Das könnte Ihnen auch gefallen

- The Social Protection Indicator for the Pacific: Tracking Developments in Social ProtectionVon EverandThe Social Protection Indicator for the Pacific: Tracking Developments in Social ProtectionNoch keine Bewertungen

- Ch 8 Risk and ReturnDokument115 SeitenCh 8 Risk and Returnalmandouh.mustafa.khaledNoch keine Bewertungen

- Risk-Return_AnalysisDokument42 SeitenRisk-Return_AnalysisNaranbat NamsraiNoch keine Bewertungen

- 08 Zutter Smart PMF 16e ch08Dokument114 Seiten08 Zutter Smart PMF 16e ch08Hafez QawasmiNoch keine Bewertungen

- U.S. Financial Sector Volatility DriversDokument19 SeitenU.S. Financial Sector Volatility DriversZuzanaNoch keine Bewertungen

- Share DocumentDokument1.034 SeitenShare DocumentDeepak ChamaNoch keine Bewertungen

- Allianz Risk Barometer 2020Dokument24 SeitenAllianz Risk Barometer 2020ivanhoNoch keine Bewertungen

- Ces Dovern Lect2Dokument43 SeitenCes Dovern Lect2Laur LaurNoch keine Bewertungen

- Lecture 8-Policy Framework Scenario - 2017Dokument55 SeitenLecture 8-Policy Framework Scenario - 2017Mark EllyneNoch keine Bewertungen

- External Debt Challenges and Nigerian EconomyDokument14 SeitenExternal Debt Challenges and Nigerian EconomyBello AdoNoch keine Bewertungen

- Unit 5Dokument32 SeitenUnit 5Wgt ChampNoch keine Bewertungen

- JWB_SI_ON_RISK_Final_Acceptd_version_2020Dokument25 SeitenJWB_SI_ON_RISK_Final_Acceptd_version_2020Yongye ChenNoch keine Bewertungen

- 1-S2.0-S0165176520300628-Main - Not OkDokument4 Seiten1-S2.0-S0165176520300628-Main - Not Okjkwtxyd7gsNoch keine Bewertungen

- Plenary - Prof. Iwan Jaya Azis PDFDokument14 SeitenPlenary - Prof. Iwan Jaya Azis PDFQarinaNoch keine Bewertungen

- 1 s2.0 S0165176522000581 MainDokument3 Seiten1 s2.0 S0165176522000581 MainIbrahim KhatatbehNoch keine Bewertungen

- Risk Return UploadDokument15 SeitenRisk Return UploadGauri TyagiNoch keine Bewertungen

- State aid and tacit collusion in bankingDokument23 SeitenState aid and tacit collusion in bankingRodrigo FernandezNoch keine Bewertungen

- IEV - 2022 - Risk and ReturnDokument31 SeitenIEV - 2022 - Risk and ReturnKhushbu KumariNoch keine Bewertungen

- Connectedness Between Travel & Tourism Tokens, Tourism EquityDokument9 SeitenConnectedness Between Travel & Tourism Tokens, Tourism EquityRodrigo BertelliNoch keine Bewertungen

- A54 Peer Effect On Corporate Cash Holdings 20121108Dokument39 SeitenA54 Peer Effect On Corporate Cash Holdings 20121108Missaoui IbtissemNoch keine Bewertungen

- (WWW - Entrance-Exam - Net) - Institute of Actuaries of India-Subject CT6 - Statistical Models Sample Paper 24Dokument10 Seiten(WWW - Entrance-Exam - Net) - Institute of Actuaries of India-Subject CT6 - Statistical Models Sample Paper 24Sachin BarthwalNoch keine Bewertungen

- Market Risk Var: Model-Building ApproachDokument38 SeitenMarket Risk Var: Model-Building ApproachElla Marie WicoNoch keine Bewertungen

- Lecture 3Dokument80 SeitenLecture 3Lee Li HengNoch keine Bewertungen

- Example: Investment Analysis Using A Legal Due Diligence Checklist by Ryland HamletDokument9 SeitenExample: Investment Analysis Using A Legal Due Diligence Checklist by Ryland HamletRyland Hamlet100% (13)

- 5fc9071aa4646025ba202bbb - YIELD - WhitepaperDokument37 Seiten5fc9071aa4646025ba202bbb - YIELD - WhitepaperamandotarbiraNoch keine Bewertungen

- Introduction of Insurance Fall 2023Dokument44 SeitenIntroduction of Insurance Fall 2023Tsz Mei WongNoch keine Bewertungen

- 2-Analysis of Risk Among AgribusnessDokument8 Seiten2-Analysis of Risk Among AgribusnessHilda Anugrah PutriNoch keine Bewertungen

- 4QFY19 Results - Financial - Statement PDFDokument26 Seiten4QFY19 Results - Financial - Statement PDFBubblyDeliciousNoch keine Bewertungen

- Risk and Capital BudgetingDokument12 SeitenRisk and Capital BudgetingImraanHossainAyaanNoch keine Bewertungen

- Suggested Answer Intro To Macro & SOL (Students Upload)Dokument35 SeitenSuggested Answer Intro To Macro & SOL (Students Upload)PotatoNoch keine Bewertungen

- Slides 6 - ESGDokument84 SeitenSlides 6 - ESGpierre.besnardNoch keine Bewertungen

- Jurnal Ekonomi 3Dokument19 SeitenJurnal Ekonomi 3phoebe buffayNoch keine Bewertungen

- Risk and Return: L RamprasathDokument6 SeitenRisk and Return: L RamprasathMayank RanjanNoch keine Bewertungen

- Digitalisation Promotes Adoption of Soft InformatiDokument33 SeitenDigitalisation Promotes Adoption of Soft InformatiJason MalikNoch keine Bewertungen

- SSRN Id3614875Dokument15 SeitenSSRN Id3614875ghjhghNoch keine Bewertungen

- SAC 603 Exam 19 - 20Dokument5 SeitenSAC 603 Exam 19 - 20Martin Kasuku100% (1)

- 5fe49edb67c2a75b62ff4713 - YIELD - Whitepaper - 201223Dokument37 Seiten5fe49edb67c2a75b62ff4713 - YIELD - Whitepaper - 201223Reggie ThorpeNoch keine Bewertungen

- Finance Research Letters: MD Akhtaruzzaman, Sabri Boubaker, Ahmet SensoyDokument20 SeitenFinance Research Letters: MD Akhtaruzzaman, Sabri Boubaker, Ahmet SensoyMariem RomdhaneNoch keine Bewertungen

- The Risk and Return of Impact Investing FundsDokument99 SeitenThe Risk and Return of Impact Investing FundsMatthieu LévêqueNoch keine Bewertungen

- 1 s2.0 S154461232100516X MainDokument6 Seiten1 s2.0 S154461232100516X MainIbrahim KhatatbehNoch keine Bewertungen

- Extreme Value Theory As A Risk Management Tool: Paul Embrechts, Sidney I. Resnick and Gennady SamorodnitskyDokument22 SeitenExtreme Value Theory As A Risk Management Tool: Paul Embrechts, Sidney I. Resnick and Gennady SamorodnitskylycancapitalNoch keine Bewertungen

- An Analysis of Financial Distress Accuracy Models in Indonesia Coal Mining IndustryDokument12 SeitenAn Analysis of Financial Distress Accuracy Models in Indonesia Coal Mining IndustryCharisma Rahmat PamungkasNoch keine Bewertungen

- Assessing Country-Level Privacy Risk ForDokument13 SeitenAssessing Country-Level Privacy Risk Forridho zynNoch keine Bewertungen

- CH 2 PDFDokument40 SeitenCH 2 PDFabaynewNoch keine Bewertungen

- How Does Value Relevance of Accounting Information React To Financial Crisis?Dokument9 SeitenHow Does Value Relevance of Accounting Information React To Financial Crisis?Viviane BarbosaNoch keine Bewertungen

- Preprint Not Peer Reviewed: Working Paper SeriesDokument28 SeitenPreprint Not Peer Reviewed: Working Paper SeriesYasser SadekNoch keine Bewertungen

- Research ArticleDokument10 SeitenResearch ArticleToque MasculinoNoch keine Bewertungen

- Running Head: Finance AssignmentDokument5 SeitenRunning Head: Finance AssignmentKashémNoch keine Bewertungen

- Banks and Interest Rate RiskDokument42 SeitenBanks and Interest Rate RiskckrishnaNoch keine Bewertungen

- Actuarial Models for Critical Illness Insurance ValuationDokument10 SeitenActuarial Models for Critical Illness Insurance ValuationBoris PolancoNoch keine Bewertungen

- Disentangling Types of Liquidity and Testing Limits To Arbitrage Theories in The CDS-bond BasisDokument27 SeitenDisentangling Types of Liquidity and Testing Limits To Arbitrage Theories in The CDS-bond BasisccandrastutiNoch keine Bewertungen

- Essentials of Private Real Estate International BrochureDokument16 SeitenEssentials of Private Real Estate International BrochureNNoch keine Bewertungen

- Skin in The Game Risk Analysis of Central CounterpartiesDokument51 SeitenSkin in The Game Risk Analysis of Central CounterpartiesirvinNoch keine Bewertungen

- De Oliveira and Montes (2021)Dokument23 SeitenDe Oliveira and Montes (2021)DiegoPachecoNoch keine Bewertungen

- The Role of Insurance in The Economy of The Republic of North MacedoniaDokument3 SeitenThe Role of Insurance in The Economy of The Republic of North MacedoniaEditor IJTSRDNoch keine Bewertungen

- Geopolitical Risk and InvestmentDokument18 SeitenGeopolitical Risk and InvestmentGia HânNoch keine Bewertungen

- 1 s2.0 S0969593123000367 MainDokument15 Seiten1 s2.0 S0969593123000367 MaincacaNoch keine Bewertungen

- Application of Compound Poisson Process in Pricing Catastrophe Bonds A Systematic Literature ReviewDokument20 SeitenApplication of Compound Poisson Process in Pricing Catastrophe Bonds A Systematic Literature ReviewEsa KhoirinnisaNoch keine Bewertungen

- The Econometrics of Asset Allocation: Carlo Favero Massimo GuidolinDokument20 SeitenThe Econometrics of Asset Allocation: Carlo Favero Massimo GuidolinBoldeanu Florin TeodorNoch keine Bewertungen

- Visualización, Identificación y Estimación en El Diseño de Estudio de Eventos de Panel Lineal (Disponible Sólo en Inglés)Dokument50 SeitenVisualización, Identificación y Estimación en El Diseño de Estudio de Eventos de Panel Lineal (Disponible Sólo en Inglés)Luis CalzadaNoch keine Bewertungen

- Why The Euro Will Rival The Dollar PDFDokument25 SeitenWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Statics and Dynamics in Socialist Economics PDFDokument19 SeitenStatics and Dynamics in Socialist Economics PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Claudia Jones Nuclear TestingDokument25 SeitenClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Beta Anomaly Tail Risk ApproachDokument104 SeitenBeta Anomaly Tail Risk ApproachDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Measures and Integration on Measurable SpacesDokument181 SeitenMeasures and Integration on Measurable SpacesDaniel Lee Eisenberg Jacobs100% (1)

- Continuity Change State of Process of Task ofDokument1 SeiteContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Cambridge University Press, International Labor and Working-Class, Inc. International Labor and Working-Class HistoryDokument13 SeitenCambridge University Press, International Labor and Working-Class, Inc. International Labor and Working-Class HistoryDaniel Lee Eisenberg Jacobs100% (1)

- Capital vs Labor: A History of Working Class StruggleDokument9 SeitenCapital vs Labor: A History of Working Class StruggleDaniel Lee Eisenberg Jacobs100% (1)

- Browder - The American SpiritDokument2 SeitenBrowder - The American SpiritDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- 1996 ElectionDokument84 Seiten1996 ElectionDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Necessary and Sufficient Conditions For Dynamic OptimizationDokument18 SeitenNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Notes On Forbidden RegressionsDokument5 SeitenNotes On Forbidden RegressionsZundaNoch keine Bewertungen

- Kant Conflict of FacultiesDokument11 SeitenKant Conflict of FacultiesDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Conference Group For Central European History of The American Historical AssociationDokument9 SeitenConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsNoch keine Bewertungen

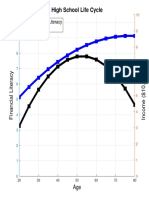

- High School Life Cycle: Financial Literacy IncomeDokument1 SeiteHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Karl Kautsky Republic and Social Democra PDFDokument4 SeitenKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Incentive Contracts in Delegated Portfolio ManagementDokument41 SeitenIncentive Contracts in Delegated Portfolio ManagementDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Marx's Critique of Political EconomyDokument5 SeitenMarx's Critique of Political EconomyDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Vanguard How Investors Select Advisors PDFDokument49 SeitenVanguard How Investors Select Advisors PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Time Is Money - Rational Life Cycle InertiaDokument39 SeitenTime Is Money - Rational Life Cycle InertiaDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- LTC Insurance Puzzle ExplainedDokument17 SeitenLTC Insurance Puzzle ExplainedDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- University of Oxford Draft-COVID-19-Model - 2020Dokument7 SeitenUniversity of Oxford Draft-COVID-19-Model - 2020Eric L. VanDussenNoch keine Bewertungen

- Individualization of Robo-AdviceDokument8 SeitenIndividualization of Robo-AdviceDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Vanguard How Investors Select Advisors PDFDokument49 SeitenVanguard How Investors Select Advisors PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- A Multiobjective Model For Passive Portfolio ManagementDokument32 SeitenA Multiobjective Model For Passive Portfolio ManagementDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Morningstar GammaDokument4 SeitenMorningstar GammaDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- FERC Economist Position Application by Daniel JacobsDokument1 SeiteFERC Economist Position Application by Daniel JacobsDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Genetic Algorithm in Economics and Agent Based ModelsDokument23 SeitenGenetic Algorithm in Economics and Agent Based ModelsDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- 09 MihatovDokument14 Seiten09 MihatovRaphael T. SprengerNoch keine Bewertungen

- Gpebook PDFDokument332 SeitenGpebook PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Problems Chapter 7Dokument9 SeitenProblems Chapter 7Trang Le0% (1)

- 1 Run EscapeDokument3 Seiten1 Run EscapeRJ Melgar BayotNoch keine Bewertungen

- UpsDokument3 SeitenUpsanandi.g9Noch keine Bewertungen

- Review - Udayana - Baiq Sonia Toin - GBDokument9 SeitenReview - Udayana - Baiq Sonia Toin - GBBaiq sonia ToinNoch keine Bewertungen

- Carlinsoskice Solutions ch06Dokument9 SeitenCarlinsoskice Solutions ch06Clara LustosaNoch keine Bewertungen

- FIN B488F - 2022 Autumn - Exam Formula Booklet - SVDokument7 SeitenFIN B488F - 2022 Autumn - Exam Formula Booklet - SVNile SethNoch keine Bewertungen

- Capital MarketDokument8 SeitenCapital Marketkomal_studentNoch keine Bewertungen

- Indigo PaperDokument75 SeitenIndigo Papernxoxoxrx xxxNoch keine Bewertungen

- Card Monthly Summary 10072022023013Dokument5 SeitenCard Monthly Summary 10072022023013Marsha BaconNoch keine Bewertungen

- Inflation: Its Causes, Effects, and Social Costs: MacroeconomicsDokument61 SeitenInflation: Its Causes, Effects, and Social Costs: MacroeconomicsTai612Noch keine Bewertungen

- Salam & Parallel Salam Transactions-CH.7Dokument36 SeitenSalam & Parallel Salam Transactions-CH.7Yusuf Hussein0% (1)

- NI Act 1881Dokument11 SeitenNI Act 1881AngelinaGuptaNoch keine Bewertungen

- Working Report 2022 30 June English Single Page Artwork Low ResDokument36 SeitenWorking Report 2022 30 June English Single Page Artwork Low ResAparajita RB SinghNoch keine Bewertungen

- CLO PrimerDokument31 SeitenCLO PrimerdgnyNoch keine Bewertungen

- PF Withdrawal Application (Sample Copy)Dokument5 SeitenPF Withdrawal Application (Sample Copy)Ashok Mahanta100% (1)

- Managing Working CapitalDokument16 SeitenManaging Working Capitalsalehin1969Noch keine Bewertungen

- How Warren Buffett Interprets Financial Statements - Old School ValueDokument30 SeitenHow Warren Buffett Interprets Financial Statements - Old School ValueAnant JainNoch keine Bewertungen

- SCF WorksheetDokument19 SeitenSCF WorksheetAngelo Gian CoNoch keine Bewertungen

- Simple Interest Formula and ProblemsDokument4 SeitenSimple Interest Formula and ProblemsTAภaу ЎALLaмᎥlliNoch keine Bewertungen

- Practical Investment Management by Robert.A.Strong Slides ch08Dokument28 SeitenPractical Investment Management by Robert.A.Strong Slides ch08mzqaceNoch keine Bewertungen

- Corporate Finance DecisionsDokument3 SeitenCorporate Finance DecisionsPua Suan Jin RobinNoch keine Bewertungen

- Inflation Case Studies 500Dokument3 SeitenInflation Case Studies 500Navita SinghNoch keine Bewertungen

- BPO Frequently Asked Questions Corporates May2018 FinalDokument10 SeitenBPO Frequently Asked Questions Corporates May2018 FinalMuthu SelvanNoch keine Bewertungen

- Chapter 20 - Audit of NBFC PDFDokument4 SeitenChapter 20 - Audit of NBFC PDFRakhi SinghalNoch keine Bewertungen

- Internal Assignment of Financial & Accounting ManagementDokument26 SeitenInternal Assignment of Financial & Accounting ManagementBasudev SharmaNoch keine Bewertungen

- Account StatementDokument2 SeitenAccount StatementgobeyondskyNoch keine Bewertungen

- Security Analysis GuideDokument11 SeitenSecurity Analysis GuideAshley WintersNoch keine Bewertungen

- SECURITIZATION AUDIT - A Waste of Foreclosure Victim MoneyDokument9 SeitenSECURITIZATION AUDIT - A Waste of Foreclosure Victim MoneyBob Hurt50% (2)

- EMA-RSI-MACD 15min System - ProfitF - Website For Forex, Binary Options Traders (Helpful Reviews)Dokument5 SeitenEMA-RSI-MACD 15min System - ProfitF - Website For Forex, Binary Options Traders (Helpful Reviews)Sonarat MoulnengNoch keine Bewertungen