Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Advanced Management AccountingDokument204 SeitenAdvanced Management AccountingP TM100% (3)

- Accounting Entries in R12 Account Receivables - Oracle Apps Knowledge SharingDokument6 SeitenAccounting Entries in R12 Account Receivables - Oracle Apps Knowledge Sharingdevender143Noch keine Bewertungen

- Job Order Costing: Illustrative ProblemsDokument30 SeitenJob Order Costing: Illustrative ProblemsPatrick LanceNoch keine Bewertungen

- AP-5906 ReceivablesDokument5 SeitenAP-5906 Receivablesjhouvan100% (1)

- Doc/Inv No. Doc. Dt. D.T. Plant Destination Material Quantity Debit Credit Balance TextDokument2 SeitenDoc/Inv No. Doc. Dt. D.T. Plant Destination Material Quantity Debit Credit Balance TextPrashant EnterprisesNoch keine Bewertungen

- Iloilo Federation of Junior Philippine Institute of AccountantsDokument8 SeitenIloilo Federation of Junior Philippine Institute of AccountantsLysha DalipeNoch keine Bewertungen

- Accounting For Receivables: Summary of Questions by Study Objectives and Bloom'S TaxonomyDokument51 SeitenAccounting For Receivables: Summary of Questions by Study Objectives and Bloom'S TaxonomyRabie HarounNoch keine Bewertungen

- Job Opportunities World Bank IUCEA African Centers of Excellence (ACE II) ProjectDokument1 SeiteJob Opportunities World Bank IUCEA African Centers of Excellence (ACE II) ProjectRashid BumarwaNoch keine Bewertungen

- ReceivablesDokument4 SeitenReceivableshellohello50% (2)

- PETRONAS PIR2021 Financial Report 2021Dokument174 SeitenPETRONAS PIR2021 Financial Report 2021Ez BzNoch keine Bewertungen

- Entrep 7 Business Implementation Autosaved Autosaved April 242020Dokument62 SeitenEntrep 7 Business Implementation Autosaved Autosaved April 242020Carl Jayson Bravo-SierraNoch keine Bewertungen

- Sarangapani & Co: Chartered AccountantsDokument14 SeitenSarangapani & Co: Chartered AccountantsSarangapani KaliyamoorthyNoch keine Bewertungen

- Sap Fi GLDokument56 SeitenSap Fi GLrohitmandhania89% (9)

- Smruthi Organics LTD 2009Dokument51 SeitenSmruthi Organics LTD 2009rakesh_arorajprNoch keine Bewertungen

- Financial Statements PLDT and GLobeDokument18 SeitenFinancial Statements PLDT and GLobeArnelli GregorioNoch keine Bewertungen

- Paec Test PrepDokument4 SeitenPaec Test Prepaliakhtar02100% (3)

- Tally QuestionDokument9 SeitenTally QuestionmekavinashNoch keine Bewertungen

- Marasigan TransactionDokument20 SeitenMarasigan TransactionE.D.J100% (2)

- Session Ending Examination 2019Dokument7 SeitenSession Ending Examination 2019madhudevi06435Noch keine Bewertungen

- Full Download:: Suggested Answers To Discussion QuestionsDokument8 SeitenFull Download:: Suggested Answers To Discussion QuestionsIrawatiNoch keine Bewertungen

- Problem Solving: Merchandising Problem (Periodic Inventory System)Dokument1 SeiteProblem Solving: Merchandising Problem (Periodic Inventory System)Vincent Madrid100% (6)

- The The The Which Procedures? And: (! Te. of The Following Is ToDokument1 SeiteThe The The Which Procedures? And: (! Te. of The Following Is ToLove Sunshine BancaleNoch keine Bewertungen

- Lesson 1 - Introduction To AccountingDokument22 SeitenLesson 1 - Introduction To Accountingdelgadojudith100% (1)

- Who Wants To Get UnoDokument45 SeitenWho Wants To Get UnoCarmen YanguasNoch keine Bewertungen

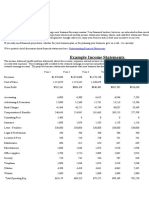

- Example Income Statements: Business Plan Financial ProjectionsDokument3 SeitenExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNoch keine Bewertungen

- Chapter 1-Introduction To Financial Reporting: Multiple ChoiceDokument17 SeitenChapter 1-Introduction To Financial Reporting: Multiple Choicekurinkato83100% (1)

- 1.statutory Audit MSME PDFDokument17 Seiten1.statutory Audit MSME PDFchariNoch keine Bewertungen

- Overheads: Faculty: Zaira AneesDokument59 SeitenOverheads: Faculty: Zaira AneesVishal MalhiNoch keine Bewertungen

- Graduate Recruitment Presentation BirmDokument23 SeitenGraduate Recruitment Presentation BirmSabeeh -ul -HassanNoch keine Bewertungen

- Accounting Principles - A Business Perspective, Financial AccountingDokument433 SeitenAccounting Principles - A Business Perspective, Financial Accountinggimi21100% (6)