Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- SMChap 013Dokument49 SeitenSMChap 013testbank100% (5)

- Calpine RGGI LawsuitDokument208 SeitenCalpine RGGI LawsuitCommonwealth FoundationNoch keine Bewertungen

- Commonwealth Foundation Testimony On RGGI 10.28.19Dokument3 SeitenCommonwealth Foundation Testimony On RGGI 10.28.19Commonwealth FoundationNoch keine Bewertungen

- Constitutional and Legal Requirements of A Balanced Budget in PennsylvaniaDokument1 SeiteConstitutional and Legal Requirements of A Balanced Budget in PennsylvaniaCommonwealth FoundationNoch keine Bewertungen

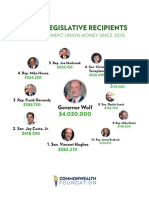

- Top 10 Legislative Recipients of Union Political MoneyDokument1 SeiteTop 10 Legislative Recipients of Union Political MoneyCommonwealth FoundationNoch keine Bewertungen

- Pennsylvania Government Flow ChartDokument1 SeitePennsylvania Government Flow ChartCommonwealth FoundationNoch keine Bewertungen

- Memo in Support of DOC and PBPP MergerDokument2 SeitenMemo in Support of DOC and PBPP MergerCommonwealth FoundationNoch keine Bewertungen

- UFCW 1776 LetterDokument1 SeiteUFCW 1776 LetterCommonwealth FoundationNoch keine Bewertungen

- Obamacare Has Harmed Pennsylvania FamiliesDokument2 SeitenObamacare Has Harmed Pennsylvania FamiliesCommonwealth FoundationNoch keine Bewertungen

- SAT Scores by State 2015Dokument2 SeitenSAT Scores by State 2015Commonwealth FoundationNoch keine Bewertungen

- Pennsylvanians Flee From High TaxesDokument4 SeitenPennsylvanians Flee From High TaxesCommonwealth FoundationNoch keine Bewertungen

- Charter Testimony October 2016Dokument6 SeitenCharter Testimony October 2016Commonwealth FoundationNoch keine Bewertungen

- Pennsylvania Sat 1986-2011 (Intern's Conflicted Copy 2016-06-16)Dokument13 SeitenPennsylvania Sat 1986-2011 (Intern's Conflicted Copy 2016-06-16)Commonwealth FoundationNoch keine Bewertungen

- Vape Tax VictimsDokument2 SeitenVape Tax VictimsCommonwealth FoundationNoch keine Bewertungen

- How Workers Are Forced To Fund Attack AdsDokument2 SeitenHow Workers Are Forced To Fund Attack AdsCommonwealth FoundationNoch keine Bewertungen

- What Is Paycheck Protection?Dokument1 SeiteWhat Is Paycheck Protection?Commonwealth FoundationNoch keine Bewertungen

- Mary Isenhour Letter To PERCDokument2 SeitenMary Isenhour Letter To PERCCommonwealth FoundationNoch keine Bewertungen

- AFSCME Local 2528 PAC SolicitationDokument3 SeitenAFSCME Local 2528 PAC SolicitationCommonwealth FoundationNoch keine Bewertungen

- PA Pension ReformDokument31 SeitenPA Pension ReformCommonwealth FoundationNoch keine Bewertungen

- Pennsylvania's Pension Crisis: Facts and MythsDokument2 SeitenPennsylvania's Pension Crisis: Facts and MythsCommonwealth FoundationNoch keine Bewertungen

- Commonwealth Foundation RTKDokument10 SeitenCommonwealth Foundation RTKCommonwealth FoundationNoch keine Bewertungen

- DPW Welfare Waste, Fraud & Abuse SavingsDokument2 SeitenDPW Welfare Waste, Fraud & Abuse SavingsCommonwealth FoundationNoch keine Bewertungen

- Patient-Centered Medicaid Reform ActDokument14 SeitenPatient-Centered Medicaid Reform ActCommonwealth FoundationNoch keine Bewertungen

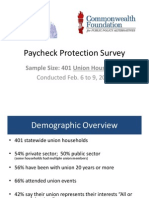

- Paycheck Protection Survey: Sample Size: 401 Union HouseholdsDokument7 SeitenPaycheck Protection Survey: Sample Size: 401 Union HouseholdsCommonwealth FoundationNoch keine Bewertungen

- Public Pensions: Past, Present and FutureDokument2 SeitenPublic Pensions: Past, Present and FutureCommonwealth FoundationNoch keine Bewertungen

- Unsinkable: The True Story of Pennsylvania's Sinking Pension SystemDokument1 SeiteUnsinkable: The True Story of Pennsylvania's Sinking Pension SystemCommonwealth FoundationNoch keine Bewertungen

- Letter To Corbett: Reject Medicaid ExpansionDokument4 SeitenLetter To Corbett: Reject Medicaid ExpansionCommonwealth FoundationNoch keine Bewertungen

- Liquor Privatization Facts and MythsDokument2 SeitenLiquor Privatization Facts and MythsCommonwealth FoundationNoch keine Bewertungen

- Social Impacts of Liquor PrivatizationDokument6 SeitenSocial Impacts of Liquor PrivatizationCommonwealth FoundationNoch keine Bewertungen

- FM3 Privatization PollDokument15 SeitenFM3 Privatization PollCommonwealth FoundationNoch keine Bewertungen

- Comparison ChartDokument1 SeiteComparison ChartCommonwealth FoundationNoch keine Bewertungen

- Accounting For Pensions and Postretirement Benefits: Assignment Classification Table (By Topic)Dokument71 SeitenAccounting For Pensions and Postretirement Benefits: Assignment Classification Table (By Topic)Andreas AndreanoNoch keine Bewertungen

- Accounting and Reporting by Retirement Benefit Plans: Malaysian Financial Reporting Standard 126Dokument14 SeitenAccounting and Reporting by Retirement Benefit Plans: Malaysian Financial Reporting Standard 126Eka MemengNoch keine Bewertungen

- CIFC Exam Prep Live Webinar Practice Questions 2018 v.2 69276 1 25 2018 1254Dokument17 SeitenCIFC Exam Prep Live Webinar Practice Questions 2018 v.2 69276 1 25 2018 1254Anup KhanalNoch keine Bewertungen

- Risk Management Assignment 3: President University Cikarang UtaraDokument7 SeitenRisk Management Assignment 3: President University Cikarang UtaraAlya RamadhaniNoch keine Bewertungen

- Advanced Financial Accounting Under IFRSDokument57 SeitenAdvanced Financial Accounting Under IFRSAlexandra Mihaela TanaseNoch keine Bewertungen

- Faculty WelfareDokument6 SeitenFaculty Welfaremerin sunilNoch keine Bewertungen

- Chapter 14Dokument23 SeitenChapter 14YolandaNoch keine Bewertungen

- Federal RetirementDokument50 SeitenFederal RetirementFedSmith Inc.100% (1)

- Employee Benefits Pas 19Dokument44 SeitenEmployee Benefits Pas 19Joanne Rey OcanaNoch keine Bewertungen

- IND 14 CHP 13 2 Homework Sol RETIREMENT Combined 2014Dokument8 SeitenIND 14 CHP 13 2 Homework Sol RETIREMENT Combined 2014Nada Mucho100% (1)

- Employee BenefitsDokument83 SeitenEmployee BenefitsArlene Rose GonzaloNoch keine Bewertungen

- Actuarial Glossary PDFDokument18 SeitenActuarial Glossary PDFmiguelNoch keine Bewertungen

- NZF PensionGuide2020Dokument12 SeitenNZF PensionGuide2020umairNoch keine Bewertungen

- Denga Report CurrentDokument38 SeitenDenga Report CurrentAnesu Nathan ChiwaridzoNoch keine Bewertungen

- Analysis of The Survival of Pension Funds During Hyperinflationary Periods in ZimbabweDokument97 SeitenAnalysis of The Survival of Pension Funds During Hyperinflationary Periods in ZimbabweTatenda Takie TakaidzaNoch keine Bewertungen

- Defined Contribution Plan Summary DescriptionDokument20 SeitenDefined Contribution Plan Summary DescriptionJorge Monroy VillapuduaNoch keine Bewertungen

- EB Handouts 1Dokument4 SeitenEB Handouts 1John Vicente BalanquitNoch keine Bewertungen

- Topic 13 - Retirement PlanningDokument54 SeitenTopic 13 - Retirement PlanningArun GhatanNoch keine Bewertungen

- Casey Quirk (2008) - The New GatekeepersDokument30 SeitenCasey Quirk (2008) - The New Gatekeeperssawilson1Noch keine Bewertungen

- AC 2202 CHAPTER 17 NotesDokument8 SeitenAC 2202 CHAPTER 17 NotesKemuel TantuanNoch keine Bewertungen

- Employee BenefitDokument32 SeitenEmployee BenefitnatiNoch keine Bewertungen

- RMC No. 13-2024 - Accounting and Tax Treatment of Retirement Benefits ExpenseDokument10 SeitenRMC No. 13-2024 - Accounting and Tax Treatment of Retirement Benefits ExpenseAnostasia NemusNoch keine Bewertungen

- Ch.20 SolDokument43 SeitenCh.20 Solkokmunwai717Noch keine Bewertungen

- Designing and Administering BenefitsDokument21 SeitenDesigning and Administering Benefitsnitinmt100% (1)

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODokument38 SeitenEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNoch keine Bewertungen

- Topic 1 - Pension SystemDokument11 SeitenTopic 1 - Pension SystemfadeNoch keine Bewertungen

- Insurance CompaniesDokument11 SeitenInsurance CompaniesPricia AbellaNoch keine Bewertungen

- ObligationDokument2 SeitenObligationJustine Airra OndoyNoch keine Bewertungen

- Handouts PDFDokument129 SeitenHandouts PDFRomulus GarciaNoch keine Bewertungen