 54-Mcc-Qop-Lgl-001 - Final 13aug2020Dokument11 Seiten54-Mcc-Qop-Lgl-001 - Final 13aug2020KarlaColinaNoch keine Bewertungen

- EOI Penyiapan Izin Operasi Bendungan PDFDokument12 SeitenEOI Penyiapan Izin Operasi Bendungan PDFmelati jayagiriNoch keine Bewertungen

- DO 003 S2011 Updated Consultancy Billing GuidelinesDokument274 SeitenDO 003 S2011 Updated Consultancy Billing GuidelinesChito jungoyNoch keine Bewertungen

- LGSF ANNEX B Sample OnlyDokument2 SeitenLGSF ANNEX B Sample OnlyRen Mathew QuitorianoNoch keine Bewertungen

- Annex A MavuDokument12 SeitenAnnex A Mavusoncrmp ncrmpndmadelhiNoch keine Bewertungen

- QMS 2017 Minutes of The Meeting On Management ReviewDokument3 SeitenQMS 2017 Minutes of The Meeting On Management ReviewThee BouyyNoch keine Bewertungen

- Audit Review PSA 560 Subsequent EventsDokument2 SeitenAudit Review PSA 560 Subsequent Eventsetackenneth961Noch keine Bewertungen

- Mbhashe Municipality Idp & Budget Process Plan 2015 - 2016Dokument10 SeitenMbhashe Municipality Idp & Budget Process Plan 2015 - 2016sbuja7Noch keine Bewertungen

- Sample Procurement Plan: Aug 2017 - Dec 2017Dokument6 SeitenSample Procurement Plan: Aug 2017 - Dec 2017aliakhtar02Noch keine Bewertungen

- For The Ministry of Integration and Reconciliation: Concept PaperDokument5 SeitenFor The Ministry of Integration and Reconciliation: Concept PapersuntharthiNoch keine Bewertungen

- LGSF Am Quarterly Report FormatDokument1 SeiteLGSF Am Quarterly Report FormatMarie AlejoNoch keine Bewertungen

- Project Proposal Template For Grant Agreements 2023Dokument2 SeitenProject Proposal Template For Grant Agreements 2023saparudinikspiNoch keine Bewertungen

- EDELYNDokument4 SeitenEDELYNjhonx talahibanNoch keine Bewertungen

- Commission On AuditDokument207 SeitenCommission On AuditJaniceNoch keine Bewertungen

- Form Code: F-RAI-006 Revision No.: 0 Effective Date: July 03, 2017 Page No.: Page 1 of 2Dokument2 SeitenForm Code: F-RAI-006 Revision No.: 0 Effective Date: July 03, 2017 Page No.: Page 1 of 2Jerusalem AlardeNoch keine Bewertungen

- Sample OFI Report FormDokument12 SeitenSample OFI Report FormSarah Jane UsopNoch keine Bewertungen

- Philippine Carabao Center USM Kabacan, North Cotabato Agency Action Plan and Status of Implementation Audit Observations and Recommendations For The Calendar Year 2018 As of March 2019Dokument2 SeitenPhilippine Carabao Center USM Kabacan, North Cotabato Agency Action Plan and Status of Implementation Audit Observations and Recommendations For The Calendar Year 2018 As of March 2019Mea Cocal JTNoch keine Bewertungen

- Part Iii - Status of Implementation of Prior Years' Audit RecommendationsDokument12 SeitenPart Iii - Status of Implementation of Prior Years' Audit RecommendationsAlicia NhsNoch keine Bewertungen

- 01-MMSU2019 Audit ReportDokument71 Seiten01-MMSU2019 Audit ReportGabriel OrolfoNoch keine Bewertungen

- Appendix+ G PM-Abhim TOR 2023-24Dokument7 SeitenAppendix+ G PM-Abhim TOR 2023-24cfeaakashtiwariNoch keine Bewertungen

- Plan Archive 19Dokument5 SeitenPlan Archive 19Kld HusNoch keine Bewertungen

- SP Final Revised Admin Qop Monitoring - 2017Dokument28 SeitenSP Final Revised Admin Qop Monitoring - 2017Ju LanNoch keine Bewertungen

- Final Copy of GHMC LBnagar IR - 1Dokument35 SeitenFinal Copy of GHMC LBnagar IR - 1District Audit Officer DAONoch keine Bewertungen

- Status of Implementation of Prior Years' Audit RecommendationDokument8 SeitenStatus of Implementation of Prior Years' Audit Recommendationsandra bolokNoch keine Bewertungen

- 140-First Management Progress Report-17 December 2021334Dokument23 Seiten140-First Management Progress Report-17 December 2021334assefamenelik1Noch keine Bewertungen

- AIMEEDokument2 SeitenAIMEEjhonx talahibanNoch keine Bewertungen

- Procurement Plan: The Bank's Standard Procurement DocumentsDokument14 SeitenProcurement Plan: The Bank's Standard Procurement DocumentsKévin PereiraNoch keine Bewertungen

- Visa QuestionsDokument12 SeitenVisa QuestionsMorshedDenarAlamMannaNoch keine Bewertungen

- 01-IlocosNorteProvince2020 Audit ReportDokument89 Seiten01-IlocosNorteProvince2020 Audit ReportRuffus TooqueroNoch keine Bewertungen

- Republic of The Philippines Commonwealth Avenue, Quezon CityDokument5 SeitenRepublic of The Philippines Commonwealth Avenue, Quezon CityOrlando V. Madrid Jr.Noch keine Bewertungen

- Corporate Guidance Events After The Reporting DateDokument17 SeitenCorporate Guidance Events After The Reporting DateGedionNoch keine Bewertungen

- Acp NC Iii Action Catalogue (Assessment Center)Dokument2 SeitenAcp NC Iii Action Catalogue (Assessment Center)mario layanNoch keine Bewertungen

- 17 Events After The Reporting Date 30 Sept 2021 Final For PublishingDokument12 Seiten17 Events After The Reporting Date 30 Sept 2021 Final For PublishingDineo NongNoch keine Bewertungen

- 310-A GAS FY 2024 TIER 1Dokument5 Seiten310-A GAS FY 2024 TIER 1MOTC INTERNAL AUDIT SECTIONNoch keine Bewertungen

- Public Financial Management Systems—Fiji: Key Elements from a Financial Management PerspectiveVon EverandPublic Financial Management Systems—Fiji: Key Elements from a Financial Management PerspectiveNoch keine Bewertungen

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanVon EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNoch keine Bewertungen

- Aging 148 2015 - DPPFDokument12 SeitenAging 148 2015 - DPPFLa AlvarezNoch keine Bewertungen

- 4rev AOM No. 2020-004.DPPF - Draft.bondDokument3 Seiten4rev AOM No. 2020-004.DPPF - Draft.bondLa AlvarezNoch keine Bewertungen

- 3rev AOM No. 2020-003.DPPF - draft.PPEReconDokument3 Seiten3rev AOM No. 2020-003.DPPF - draft.PPEReconLa AlvarezNoch keine Bewertungen

- 6rev AOM No. 2020-006 (19) DPPF - CIPpDokument3 Seiten6rev AOM No. 2020-006 (19) DPPF - CIPpLa AlvarezNoch keine Bewertungen

- 2019 CollectionsDokument42 Seiten2019 CollectionsLa AlvarezNoch keine Bewertungen

- Transmittal Letter IPCRDokument1 SeiteTransmittal Letter IPCRLa AlvarezNoch keine Bewertungen

- 0001 PPA Review NotesDokument5 Seiten0001 PPA Review NotesLa AlvarezNoch keine Bewertungen

- Final Qar 4th QRTRDokument52 SeitenFinal Qar 4th QRTRLa AlvarezNoch keine Bewertungen

- COnfirm Letter ITDokument1 SeiteCOnfirm Letter ITLa AlvarezNoch keine Bewertungen

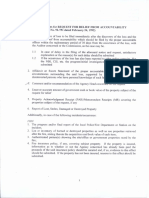

- Checklist of Documents For Request For Relief From AccountabilityDokument2 SeitenChecklist of Documents For Request For Relief From AccountabilityLa AlvarezNoch keine Bewertungen

- Sun Life Assure BrochureDokument3 SeitenSun Life Assure BrochureLa AlvarezNoch keine Bewertungen

- Cases FullDokument59 SeitenCases FullLa AlvarezNoch keine Bewertungen

- Audit Area Procument of Goods and Infrastructure Projects Risk StatementDokument5 SeitenAudit Area Procument of Goods and Infrastructure Projects Risk StatementLa AlvarezNoch keine Bewertungen

- Form 02-01.AAW - Team R11-11.CY2018Dokument6 SeitenForm 02-01.AAW - Team R11-11.CY2018La AlvarezNoch keine Bewertungen

- Sicat V AriolaDokument2 SeitenSicat V AriolaLa AlvarezNoch keine Bewertungen

- RA 9184 Implementing Rules and RegulationsDokument2 SeitenRA 9184 Implementing Rules and Regulationsamiel pugatNoch keine Bewertungen

- Fibrbiz Enterprise BroadbandDokument5 SeitenFibrbiz Enterprise Broadbandapi-497016885Noch keine Bewertungen

- Committee Investigation Report - Aviation Safety ReportDokument102 SeitenCommittee Investigation Report - Aviation Safety ReporttmuthukumarNoch keine Bewertungen

- BS en Iso 3691-6-2013Dokument38 SeitenBS en Iso 3691-6-2013yamen sayedNoch keine Bewertungen

- OSP Towing PolicyDokument4 SeitenOSP Towing PolicyMNCOOhio50% (2)

- Masoneilan - 78 Series Air Filter Regulators IOMDokument8 SeitenMasoneilan - 78 Series Air Filter Regulators IOMNithyANoch keine Bewertungen

- Practice Exercise 1.6Dokument3 SeitenPractice Exercise 1.6leshz zynNoch keine Bewertungen

- Espiritu Vs Cipriano 55 Scra 533Dokument2 SeitenEspiritu Vs Cipriano 55 Scra 533YenNoch keine Bewertungen

- Executive Summary: A. IntroductionDokument6 SeitenExecutive Summary: A. IntroductionMarcoNoch keine Bewertungen

- Administrative Code of The PhilippinesDokument11 SeitenAdministrative Code of The PhilippinesJestoni PabiaNoch keine Bewertungen

- Irish Standard I.S. EN ISO 11126-3:2018Dokument14 SeitenIrish Standard I.S. EN ISO 11126-3:2018Nitin KawareNoch keine Bewertungen

- Concentrated Clusters and Supply Chain ManagementDokument3 SeitenConcentrated Clusters and Supply Chain ManagementNael Nasir ChiraghNoch keine Bewertungen

- Appendix 3 EMS AUDIT CHECKLISTDokument9 SeitenAppendix 3 EMS AUDIT CHECKLISTSharif KhanNoch keine Bewertungen

- IT EnterpriseDokument10 SeitenIT EnterpriseNikki OcampoNoch keine Bewertungen

- Public Administration and Private AdministrationDokument4 SeitenPublic Administration and Private AdministrationRainaNoch keine Bewertungen

- Read Ellen Psychas and Bing Yee's Proposed Treehouse Rules in FullDokument4 SeitenRead Ellen Psychas and Bing Yee's Proposed Treehouse Rules in FullRachel SadonNoch keine Bewertungen

- Evolution of Corporate Reporting and Emerging Trends-JCAF-publishedDokument7 SeitenEvolution of Corporate Reporting and Emerging Trends-JCAF-publishedSathishKumar ArumugamNoch keine Bewertungen

- 2 (1) - G.O.Ms - No.901.MA DT 31.12 2007 PDFDokument12 Seiten2 (1) - G.O.Ms - No.901.MA DT 31.12 2007 PDFM V N MurtyNoch keine Bewertungen

- Remy L. Untalan - Educ Laws - Ca 177 & 578Dokument14 SeitenRemy L. Untalan - Educ Laws - Ca 177 & 578Remy Lopez UntalanNoch keine Bewertungen

- 2.10. Tongko vs. Manufacturer Life Insurance Co. (Phils), Inc., Et Al., G.R. No. 167622, January 25, 2011Dokument4 Seiten2.10. Tongko vs. Manufacturer Life Insurance Co. (Phils), Inc., Et Al., G.R. No. 167622, January 25, 2011Aid BolanioNoch keine Bewertungen

- Checklist For Office LeasesDokument6 SeitenChecklist For Office LeasesRevamp TwentyoneNoch keine Bewertungen

- RFP For Endpoint Email and Web SecurityDokument69 SeitenRFP For Endpoint Email and Web SecurityDinesh GaikwadNoch keine Bewertungen

- Competition Law and International TradeDokument17 SeitenCompetition Law and International Tradevainygoel100% (2)

- Stakeholders ' Perspectives On The Regulation and Integration of Complementary and Alternative Medicine Products in Lebanon: A Qualitative StudyDokument10 SeitenStakeholders ' Perspectives On The Regulation and Integration of Complementary and Alternative Medicine Products in Lebanon: A Qualitative StudyEdward Joshua NuguidNoch keine Bewertungen

- Employee Complaint LetterDokument6 SeitenEmployee Complaint LetterFrancisco Javier Talavera VillaNoch keine Bewertungen

- Boat Registration in The UkDokument10 SeitenBoat Registration in The UkSandraMcCoshamNoch keine Bewertungen

- Haywood Securities Launches CoverageDokument79 SeitenHaywood Securities Launches CoverageAnonymous 7USzmqTQ100% (1)

- Competition Law in India - An OverviewDokument9 SeitenCompetition Law in India - An OverviewDeepanshi S.Noch keine Bewertungen

- Factors To Consider in Starting A BusinessDokument12 SeitenFactors To Consider in Starting A BusinessAngelo DumaopNoch keine Bewertungen

- Notice: Hazardous Materials: Special Permit Applications ListDokument17 SeitenNotice: Hazardous Materials: Special Permit Applications ListJustia.comNoch keine Bewertungen