Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Adobe Scan Jul 28, 2022Dokument1 SeiteAdobe Scan Jul 28, 2022Palani KumarNoch keine Bewertungen

- To Tell A Tale The Use of Moral Dilemmas To Increase Empathy in The Elementary School ChildDokument6 SeitenTo Tell A Tale The Use of Moral Dilemmas To Increase Empathy in The Elementary School ChildPaula CamilaNoch keine Bewertungen

- PD 705 Revised - Forestry - CodeDokument36 SeitenPD 705 Revised - Forestry - CodeInter_vivosNoch keine Bewertungen

- At December 31 2014 The Records of Nortech Corporation Provided PDFDokument1 SeiteAt December 31 2014 The Records of Nortech Corporation Provided PDFFreelance WorkerNoch keine Bewertungen

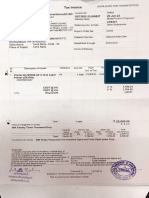

- Sales InvoiceDokument11 SeitenSales InvoiceMuhammad NurwegionoNoch keine Bewertungen

- Fact Sheet - Home Renovation Loan: MaybankDokument2 SeitenFact Sheet - Home Renovation Loan: MaybankLissa ChooNoch keine Bewertungen

- FNDWRR PDFDokument5 SeitenFNDWRR PDFngole ngoleNoch keine Bewertungen

- Modern History USA 1919-1941 NotesDokument13 SeitenModern History USA 1919-1941 NotesOliver Al-MasriNoch keine Bewertungen

- Boult Audio BillDokument1 SeiteBoult Audio BillBinay ShawNoch keine Bewertungen

- CBSE XII Economics NotesDokument165 SeitenCBSE XII Economics NoteschehalNoch keine Bewertungen

- Secretarial AuditDokument77 SeitenSecretarial Auditdkdinesh100% (1)

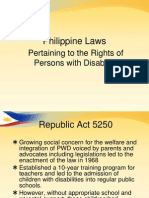

- Laws Pertaining To SPEDDokument20 SeitenLaws Pertaining To SPEDginasalyv73% (22)

- Corporate Social Responsibility (CSR) As A Model of "Extended" Corporate Governance. An Explanation Based On The Economic Theories of Social Contract, Reputation and Reciprocal ConformismDokument49 SeitenCorporate Social Responsibility (CSR) As A Model of "Extended" Corporate Governance. An Explanation Based On The Economic Theories of Social Contract, Reputation and Reciprocal ConformismronaqvNoch keine Bewertungen

- Cambridge IGCSE: Economics 0455/12Dokument12 SeitenCambridge IGCSE: Economics 0455/12ShadyNoch keine Bewertungen

- METROPOLITAN WATERWORKS SEWERAGE Vs Quezon CityDokument16 SeitenMETROPOLITAN WATERWORKS SEWERAGE Vs Quezon CityJaysonNoch keine Bewertungen

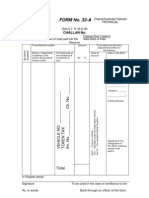

- Form 32A DtoDokument1 SeiteForm 32A Dtoapi-19912235Noch keine Bewertungen

- Nature and Purpose of BusinessDokument17 SeitenNature and Purpose of BusinessKunal SarohaNoch keine Bewertungen

- Form PDF 345858330310722Dokument10 SeitenForm PDF 345858330310722narasimhahanNoch keine Bewertungen

- Stamp PapersDokument2 SeitenStamp PapersAyesha ChhatwalNoch keine Bewertungen

- Tile SectorDokument33 SeitenTile SectorMike LassaNoch keine Bewertungen

- Journal of Cleaner Production: Yan Qin, Julie Harrison, Li ChenDokument27 SeitenJournal of Cleaner Production: Yan Qin, Julie Harrison, Li ChenTABAH RIZKINoch keine Bewertungen

- Researchspu, 13 Thanaporn KariyapolDokument13 SeitenResearchspu, 13 Thanaporn KariyapolSu MonsanNoch keine Bewertungen

- WEF Making Affordable Housing A Reality in Cities ReportDokument60 SeitenWEF Making Affordable Housing A Reality in Cities ReportAnonymous XUFoDm6dNoch keine Bewertungen

- Analyzing Political CartoonsDokument3 SeitenAnalyzing Political Cartoonsapi-589327192Noch keine Bewertungen

- Job Order CostingDokument1 SeiteJob Order CostingVincent Pham100% (1)

- Course Curriculum of MBA in Oil and Gas ManagementDokument31 SeitenCourse Curriculum of MBA in Oil and Gas Managementantopaul2Noch keine Bewertungen

- Data Visvilization Project Boston-Condo-SalesDokument61 SeitenData Visvilization Project Boston-Condo-SalesKATHIRVEL SNoch keine Bewertungen

- Roxas v. RaffertyDokument2 SeitenRoxas v. RaffertySophiaFrancescaEspinosaNoch keine Bewertungen

- NOLCO ReportDokument9 SeitenNOLCO ReportfebwinNoch keine Bewertungen