Das könnte Ihnen auch gefallen

- Cognizant Technology SolutionsDokument11 SeitenCognizant Technology SolutionsMj PayalNoch keine Bewertungen

- I 04.05studentDokument22 SeitenI 04.05studentFaizan Yousuf67% (3)

- Economics 100 Quiz 1Dokument15 SeitenEconomics 100 Quiz 1Ayaz AliNoch keine Bewertungen

- Kalyani Powertrain Ltd-4Nov2022Dokument32 SeitenKalyani Powertrain Ltd-4Nov2022Sreekanth DevarasettyNoch keine Bewertungen

- Business Plan and Entrepreneurship Toolkit - Overview and ApproachDokument48 SeitenBusiness Plan and Entrepreneurship Toolkit - Overview and Approachtagay100% (2)

- Atlantic Case PricingDokument3 SeitenAtlantic Case PricingShivraj KarthikNoch keine Bewertungen

- NTPC Financial Statement AnalysisDokument19 SeitenNTPC Financial Statement AnalysisprahladagarwalNoch keine Bewertungen

- Trappist Case AnalysisDokument6 SeitenTrappist Case AnalysisSalve Babar100% (1)

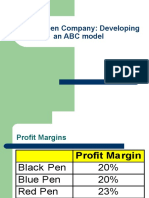

- Classic Pen Company: Developing An ABC ModelDokument22 SeitenClassic Pen Company: Developing An ABC Modeljk kumarNoch keine Bewertungen

- Mba ZC417 Ec-3m First Sem 2018-2019Dokument6 SeitenMba ZC417 Ec-3m First Sem 2018-2019shiintuNoch keine Bewertungen

- Cost Sheet For The Month of January: TotalDokument9 SeitenCost Sheet For The Month of January: TotalgauravpalgarimapalNoch keine Bewertungen

- AF304 Auditing Tutorial 5 AnswersDokument9 SeitenAF304 Auditing Tutorial 5 AnswersShivneel NaiduNoch keine Bewertungen

- 2g Scam ProjectDokument24 Seiten2g Scam Projectk_suryaNoch keine Bewertungen

- WCM QuizDokument33 SeitenWCM QuizbalaNoch keine Bewertungen

- Report On The Coal AnalysisDokument10 SeitenReport On The Coal AnalysisumerNoch keine Bewertungen

- France TelecomDokument17 SeitenFrance Telecomabhi2djNoch keine Bewertungen

- Advantages and DisadvantagesDokument5 SeitenAdvantages and DisadvantagesOmkar KulkarniNoch keine Bewertungen

- Analysis of Indian Luggage Market and Key PlayersDokument9 SeitenAnalysis of Indian Luggage Market and Key PlayersSurya RanaNoch keine Bewertungen

- How Kohinoor Chemicals Indusries Ltd. Maintain Its Old Lagacy Facing Intense Competiton in The MarketDokument14 SeitenHow Kohinoor Chemicals Indusries Ltd. Maintain Its Old Lagacy Facing Intense Competiton in The Market0302038Noch keine Bewertungen

- Aaker and Keller: Key HighlightsDokument1 SeiteAaker and Keller: Key HighlightsShyamal VermaNoch keine Bewertungen

- Igcar RecruitmentDokument13 SeitenIgcar RecruitmentDeepak Kumar VasudevanNoch keine Bewertungen

- The Rise and Fall of Kingfisher Airlines: The Microeconomic FactorsDokument11 SeitenThe Rise and Fall of Kingfisher Airlines: The Microeconomic FactorsVinodshankar BhatNoch keine Bewertungen

- Butyl AcetateDokument8 SeitenButyl AcetateGovindanayagi PattabiramanNoch keine Bewertungen

- Anoop GomechanicDokument3 SeitenAnoop GomechanicANOOP SHARMANoch keine Bewertungen

- BEW case study: Loan repayment optionsDokument3 SeitenBEW case study: Loan repayment optionsjohnleh1733% (3)

- SIRP Report - Jainam & KavishDokument24 SeitenSIRP Report - Jainam & KavishKavish JainNoch keine Bewertungen

- Summer Internship Project-NishantDokument80 SeitenSummer Internship Project-Nishantnishant singhNoch keine Bewertungen

- Beta Case Study (Nirbhay Chauhan)Dokument10 SeitenBeta Case Study (Nirbhay Chauhan)Nirbhay ChauhanNoch keine Bewertungen

- 820001-Cost and Management AccountingDokument4 Seiten820001-Cost and Management AccountingsuchjazzNoch keine Bewertungen

- HBK - Fatigue and Durability ExplainedDokument111 SeitenHBK - Fatigue and Durability ExplainedsengozkNoch keine Bewertungen

- 355 Tata Structura Brochure PDFDokument13 Seiten355 Tata Structura Brochure PDFAbhi JainNoch keine Bewertungen

- Case Study Tata SteelDokument3 SeitenCase Study Tata SteelAnkurNoch keine Bewertungen

- Luminus Education: - Assignment Brief (RQF)Dokument15 SeitenLuminus Education: - Assignment Brief (RQF)Tawfiq Nassoura0% (1)

- EOQDokument15 SeitenEOQPrajaktaNoch keine Bewertungen

- Recruitment and Selection in Multinational CorporationDokument18 SeitenRecruitment and Selection in Multinational CorporationAbhishek Mishra100% (3)

- A1 10BM60005Dokument13 SeitenA1 10BM60005amit_dce100% (2)

- Assignment On ABCDokument5 SeitenAssignment On ABCRaghav MehraNoch keine Bewertungen

- HMT Marketing MixDokument67 SeitenHMT Marketing Mixakashsadoriya5477Noch keine Bewertungen

- 2 CRM AT TATA SKY - Group 2Dokument17 Seiten2 CRM AT TATA SKY - Group 2manmeet kaurNoch keine Bewertungen

- Valuing Project AchieveDokument2 SeitenValuing Project AchieveRahul TiwariNoch keine Bewertungen

- Balaji Corporate PresentationDokument34 SeitenBalaji Corporate PresentationPrashant PatilNoch keine Bewertungen

- Audit Report Sweets Factory (6th July2021) Unannounced - FinalDokument25 SeitenAudit Report Sweets Factory (6th July2021) Unannounced - Finalsajid waqasNoch keine Bewertungen

- Porter's Five Competitive Forces: Recommended ReadingDokument6 SeitenPorter's Five Competitive Forces: Recommended ReadingJadric CummingsNoch keine Bewertungen

- Project Reoprt On JSW SteelsDokument30 SeitenProject Reoprt On JSW SteelsSakthi Krishnan100% (1)

- Industry Analysis of MRF and JK TyresDokument9 SeitenIndustry Analysis of MRF and JK TyresDamanpreet singhNoch keine Bewertungen

- 102B - Business Organisation & Office ManagementDokument22 Seiten102B - Business Organisation & Office ManagementAnonymous WtjVcZCgNoch keine Bewertungen

- Consumer Perception of Emerging Smartphone Brand XiaomiDokument16 SeitenConsumer Perception of Emerging Smartphone Brand XiaomiAbhishek MehtaNoch keine Bewertungen

- Consumer Satisfaction Towards LG TelevisionsDokument75 SeitenConsumer Satisfaction Towards LG TelevisionsSubramanya DgNoch keine Bewertungen

- EtopDokument7 SeitenEtopAnilBahugunaNoch keine Bewertungen

- NSU 11-1 Eco 101 - Practice Question 1Dokument3 SeitenNSU 11-1 Eco 101 - Practice Question 1Asif Abedin Einstein100% (1)

- After Sales Service - ATHERDokument12 SeitenAfter Sales Service - ATHERPrasath NagendraNoch keine Bewertungen

- Entrepreneurship Development CIA 1 Component 2 RatikDokument4 SeitenEntrepreneurship Development CIA 1 Component 2 RatikRatik RebelloNoch keine Bewertungen

- M3 - Valuation Question SetDokument13 SeitenM3 - Valuation Question SetHetviNoch keine Bewertungen

- HMT CompleteDokument34 SeitenHMT CompletemundawalaNoch keine Bewertungen

- Operation Management ASSIGNMENT 02Dokument5 SeitenOperation Management ASSIGNMENT 02Saumya JaiswalNoch keine Bewertungen

- Integrated Approach For Supply ChainDokument9 SeitenIntegrated Approach For Supply ChainSai GaneshNoch keine Bewertungen

- A MM1 Assignment1Dokument12 SeitenA MM1 Assignment1Abhijeet singhNoch keine Bewertungen

- Exam 2 Guidelines 2019Dokument6 SeitenExam 2 Guidelines 2019Sri VeludandiNoch keine Bewertungen

- Cost SheetDokument9 SeitenCost Sheetsdiv92Noch keine Bewertungen

- Avenue Dmart PDFDokument74 SeitenAvenue Dmart PDFdarshanmadeNoch keine Bewertungen

- CH - 11 (Internal Analysis)Dokument21 SeitenCH - 11 (Internal Analysis)Pankaj SinghNoch keine Bewertungen

- Vodafone India Evaluation and Entry StrategyDokument15 SeitenVodafone India Evaluation and Entry StrategySadia AnumNoch keine Bewertungen

- Acc Assign Sem 2Dokument7 SeitenAcc Assign Sem 2xuanylimNoch keine Bewertungen

- Cost Accounting Exam PaperDokument5 SeitenCost Accounting Exam PaperAhmed EltayebNoch keine Bewertungen

- Factor Analysis Preview - Rev1Dokument42 SeitenFactor Analysis Preview - Rev1abcd_123425Noch keine Bewertungen

- Factor Analysis Preview - Rev1Dokument42 SeitenFactor Analysis Preview - Rev1abcd_123425Noch keine Bewertungen

- Principal Component Analysis (PCA) FinalDokument37 SeitenPrincipal Component Analysis (PCA) Finalabcd_123425Noch keine Bewertungen

- Factor Analysis Preview - Rev1Dokument8 SeitenFactor Analysis Preview - Rev1abcd_123425Noch keine Bewertungen

- The Mavericks - Moody's Case Study - FinalDokument67 SeitenThe Mavericks - Moody's Case Study - Finalabcd_123425Noch keine Bewertungen

- The Hindu Review July 2017Dokument21 SeitenThe Hindu Review July 2017RamanNoch keine Bewertungen

- The Hindu Review October 2017Dokument18 SeitenThe Hindu Review October 2017Kaushik SreenivasNoch keine Bewertungen

- SMDokument306 SeitenSMabcd_123425Noch keine Bewertungen

- The Hindu Review June 2017Dokument23 SeitenThe Hindu Review June 2017SURYA TAMANGNoch keine Bewertungen

- WSMADokument9 SeitenWSMAabcd_123425Noch keine Bewertungen

- The Hindu Review August 2017Dokument23 SeitenThe Hindu Review August 2017kanchanagrawal91Noch keine Bewertungen

- The Hindu Review September 2017Dokument21 SeitenThe Hindu Review September 2017rajanNoch keine Bewertungen

- The Hindu Review 2017 PDFDokument16 SeitenThe Hindu Review 2017 PDFvijayNoch keine Bewertungen

- Current Affairs Study PDF - September 2017 by AffairsCloud PDFDokument169 SeitenCurrent Affairs Study PDF - September 2017 by AffairsCloud PDFSaurav ShabbyNoch keine Bewertungen

- The Hindu Review April PDFDokument14 SeitenThe Hindu Review April PDFgbgbkrishnaNoch keine Bewertungen

- Current Affairs Study PDF - October 2017 by AffairsCloudDokument168 SeitenCurrent Affairs Study PDF - October 2017 by AffairsCloudHitesh KumarNoch keine Bewertungen

- Current Affairs For 2017Dokument160 SeitenCurrent Affairs For 2017anarchanonNoch keine Bewertungen

- Hindu Review February (English)Dokument17 SeitenHindu Review February (English)srinivasNoch keine Bewertungen

- Current Affairs Study PDF - June 2017 by AffairsCloudDokument162 SeitenCurrent Affairs Study PDF - June 2017 by AffairsCloudMohit AryaNoch keine Bewertungen

- August 2017 PDFDokument165 SeitenAugust 2017 PDFVicky GunasekaranNoch keine Bewertungen

- Hindu Review March (English)Dokument13 SeitenHindu Review March (English)Vipin BabuNoch keine Bewertungen

- Current Affairs Study PDF - March 2017 by AffairsCloudDokument169 SeitenCurrent Affairs Study PDF - March 2017 by AffairsCloudabcd_123425Noch keine Bewertungen

- 2017 Awards by AffairsCloud PDFDokument22 Seiten2017 Awards by AffairsCloud PDFRam RamNoch keine Bewertungen

- Current Affairs Study PDF - May 2017 by AffairsCloudDokument151 SeitenCurrent Affairs Study PDF - May 2017 by AffairsCloudGhagniSinghaniaNoch keine Bewertungen

- 2017 Static GK Capsule by AffairsCloud - V4 PDFDokument109 Seiten2017 Static GK Capsule by AffairsCloud - V4 PDFGurpreet GabaNoch keine Bewertungen

- Current Affairs Study PDF - July 2017 by AffairsCloudDokument172 SeitenCurrent Affairs Study PDF - July 2017 by AffairsCloudabcd_123425Noch keine Bewertungen

- Government Schemes 2017 by AffairsCloudDokument48 SeitenGovernment Schemes 2017 by AffairsCloudatultirkeyNoch keine Bewertungen

- 2017 Appointments by AffairsCloudDokument14 Seiten2017 Appointments by AffairsCloudabcd_123425Noch keine Bewertungen

- 2017 List of Summits & Conferences (Jan - Oct)Dokument16 Seiten2017 List of Summits & Conferences (Jan - Oct)abcd_123425Noch keine Bewertungen

- Oregon Public Employees Retirement System Aug. 2012 Board Meeting PacketDokument138 SeitenOregon Public Employees Retirement System Aug. 2012 Board Meeting PacketStatesman JournalNoch keine Bewertungen

- Assignment of Advertisement and PromotionDokument16 SeitenAssignment of Advertisement and PromotionMoin UddinNoch keine Bewertungen

- Case Interview - Prep - Frameworks PDFDokument14 SeitenCase Interview - Prep - Frameworks PDFProdigi ConsultingNoch keine Bewertungen

- Quiz6 MEAcctg1102 - 91 E0Dokument17 SeitenQuiz6 MEAcctg1102 - 91 E0Saeym SegoviaNoch keine Bewertungen

- Module-2 Application of Demand and SupplyDokument19 SeitenModule-2 Application of Demand and Supplyha? hakdogNoch keine Bewertungen

- Chapter 6 PDFDokument28 SeitenChapter 6 PDFDiva CarissaNoch keine Bewertungen

- 1.4 Risk+Management:+A+Helicopter+View+风险管理:从一个宏观、全局的角度看Dokument17 Seiten1.4 Risk+Management:+A+Helicopter+View+风险管理:从一个宏观、全局的角度看James JiangNoch keine Bewertungen

- Chapter 3 Homework Chapter 3 HomeworkDokument8 SeitenChapter 3 Homework Chapter 3 HomeworkPhương NguyễnNoch keine Bewertungen

- Acctg13 PPE ProblemsDokument4 SeitenAcctg13 PPE ProblemsKristel Keith NievaNoch keine Bewertungen

- Chapter 12 Managing Marketing Communications - WEEK 7Dokument21 SeitenChapter 12 Managing Marketing Communications - WEEK 7abe onimushaNoch keine Bewertungen

- Lavigne RoofDokument7 SeitenLavigne Roofusmanf87Noch keine Bewertungen

- Distribution Management ReviewerDokument11 SeitenDistribution Management ReviewerSALEM, JUSTINE WINSTON DS.Noch keine Bewertungen

- Ucsp Week 1 LessonDokument2 SeitenUcsp Week 1 Lessonbless HamiNoch keine Bewertungen

- Quiz 2 Chpts 3 4Dokument14 SeitenQuiz 2 Chpts 3 4Jayden Galing100% (1)

- Internal Control Reviewer3Dokument12 SeitenInternal Control Reviewer3Lon DiazNoch keine Bewertungen

- Banking - Citi - Original File1Dokument16 SeitenBanking - Citi - Original File1Xiaochen TangNoch keine Bewertungen

- LISTA AGENTIILOR DE TURISM LICENTIATE Actualizare 14.08.2018Dokument356 SeitenLISTA AGENTIILOR DE TURISM LICENTIATE Actualizare 14.08.2018Năstasă Alexandru-GeorgeNoch keine Bewertungen

- The Metro CompanyDokument1 SeiteThe Metro CompanyTk KimNoch keine Bewertungen

- Assignment 1Dokument4 SeitenAssignment 1ABHISHEK TRIPATHINoch keine Bewertungen

- Marketing Research of MiloDokument5 SeitenMarketing Research of MiloAsha100% (1)

- A Close Look at China's Revenue-Sharing Platforms - Yunji, Beidian and Global Scanner - WalktheChatDokument10 SeitenA Close Look at China's Revenue-Sharing Platforms - Yunji, Beidian and Global Scanner - WalktheChatAkshay ChandorkarNoch keine Bewertungen

- Kishor Thesis PDFDokument65 SeitenKishor Thesis PDFKishor KhatikNoch keine Bewertungen

- Pcoa 008 - Intermediate Accounting Ii Learning OutcomesDokument19 SeitenPcoa 008 - Intermediate Accounting Ii Learning OutcomesNicole LucasNoch keine Bewertungen

- Principals of Marketing BUS 206Dokument33 SeitenPrincipals of Marketing BUS 206Sahal Bin SaadNoch keine Bewertungen

- Case Study 1: Actions to Improve RBG Cookie PerformanceDokument6 SeitenCase Study 1: Actions to Improve RBG Cookie PerformanceJeffrey O'LearyNoch keine Bewertungen

- Ap - Cost of Goods SoldDokument2 SeitenAp - Cost of Goods SoldRoby Renna EstoqueNoch keine Bewertungen