Das könnte Ihnen auch gefallen

- Wartsila Me Operations ManualDokument373 SeitenWartsila Me Operations ManualsridharsharmaNoch keine Bewertungen

- Case Study 2 - Planning An Audit of FSDokument7 SeitenCase Study 2 - Planning An Audit of FSKristine Lirose Bordeos100% (3)

- India Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBREDokument20 SeitenIndia Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBRErealtywatch108Noch keine Bewertungen

- Rational MethodDokument158 SeitenRational MethodMilos Petrovic100% (2)

- QGL-CE-001Guidelines For Corridors and Corridor CrossingsRev2Dokument29 SeitenQGL-CE-001Guidelines For Corridors and Corridor CrossingsRev2tomNoch keine Bewertungen

- Hollow Blocks MakingDokument41 SeitenHollow Blocks Makingeleonor100% (1)

- Project Proposal: Project Proposal Level III Waterworks Project LGU Gamu, Isabela C.Y. 2017Dokument3 SeitenProject Proposal: Project Proposal Level III Waterworks Project LGU Gamu, Isabela C.Y. 2017Marieta Alejo83% (6)

- Plumbing Key AnswerDokument7 SeitenPlumbing Key AnswerStanley Scott ArroyoNoch keine Bewertungen

- Ecological ModelingDokument421 SeitenEcological ModelingMiguel HLNoch keine Bewertungen

- Chief Officer On Job Training: Cargo Plan, SequenceDokument48 SeitenChief Officer On Job Training: Cargo Plan, SequenceNyan Min Htet100% (1)

- 2021 Thailand Market Outlook Report enDokument23 Seiten2021 Thailand Market Outlook Report enGalih AnggoroNoch keine Bewertungen

- Purification of Water: On Large ScaleDokument71 SeitenPurification of Water: On Large ScaleHarshal Sabane100% (5)

- Horizon Real EstateDokument72 SeitenHorizon Real EstateShobhit GoswamiNoch keine Bewertungen

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaVon EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaNoch keine Bewertungen

- Effect of External Public Debt On The Exchange Rate in KenyaDokument22 SeitenEffect of External Public Debt On The Exchange Rate in KenyaIJEBR100% (1)

- Introduction To The Study of GlobalizationDokument83 SeitenIntroduction To The Study of GlobalizationIt zyNoch keine Bewertungen

- The Build Build Build Program To The Philippines EconomyDokument5 SeitenThe Build Build Build Program To The Philippines EconomyLEVY ALVAREZNoch keine Bewertungen

- Vision 2025 EnglishDokument56 SeitenVision 2025 EnglishAhmed IqbalNoch keine Bewertungen

- Overview Facility Management Financing in The Construction Industry in Accra, GhanaDokument5 SeitenOverview Facility Management Financing in The Construction Industry in Accra, GhanaAlexander DeckerNoch keine Bewertungen

- High GDP Growth: Growth of Services SectorDokument5 SeitenHigh GDP Growth: Growth of Services SectorAbhishek MahnotNoch keine Bewertungen

- Risks in Financing Real Estate Projects - Rating Agency PerspectivesDokument8 SeitenRisks in Financing Real Estate Projects - Rating Agency Perspectivesirfan alamNoch keine Bewertungen

- Economics 2 - Cia 4Dokument10 SeitenEconomics 2 - Cia 4PranavNoch keine Bewertungen

- Mae ReportDokument7 SeitenMae ReportAreesha KamranNoch keine Bewertungen

- Political EconomicalDokument15 SeitenPolitical EconomicalRaymond PascualNoch keine Bewertungen

- 10 - QH (Sep Dec 2022) - Answer by Sir Hasan Dossani (Full Drafting)Dokument16 Seiten10 - QH (Sep Dec 2022) - Answer by Sir Hasan Dossani (Full Drafting)abdullahdap9691Noch keine Bewertungen

- Impact of COVID-19 On The Economy:: Recovery of Aggregate Demand Hinges On Private InvestmentDokument9 SeitenImpact of COVID-19 On The Economy:: Recovery of Aggregate Demand Hinges On Private InvestmentTavish SettNoch keine Bewertungen

- Penta OceanDokument4 SeitenPenta OceanLee YengNoch keine Bewertungen

- Government Support To Private Infrastructure: M ArketsDokument35 SeitenGovernment Support To Private Infrastructure: M ArketsspratiwiaNoch keine Bewertungen

- DLF LTD..PPTX (Autosaved)Dokument18 SeitenDLF LTD..PPTX (Autosaved)kevinNoch keine Bewertungen

- Mid SemDokument11 SeitenMid SemUdeshi ShermilaNoch keine Bewertungen

- Economic Analysis of Indian Construction IndustryDokument23 SeitenEconomic Analysis of Indian Construction IndustryDIVYANSHU SHEKHARNoch keine Bewertungen

- Covid 19onEthiopianConstructionIndustryDokument7 SeitenCovid 19onEthiopianConstructionIndustryThomas MehariNoch keine Bewertungen

- Research On Infrastructure FundDokument33 SeitenResearch On Infrastructure FundSimaNoch keine Bewertungen

- RLB International Report First Quarter 2012Dokument36 SeitenRLB International Report First Quarter 2012Chris GonzalesNoch keine Bewertungen

- India's GDP Growth - Challenges and OpportunitiesDokument8 SeitenIndia's GDP Growth - Challenges and OpportunitiesAnjali SinghNoch keine Bewertungen

- August 2019Dokument2 SeitenAugust 2019Kiran MNoch keine Bewertungen

- Construction Situation Analysis Write UpDokument10 SeitenConstruction Situation Analysis Write UpEliza Mae de GuzmanNoch keine Bewertungen

- Industry Profile and Analysis - ConstructionDokument17 SeitenIndustry Profile and Analysis - Constructionmarcred24Noch keine Bewertungen

- Foreign Direct Investment Cohesion To EmploymentDokument25 SeitenForeign Direct Investment Cohesion To EmploymentChandan SrivastavaNoch keine Bewertungen

- Fundamental Analysis Economy Analysis: TaxationDokument54 SeitenFundamental Analysis Economy Analysis: Taxationvivek0020100% (1)

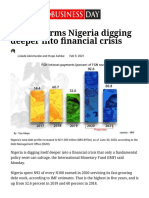

- IMF Confirms Nigeria Digging Deeper Into Financial Crisis - Businessday NGDokument4 SeitenIMF Confirms Nigeria Digging Deeper Into Financial Crisis - Businessday NGAnneNoch keine Bewertungen

- Economic Slowdown Causes, Remedied and SugesstionDokument14 SeitenEconomic Slowdown Causes, Remedied and Sugesstionsagar beheraNoch keine Bewertungen

- The Dynamic Situation of Foot Loose Industry in Indonesia Artha Yudilla, S.I.P, M.ADokument6 SeitenThe Dynamic Situation of Foot Loose Industry in Indonesia Artha Yudilla, S.I.P, M.AwhyyoumakeitsohardNoch keine Bewertungen

- Research Paper On GDP of IndiaDokument6 SeitenResearch Paper On GDP of Indiauifjzvrif100% (1)

- CommentDokument2 SeitenCommentshanikayani_20103758Noch keine Bewertungen

- Economic Reforms in India New Regimen of LPG: Presented by Anil Bishnoi Amit Joshi Amrish Pal Anand KishoreDokument32 SeitenEconomic Reforms in India New Regimen of LPG: Presented by Anil Bishnoi Amit Joshi Amrish Pal Anand KishoreantiamitNoch keine Bewertungen

- Report of Economic CommitteeDokument13 SeitenReport of Economic CommitteekathyskwoNoch keine Bewertungen

- Reversing India's Downward Trajectory-Jan 2012Dokument3 SeitenReversing India's Downward Trajectory-Jan 2012SP1Noch keine Bewertungen

- 20030220-21 Vijayakumari Kanapathy Services SectorDokument23 Seiten20030220-21 Vijayakumari Kanapathy Services Sectorngan ping pingNoch keine Bewertungen

- Strama 1 Reporting SampleDokument19 SeitenStrama 1 Reporting SampleMark Roger II HuberitNoch keine Bewertungen

- Singapore Construction Market Review and OUTLOOK 2021Dokument18 SeitenSingapore Construction Market Review and OUTLOOK 2021Conifer YuNoch keine Bewertungen

- GS-3 Answer WritingDokument35 SeitenGS-3 Answer WritingPranav VatsNoch keine Bewertungen

- Malaysian Government's Debt To Approach RM1Dokument2 SeitenMalaysian Government's Debt To Approach RM1reachmyaNoch keine Bewertungen

- Impact of Private Sectors in Philippine Urban PlanningDokument4 SeitenImpact of Private Sectors in Philippine Urban PlanningAnon123Noch keine Bewertungen

- Unitech Limited Annual Report 2014 15Dokument192 SeitenUnitech Limited Annual Report 2014 15sriramrangaNoch keine Bewertungen

- Impact of Covid 19: Shreyash Punnamwar Sarthak Rawat Amit Kumar DashDokument10 SeitenImpact of Covid 19: Shreyash Punnamwar Sarthak Rawat Amit Kumar DashKhushram YadavNoch keine Bewertungen

- Foreign Direct Investment Bharth Cohesion To EmploymentDokument24 SeitenForeign Direct Investment Bharth Cohesion To EmploymentBharath GudiNoch keine Bewertungen

- Principle of Economics Theory Group AssigmentDokument16 SeitenPrinciple of Economics Theory Group AssigmentCrystalPingNoch keine Bewertungen

- FSABV Final ReportDokument3 SeitenFSABV Final ReportSrikanth Kumar KonduriNoch keine Bewertungen

- Debt & Econmy of PaistanDokument15 SeitenDebt & Econmy of PaistanSajjad Ahmed ShaikhNoch keine Bewertungen

- Global Location TrendsDokument26 SeitenGlobal Location TrendsigorNoch keine Bewertungen

- Owoyemi Olaide PSR 305 AssignmentDokument5 SeitenOwoyemi Olaide PSR 305 AssignmentomobayodenelsonNoch keine Bewertungen

- September Dossier 2Dokument8 SeitenSeptember Dossier 2...Noch keine Bewertungen

- Case Study 2 - First DraftDokument4 SeitenCase Study 2 - First DraftCyra EllaineNoch keine Bewertungen

- CII BWR ReportDokument27 SeitenCII BWR ReportBalakrishna DammatiNoch keine Bewertungen

- Private Sector Operations in 2019: Report on Development EffectivenessVon EverandPrivate Sector Operations in 2019: Report on Development EffectivenessNoch keine Bewertungen

- Overcoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyVon EverandOvercoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyNoch keine Bewertungen

- Policy Forum On ISWM Proceedings - FINALDokument103 SeitenPolicy Forum On ISWM Proceedings - FINALRegg Dela CruzNoch keine Bewertungen

- Study of Parameters Affecting Dry and Wet Ozone Bleaching of Denim FabricDokument8 SeitenStudy of Parameters Affecting Dry and Wet Ozone Bleaching of Denim FabricMd.HussainNoch keine Bewertungen

- Peigao Duan, Xiujun Bai, Yuping Xu, Aiyun Zhang, Feng Wang, Lei Zhang, Juan MiaoDokument9 SeitenPeigao Duan, Xiujun Bai, Yuping Xu, Aiyun Zhang, Feng Wang, Lei Zhang, Juan MiaoyemresimsekNoch keine Bewertungen

- Abílio Et Al., 2005Dokument10 SeitenAbílio Et Al., 2005Wenner BritoNoch keine Bewertungen

- Módulo 8 de InglêsDokument8 SeitenMódulo 8 de InglêsFilipe SantosNoch keine Bewertungen

- IWA City Stories SingaporeDokument2 SeitenIWA City Stories SingaporeThang LongNoch keine Bewertungen

- Polyisobutylene SuccinicamideDokument9 SeitenPolyisobutylene Succinicamideperqs BeautyisjoyNoch keine Bewertungen

- Study of Cooling System With Water Mist Sprayers FDokument10 SeitenStudy of Cooling System With Water Mist Sprayers FAbdelrhman MahfouzNoch keine Bewertungen

- Recent Ceramic Analysis: Origins 1. Function, Style, andDokument31 SeitenRecent Ceramic Analysis: Origins 1. Function, Style, andTony SneijderNoch keine Bewertungen

- Water Filters Ionicore CatalogDokument9 SeitenWater Filters Ionicore CatalogSinergroup Water Filters Water Purifiers Water SoftenersNoch keine Bewertungen

- A New Scheme For Ammonia and Fertilizer GenerationDokument14 SeitenA New Scheme For Ammonia and Fertilizer GenerationChiaoNoch keine Bewertungen

- In-Class Thermochemistry Practice Problems Name - Ella Bomberger - Date - Block - BDokument3 SeitenIn-Class Thermochemistry Practice Problems Name - Ella Bomberger - Date - Block - BElla BombergerNoch keine Bewertungen

- Technical Specification RECDokument742 SeitenTechnical Specification RECHooghly IPDSNoch keine Bewertungen

- Alternative Deconstruct and Design TaskDokument5 SeitenAlternative Deconstruct and Design Taskapi-321385393Noch keine Bewertungen

- Coming Out of The Ice Age - BASF Durasorb Cryo-HRUDokument11 SeitenComing Out of The Ice Age - BASF Durasorb Cryo-HRULiu YangtzeNoch keine Bewertungen

- Introduction To Water TreatmentDokument132 SeitenIntroduction To Water TreatmentViorel HarceagNoch keine Bewertungen

- 4 A's DLP SampleDokument5 Seiten4 A's DLP SampleJake AlojadoNoch keine Bewertungen

- Physics PressureDokument35 SeitenPhysics Pressuresai yadaNoch keine Bewertungen

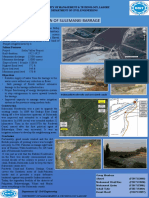

- Design of Sulemanki Barrage: University of Management & Technology, Lahore Department of Civil EngineeringDokument1 SeiteDesign of Sulemanki Barrage: University of Management & Technology, Lahore Department of Civil EngineeringWasif RiazNoch keine Bewertungen

- Civil Engineering and Environmental ScienceDokument2 SeitenCivil Engineering and Environmental ScienceNyel SaduesteNoch keine Bewertungen

- Rainwater Harvesting 101 - Your How-To Collect Rainwater GuideDokument13 SeitenRainwater Harvesting 101 - Your How-To Collect Rainwater GuideNitheesh KumarNoch keine Bewertungen

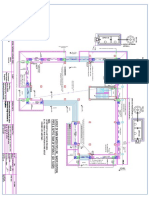

- Option-05 - Ground Floor Plan-Detailed DrawingsDokument1 SeiteOption-05 - Ground Floor Plan-Detailed DrawingsCEG BangladeshNoch keine Bewertungen