Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- CB2 Booklet 1Dokument114 SeitenCB2 Booklet 1Somya AgrawalNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- E PassbookDokument5 SeitenE PassbookJASVINDER SINGHNoch keine Bewertungen

- Unit 4Dokument100 SeitenUnit 4Somya AgrawalNoch keine Bewertungen

- William Stallings Computer Organization and Architecture 10 EditionDokument38 SeitenWilliam Stallings Computer Organization and Architecture 10 EditionSomya AgrawalNoch keine Bewertungen

- William Stallings Computer Organization and Architecture 10 EditionDokument52 SeitenWilliam Stallings Computer Organization and Architecture 10 EditionSomya AgrawalNoch keine Bewertungen

- William Stallings Computer Organization and Architecture 10 EditionDokument47 SeitenWilliam Stallings Computer Organization and Architecture 10 EditionAbood AbujamousNoch keine Bewertungen

- William Stallings Computer Organization and Architecture 10 EditionDokument43 SeitenWilliam Stallings Computer Organization and Architecture 10 EditionSomya AgrawalNoch keine Bewertungen

- William Stallings Computer Organization and Architecture 10 EditionDokument19 SeitenWilliam Stallings Computer Organization and Architecture 10 EditionSomya AgrawalNoch keine Bewertungen

- CH04-COA10e Cache MemoryDokument46 SeitenCH04-COA10e Cache MemoryGet InsightNoch keine Bewertungen

- William Stallings Computer Organization and Architecture 10 EditionDokument33 SeitenWilliam Stallings Computer Organization and Architecture 10 EditionkrtxbNoch keine Bewertungen

- CB2 Booklet 2Dokument150 SeitenCB2 Booklet 2Somya AgrawalNoch keine Bewertungen

- CB2 Booklet 3Dokument102 SeitenCB2 Booklet 3Somya AgrawalNoch keine Bewertungen

- Subject CT7 - Economics: Institute of Actuaries of IndiaDokument7 SeitenSubject CT7 - Economics: Institute of Actuaries of IndiaSomya AgrawalNoch keine Bewertungen

- Actuarial Society of India: ExaminationsDokument7 SeitenActuarial Society of India: ExaminationsSomya AgrawalNoch keine Bewertungen

- Actuarial Society of India: ExaminationsDokument4 SeitenActuarial Society of India: ExaminationsSomya AgrawalNoch keine Bewertungen

- Algebra Cheat Sheet: Basic Properties & FactsDokument4 SeitenAlgebra Cheat Sheet: Basic Properties & FactsAnonymous wTQriXbYt9Noch keine Bewertungen

- Question Paper of The DAVV CET ExamDokument32 SeitenQuestion Paper of The DAVV CET ExamMunna RajNoch keine Bewertungen

- IDIOMS and PhrasesDokument67 SeitenIDIOMS and PhraseskavinkumareceNoch keine Bewertungen

- Electricals and ElectronicsDokument14 SeitenElectricals and ElectronicsSomya AgrawalNoch keine Bewertungen

- Common English IdiomsDokument13 SeitenCommon English IdiomsLucia PopaNoch keine Bewertungen

- Algebra Cheat Sheet: Basic Properties & FactsDokument4 SeitenAlgebra Cheat Sheet: Basic Properties & FactsAnonymous wTQriXbYt9Noch keine Bewertungen

- Science ProjectDokument24 SeitenScience ProjectSomya AgrawalNoch keine Bewertungen

- 4073xxxxxxxx4016 32545 Retail MMT NormDokument4 Seiten4073xxxxxxxx4016 32545 Retail MMT NormAishwarya MandhalkarNoch keine Bewertungen

- Financial Management Review: By: Lolita ApatanDokument11 SeitenFinancial Management Review: By: Lolita Apatanlovella lastrellaNoch keine Bewertungen

- Comparative Analysis of Home Loans Across Different Banks inDokument55 SeitenComparative Analysis of Home Loans Across Different Banks inShikha Wadwa0% (1)

- Urban Dictionary - AsdfghjkDokument3 SeitenUrban Dictionary - AsdfghjkPRASHANTH B SNoch keine Bewertungen

- Form 4 English Paper1 Ujian Pengesanan Sept2021Dokument16 SeitenForm 4 English Paper1 Ujian Pengesanan Sept2021NAJWA ZAHIDAH BINTI RAZALI MoeNoch keine Bewertungen

- Chapter08 TestbankDokument38 SeitenChapter08 Testbankphuoc.tran23006297Noch keine Bewertungen

- Peer Educators AllowanceDokument4 SeitenPeer Educators AllowanceKealeboga Duece ThoboloNoch keine Bewertungen

- ComputerDokument4 SeitenComputersanthoshjee73Noch keine Bewertungen

- How Interest Rates Work On Car LoansDokument3 SeitenHow Interest Rates Work On Car LoansKurt Del RosarioNoch keine Bewertungen

- BankingDokument29 SeitenBankingAnnyesha ChatterjeeNoch keine Bewertungen

- The 12 Investment Club - ICEA UGANDA MONEY MARKET FUNDDokument2 SeitenThe 12 Investment Club - ICEA UGANDA MONEY MARKET FUNDChrispus MutabuuzaNoch keine Bewertungen

- Money and Banking NotesDokument9 SeitenMoney and Banking NotesLuisLoNoch keine Bewertungen

- Idbi Loan Project For FinanceDokument46 SeitenIdbi Loan Project For Financefardeenansari 646Noch keine Bewertungen

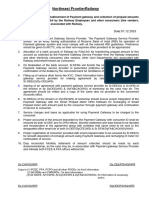

- Final JPO-Payment Gateway Integration For Smart Prepaid Meter RechargeDokument1 SeiteFinal JPO-Payment Gateway Integration For Smart Prepaid Meter RechargesitharamNoch keine Bewertungen

- Project On Punjab National BankDokument86 SeitenProject On Punjab National BankRohit ChauhanNoch keine Bewertungen

- Banking and Economics MCqs PDFDokument103 SeitenBanking and Economics MCqs PDFqazi k100% (1)

- All SAP Transaction Codes With Report and Description From F To HDokument50 SeitenAll SAP Transaction Codes With Report and Description From F To HAntonio RomeroNoch keine Bewertungen

- Questionnaire For BankDokument3 SeitenQuestionnaire For BankRahat SarwatNoch keine Bewertungen

- MBBsavings - 158118 107625 - 2016 12 31Dokument7 SeitenMBBsavings - 158118 107625 - 2016 12 31Zahar ZekNoch keine Bewertungen

- Foreign Exchange Exposure and Risk Management: Learning OutcomesDokument52 SeitenForeign Exchange Exposure and Risk Management: Learning Outcomesqamaraleem1_25038318Noch keine Bewertungen

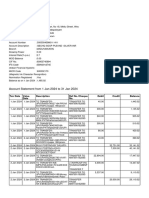

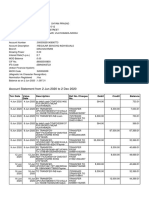

- Account Statement From 2 Jun 2020 To 2 Dec 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument11 SeitenAccount Statement From 2 Jun 2020 To 2 Dec 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceanitha anuNoch keine Bewertungen

- Sop 8Dokument4 SeitenSop 8MadhuriNikamNoch keine Bewertungen

- Payment InstructionsDokument3 SeitenPayment InstructionsNour shawaNoch keine Bewertungen

- Print ChallanDokument1 SeitePrint ChallanSameer AsifNoch keine Bewertungen

- What Is Money: - Money Give You FreedomDokument2 SeitenWhat Is Money: - Money Give You FreedomNguyễn Thành VinhNoch keine Bewertungen

- Service Marketing Mix or 7p'sDokument5 SeitenService Marketing Mix or 7p'srasel_ustcNoch keine Bewertungen

- Treasury BillsDokument11 SeitenTreasury BillsnavneetNoch keine Bewertungen

- Marshet Sisay Final Research PaperDokument81 SeitenMarshet Sisay Final Research Paperdagnaye100% (1)

- Banking ReportDokument36 SeitenBanking Reportabhishek pathakNoch keine Bewertungen