Das könnte Ihnen auch gefallen

- 2 - Table of Contents and PREFACEDokument2 Seiten2 - Table of Contents and PREFACEasunaNoch keine Bewertungen

- Negotiable Instrument: Maker - Person Issuing A Promissory NoteDokument1 SeiteNegotiable Instrument: Maker - Person Issuing A Promissory NoteasunaNoch keine Bewertungen

- Proposal 2nd BatchDokument3 SeitenProposal 2nd BatchasunaNoch keine Bewertungen

- All Subj - Mock Board Exam BBDokument9 SeitenAll Subj - Mock Board Exam BBMJ YaconNoch keine Bewertungen

- Pastel Watercoljihihuhuhuhuhor Painted PowerPoint TemplateDokument38 SeitenPastel Watercoljihihuhuhuhuhor Painted PowerPoint TemplateasunaNoch keine Bewertungen

- Beautiful Monsta XDokument2 SeitenBeautiful Monsta Xasuna100% (1)

- Tax ReviewerDokument1 SeiteTax ReviewerasunaNoch keine Bewertungen

- Proposal 2nd BatchDokument3 SeitenProposal 2nd BatchasunaNoch keine Bewertungen

- CitationsDokument1 SeiteCitationsasunaNoch keine Bewertungen

- BeaaDokument2 SeitenBeaaasunaNoch keine Bewertungen

- Earthquakes PresentationDokument18 SeitenEarthquakes PresentationDeepak Lalwani100% (1)

- Financial Planning and Forecasting Financial StatementsDokument46 SeitenFinancial Planning and Forecasting Financial StatementsRimpy SondhNoch keine Bewertungen

- Barbie Ayen MDokument20 SeitenBarbie Ayen MasunaNoch keine Bewertungen

- Free PPT Templates: Insert The Title of Your Presentation HereDokument36 SeitenFree PPT Templates: Insert The Title of Your Presentation HereFinsaria FidiyantiNoch keine Bewertungen

- Free PPT Templates: Insert The Title of Your Presentation HereDokument36 SeitenFree PPT Templates: Insert The Title of Your Presentation HereFinsaria FidiyantiNoch keine Bewertungen

- NFJPIA Mockboard 2011 P1 PDFDokument9 SeitenNFJPIA Mockboard 2011 P1 PDFLei LucasNoch keine Bewertungen

- UrsulaDokument31 SeitenUrsulaasunaNoch keine Bewertungen

- SalerioDokument28 SeitenSalerioRizqaFebrilianyNoch keine Bewertungen

- Finance ReportDokument10 SeitenFinance ReportasunaNoch keine Bewertungen

- 7 Habits Summary PDFDokument11 Seiten7 Habits Summary PDFVu Huong LyNoch keine Bewertungen

- Capital Structure and LeverageDokument8 SeitenCapital Structure and LeverageasunaNoch keine Bewertungen

- 1accounting Process ExercisesDokument7 Seiten1accounting Process Exercisesasuna0% (1)

- NFJPIA - Mockboard 2011 - TOA PDFDokument7 SeitenNFJPIA - Mockboard 2011 - TOA PDFSteven Mark MananguNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- BC - IsiDokument15 SeitenBC - IsiBen DoverNoch keine Bewertungen

- Luffy Inc office building contract profit calculationDokument2 SeitenLuffy Inc office building contract profit calculationHernandez Aliah Cyril M.Noch keine Bewertungen

- Chapter 21 FinalDokument16 SeitenChapter 21 FinalMichael HuNoch keine Bewertungen

- Eyu-Ethiopia FinanceOperations Manual January2020 v1 EnglishDokument104 SeitenEyu-Ethiopia FinanceOperations Manual January2020 v1 EnglishHenockNoch keine Bewertungen

- Ivy Tech Course DescriptionsDokument172 SeitenIvy Tech Course DescriptionsEA MorrNoch keine Bewertungen

- Journal, Ledger & Trial BalanceDokument23 SeitenJournal, Ledger & Trial BalanceGarimaBhandariNoch keine Bewertungen

- Chapter 1Dokument68 SeitenChapter 1Merrill Ojeda SaflorNoch keine Bewertungen

- 2006 Nicolet National Bank Annual ReportDokument35 Seiten2006 Nicolet National Bank Annual ReportNicolet BankNoch keine Bewertungen

- MBA Finance Deepak Kumar Singh Janakpur Nepal ResumeDokument3 SeitenMBA Finance Deepak Kumar Singh Janakpur Nepal ResumeDeepak SinghNoch keine Bewertungen

- Types of Accounts and Rules For AccountingDokument5 SeitenTypes of Accounts and Rules For AccountingROSHAN KUMAR SHAHNoch keine Bewertungen

- CFI Accountingfactsheet-1499721167572 PDFDokument1 SeiteCFI Accountingfactsheet-1499721167572 PDFአረጋዊ ሐይለማርያምNoch keine Bewertungen

- The Cash Account For Collegiate Sports Co On November 1Dokument1 SeiteThe Cash Account For Collegiate Sports Co On November 1Miroslav GegoskiNoch keine Bewertungen

- Business Combination - SubsequentDokument2 SeitenBusiness Combination - SubsequentMaan CabolesNoch keine Bewertungen

- Anonymous and non-anonymous fraud reporting channels experiment resultsDokument44 SeitenAnonymous and non-anonymous fraud reporting channels experiment resultsadnan2406Noch keine Bewertungen

- Mapa MentalDokument8 SeitenMapa MentalJOHAN UBEIMAR PALMA ORTEGANoch keine Bewertungen

- Contemporary Auditing 10th Edition Knapp Solutions ManualDokument5 SeitenContemporary Auditing 10th Edition Knapp Solutions Manualgarconshudder.4m4fs100% (23)

- Accounting Chapter 5 SolutionsDokument13 SeitenAccounting Chapter 5 Solutionsali sherNoch keine Bewertungen

- MBA ACC 551 Class Material 2Dokument7 SeitenMBA ACC 551 Class Material 2RI ShawonNoch keine Bewertungen

- UntitledDokument3 SeitenUntitledKoki HabadiNoch keine Bewertungen

- Accounting Revision Notes and Assessment TasksDokument148 SeitenAccounting Revision Notes and Assessment TasksArnoldNoch keine Bewertungen

- Faf Tutorial 3 Ifrs 16Dokument4 SeitenFaf Tutorial 3 Ifrs 16嘉慧Noch keine Bewertungen

- Logistics Costing MethodsDokument19 SeitenLogistics Costing MethodsDhiraj BathijaNoch keine Bewertungen

- Notes in Business CombinationDokument5 SeitenNotes in Business CombinationEllen BuenafeNoch keine Bewertungen

- PRACTICLE GUIDE ON IAS 18 - Pwc-Pharma-Ifrs-Vol-Iii PDFDokument38 SeitenPRACTICLE GUIDE ON IAS 18 - Pwc-Pharma-Ifrs-Vol-Iii PDFBathina Srinivasa RaoNoch keine Bewertungen

- 2022 Con Quarter04 AllDokument93 Seiten2022 Con Quarter04 AllLORENA HERRERA CASTRONoch keine Bewertungen

- Chapter XXI - Bank ReconciliationDokument7 SeitenChapter XXI - Bank Reconciliationabbey89Noch keine Bewertungen

- List of Project Topics For Accountancy DDokument4 SeitenList of Project Topics For Accountancy DnebiyuNoch keine Bewertungen

- Advanced Accounting 13th Edition Hoyle Test Bank Full Chapter PDFDokument58 SeitenAdvanced Accounting 13th Edition Hoyle Test Bank Full Chapter PDFanwalteru32x100% (7)

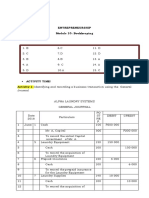

- Entrepreneurship Module 10: Bookkeeping What I KnowDokument23 SeitenEntrepreneurship Module 10: Bookkeeping What I KnowDos DosNoch keine Bewertungen

- Review Strategies of SLU CPA PassersDokument6 SeitenReview Strategies of SLU CPA PassersbrepoyoNoch keine Bewertungen