Das könnte Ihnen auch gefallen

- CORRELATION and REGRESSIONDokument19 SeitenCORRELATION and REGRESSIONcharlene quiambaoNoch keine Bewertungen

- Correlation AnalysisDokument51 SeitenCorrelation Analysisjjjjkjhkhjkhjkjk100% (1)

- HP Scanjet N9120 (Service Manual) PDFDokument394 SeitenHP Scanjet N9120 (Service Manual) PDFcamilohto80% (5)

- Dayco-Timing Belt Training - Entrenamiento Correa DentadaDokument9 SeitenDayco-Timing Belt Training - Entrenamiento Correa DentadaDeiby CeleminNoch keine Bewertungen

- Regression AnalysisDokument43 SeitenRegression AnalysisPRIYADARSHI GOURAV100% (1)

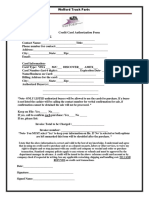

- Credit Card Authorization Form WoffordDokument1 SeiteCredit Card Authorization Form WoffordRaúl Enmanuel Capellan PeñaNoch keine Bewertungen

- CorrelationDokument29 SeitenCorrelationDevansh DwivediNoch keine Bewertungen

- 06-Correlation & Simple Regression - Nov 1Dokument124 Seiten06-Correlation & Simple Regression - Nov 1Abdulaziz AlzahraniNoch keine Bewertungen

- Admission: North South University (NSU) Question Bank Summer 2019Dokument10 SeitenAdmission: North South University (NSU) Question Bank Summer 2019Mahmoud Hasan100% (7)

- Teachers Guide Lower Secondary Science PDFDokument141 SeitenTeachers Guide Lower Secondary Science PDFNuzhat IbrahimNoch keine Bewertungen

- Career Orientation QuestionnaireDokument5 SeitenCareer Orientation QuestionnaireApple May100% (1)

- SD-NOC-MAR-202 - Rev00 Transfer of Personnel at Offshore FacilitiesDokument33 SeitenSD-NOC-MAR-202 - Rev00 Transfer of Personnel at Offshore Facilitiestho03103261100% (1)

- Regression AnalysisDokument30 SeitenRegression AnalysisAmir Sadeeq100% (1)

- Piaggio MP3 300 Ibrido LT MY 2010 (En)Dokument412 SeitenPiaggio MP3 300 Ibrido LT MY 2010 (En)Manualles100% (3)

- Introduction To Risk ManagementDokument41 SeitenIntroduction To Risk ManagementIvania CorbafoNoch keine Bewertungen

- MATH 121 (Chapter 10) - Correlation & RegressionDokument30 SeitenMATH 121 (Chapter 10) - Correlation & RegressionpotsuNoch keine Bewertungen

- Lecture 4 - Correlation and RegressionDokument35 SeitenLecture 4 - Correlation and Regressionmanuelmbiawa30Noch keine Bewertungen

- M. Amir Hossain PHD: Course No: Emba 502: Business Mathematics and StatisticsDokument31 SeitenM. Amir Hossain PHD: Course No: Emba 502: Business Mathematics and StatisticsSP VetNoch keine Bewertungen

- Oe Statistics NotesDokument32 SeitenOe Statistics NotesFirdoseNoch keine Bewertungen

- LP-III Lab ManualDokument49 SeitenLP-III Lab ManualNihal GujarNoch keine Bewertungen

- Lecture10 - SIMPLE LINEAR REGRESSIONDokument13 SeitenLecture10 - SIMPLE LINEAR REGRESSIONHiền NguyễnNoch keine Bewertungen

- Complete Business Statistics: Simple Linear Regression and CorrelationDokument50 SeitenComplete Business Statistics: Simple Linear Regression and CorrelationAli ElattarNoch keine Bewertungen

- Regression and CorrelationDokument66 SeitenRegression and CorrelationSIDDHANT KARMARKAR SIDDHANT KARMARKARNoch keine Bewertungen

- FsgsDokument28 SeitenFsgsRagul SNoch keine Bewertungen

- Session 15 Regression and CorrelationDokument66 SeitenSession 15 Regression and CorrelationAmit AdmuneNoch keine Bewertungen

- QuantitativeDokument90 SeitenQuantitativeSen RinaNoch keine Bewertungen

- Simple Linear Regression and CorrelationDokument31 SeitenSimple Linear Regression and CorrelationMohammed KashoobNoch keine Bewertungen

- Lecture 10Dokument33 SeitenLecture 10anushkaNoch keine Bewertungen

- Correlation Analysis: Concept of Univariate, Bivariate DataDokument48 SeitenCorrelation Analysis: Concept of Univariate, Bivariate DataPanma PatelNoch keine Bewertungen

- Statistics For Business STAT130: Unit 8: Correlation and Regression AnalysisDokument56 SeitenStatistics For Business STAT130: Unit 8: Correlation and Regression AnalysisUsmanNoch keine Bewertungen

- Correlation and RegressionDokument6 SeitenCorrelation and RegressionMr. JahirNoch keine Bewertungen

- BUSINESS STATISTICS: Simple Linear Regression and CorrelationDokument55 SeitenBUSINESS STATISTICS: Simple Linear Regression and CorrelationLaurence Rue AudineNoch keine Bewertungen

- BUSN 2429 Chapter 14 Correlation and Single Regression ModelDokument85 SeitenBUSN 2429 Chapter 14 Correlation and Single Regression ModelAwais SadaqatNoch keine Bewertungen

- Simple Linear Regression and Correlation 568a5ac2ce9b3Dokument31 SeitenSimple Linear Regression and Correlation 568a5ac2ce9b3Adrian RegimenNoch keine Bewertungen

- CH 08Dokument13 SeitenCH 08api-283519975Noch keine Bewertungen

- Reading 11: Correlation and Regression: S S Y X Cov RDokument24 SeitenReading 11: Correlation and Regression: S S Y X Cov Rd ddNoch keine Bewertungen

- Linear Regression and Correlation: Mcgraw Hill/IrwinDokument37 SeitenLinear Regression and Correlation: Mcgraw Hill/IrwinGabriella Widya ANoch keine Bewertungen

- Business Mathematics & StatisticsDokument31 SeitenBusiness Mathematics & StatisticszainaliNoch keine Bewertungen

- Linear Regression - Six Sigma Study GuideDokument17 SeitenLinear Regression - Six Sigma Study GuideSunilNoch keine Bewertungen

- Unit-Iii Correlation and Regression AnalysisDokument17 SeitenUnit-Iii Correlation and Regression AnalysisSiddiqullah IhsasNoch keine Bewertungen

- Chapter 14 (14.1 - 14.2)Dokument22 SeitenChapter 14 (14.1 - 14.2)JaydeNoch keine Bewertungen

- Evans Analytics2e PPT 08Dokument65 SeitenEvans Analytics2e PPT 08txuanNoch keine Bewertungen

- CH 4. BAsic Estimation TechniqueDokument27 SeitenCH 4. BAsic Estimation TechniquedanarNoch keine Bewertungen

- CorrelationDokument18 SeitenCorrelationanandNoch keine Bewertungen

- Regression: Leech N L, Barret K C & Morgan G A (2011)Dokument35 SeitenRegression: Leech N L, Barret K C & Morgan G A (2011)Sam AbdulNoch keine Bewertungen

- RegressionDokument25 SeitenRegressionABY MOTTY RMCAA20-23Noch keine Bewertungen

- L15-Correlation and RegressionDokument19 SeitenL15-Correlation and RegressionRamesh G100% (1)

- Review: I Am Examining Differences in The Mean Between GroupsDokument44 SeitenReview: I Am Examining Differences in The Mean Between GroupsAtlas Cerbo100% (1)

- Correlation & Regression AnalysisDokument39 SeitenCorrelation & Regression AnalysisAbhipreeth Mehra100% (1)

- Chpter 4 emDokument27 SeitenChpter 4 emMuhammad Hanief Al-KautsarNoch keine Bewertungen

- Bda 1Dokument28 SeitenBda 1Ikhsan WijayaNoch keine Bewertungen

- Unit 9 Simple Linear Regression: StructureDokument22 SeitenUnit 9 Simple Linear Regression: Structuresita rautelaNoch keine Bewertungen

- Simple Correlation and Regression AnalysisDokument14 SeitenSimple Correlation and Regression AnalysisBibhush MaharjanNoch keine Bewertungen

- Linear Regression and Correlation: Mcgraw-Hill/IrwinDokument10 SeitenLinear Regression and Correlation: Mcgraw-Hill/IrwinTâÿÿàbá ĮkrâmNoch keine Bewertungen

- Probability and Statistics: Simple Linear RegressionDokument37 SeitenProbability and Statistics: Simple Linear RegressionNguyễn Linh ChiNoch keine Bewertungen

- Chapter 4-Correlation and RegresssionDokument60 SeitenChapter 4-Correlation and RegresssionWario KampeNoch keine Bewertungen

- Week 6Dokument58 SeitenWeek 6ABDULLAH AAMIR100% (1)

- BRM - 4.4 Measures of Linear RelationshipDokument3 SeitenBRM - 4.4 Measures of Linear RelationshipSasin SasikalaNoch keine Bewertungen

- Linear RegressionDokument17 SeitenLinear RegressionLuka SavićNoch keine Bewertungen

- Dersnot 2400 1621509895Dokument37 SeitenDersnot 2400 1621509895aliNoch keine Bewertungen

- DADM-Correlation and RegressionDokument138 SeitenDADM-Correlation and RegressionDipesh KarkiNoch keine Bewertungen

- Unit-III (Data Analytics)Dokument15 SeitenUnit-III (Data Analytics)bhavya.shivani1473Noch keine Bewertungen

- Simple Linear Regression and Correlation (Continue..,)Dokument30 SeitenSimple Linear Regression and Correlation (Continue..,)Lan Anh BuiNoch keine Bewertungen

- Correlation and RegressionDokument71 SeitenCorrelation and RegressionPradeepNoch keine Bewertungen

- CH 8Dokument21 SeitenCH 8ጌታ እኮ ነውNoch keine Bewertungen

- Regression-SIMPLE LINEARDokument24 SeitenRegression-SIMPLE LINEARNitin chopdaNoch keine Bewertungen

- Final Exam ACF F2019Dokument3 SeitenFinal Exam ACF F2019Carey CaiNoch keine Bewertungen

- P0. Introduction and SummaryDokument43 SeitenP0. Introduction and SummaryCarey CaiNoch keine Bewertungen

- Economy of Strategic PlannningDokument10 SeitenEconomy of Strategic PlannningCarey CaiNoch keine Bewertungen

- 04 Rental Car Giant Successful 2 PDFDokument3 Seiten04 Rental Car Giant Successful 2 PDFCarey CaiNoch keine Bewertungen

- Land Secruities GroupDokument1 SeiteLand Secruities GroupCarey CaiNoch keine Bewertungen

- Apple 2015 Vision Strategy - 160402 - 8-7-2015 - CL - 13e0 - 0Dokument24 SeitenApple 2015 Vision Strategy - 160402 - 8-7-2015 - CL - 13e0 - 0Carey Cai100% (1)

- Practicewith Argument Athletesas ActivistsDokument30 SeitenPracticewith Argument Athletesas ActivistsRob BrantNoch keine Bewertungen

- Visual Metaphor Process BookDokument18 SeitenVisual Metaphor Process Bookmatt8859Noch keine Bewertungen

- Electronic Parts Catalog - Option Detail Option Group Graphic Film Card DateDokument2 SeitenElectronic Parts Catalog - Option Detail Option Group Graphic Film Card DatenurdinzaiNoch keine Bewertungen

- PCM 2.4l Turbo 5 de 5Dokument2 SeitenPCM 2.4l Turbo 5 de 5Felix VelasquezNoch keine Bewertungen

- Code of Federal RegulationsDokument14 SeitenCode of Federal RegulationsdiwolfieNoch keine Bewertungen

- Optimizing Stata For Analysis of Large Data SetsDokument29 SeitenOptimizing Stata For Analysis of Large Data SetsTrần Anh TùngNoch keine Bewertungen

- Fanii 2Dokument55 SeitenFanii 2Remixer INDONESIANoch keine Bewertungen

- ERP Solution in Hospital: Yangyang Shao TTU 2013Dokument25 SeitenERP Solution in Hospital: Yangyang Shao TTU 2013Vishakh SubbayyanNoch keine Bewertungen

- Kowalkowskietal 2023 Digital Service Innovationin B2 BDokument48 SeitenKowalkowskietal 2023 Digital Service Innovationin B2 BAdolf DasslerNoch keine Bewertungen

- Class Routine Final 13.12.18Dokument7 SeitenClass Routine Final 13.12.18RakibNoch keine Bewertungen

- International Supply Chain ManagementDokument2 SeitenInternational Supply Chain ManagementPRASANT KUMAR SAMALNoch keine Bewertungen

- Unit 3Dokument5 SeitenUnit 3Narasimman DonNoch keine Bewertungen

- 19 Uco 578Dokument20 Seiten19 Uco 578roshan jainNoch keine Bewertungen

- Swot Matrix Strengths WeaknessesDokument6 SeitenSwot Matrix Strengths Weaknessestaehyung trash100% (1)

- 19 71 Hydrologic Engineering Methods For Water Resources DevelopmentDokument654 Seiten19 71 Hydrologic Engineering Methods For Water Resources DevelopmentMartha LetchingerNoch keine Bewertungen

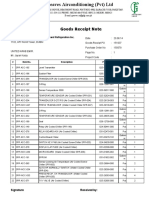

- Goods Receipt Note: Johnson Controls Air Conditioning and Refrigeration Inc. (YORK) DateDokument4 SeitenGoods Receipt Note: Johnson Controls Air Conditioning and Refrigeration Inc. (YORK) DateSaad PathanNoch keine Bewertungen

- Angle ModulationDokument26 SeitenAngle ModulationAtish RanjanNoch keine Bewertungen

- 61annual Report 2010-11 EngDokument237 Seiten61annual Report 2010-11 Engsoap_bendNoch keine Bewertungen

- Manish Kumar: Desire To Work and Grow in The Field of MechanicalDokument4 SeitenManish Kumar: Desire To Work and Grow in The Field of MechanicalMANISHNoch keine Bewertungen

- Naca Duct RMDokument47 SeitenNaca Duct RMGaurav GuptaNoch keine Bewertungen

- Why We Need A Flying Amphibious Car 1. CarsDokument20 SeitenWhy We Need A Flying Amphibious Car 1. CarsAsim AhmedNoch keine Bewertungen

- A First Etymological Dictionary of BasquDokument29 SeitenA First Etymological Dictionary of BasquDaily MailNoch keine Bewertungen