Das könnte Ihnen auch gefallen

- (EMERSON) Loop CheckingDokument29 Seiten(EMERSON) Loop CheckingDavid Chagas80% (5)

- 272 Concept Class Mansoura University DR Rev 2Dokument8 Seiten272 Concept Class Mansoura University DR Rev 2Gazzara WorldNoch keine Bewertungen

- CH - 9 Assessing The Risk of Material MisstatementDokument14 SeitenCH - 9 Assessing The Risk of Material MisstatementOmar C100% (1)

- DAP FullTextIntroductionByStuartLichtman PDFDokument21 SeitenDAP FullTextIntroductionByStuartLichtman PDFAlejandro CordobaNoch keine Bewertungen

- Audit Planning ProcessDokument7 SeitenAudit Planning ProcessJun Guerzon PaneloNoch keine Bewertungen

- Formal 17 12 04 PDFDokument184 SeitenFormal 17 12 04 PDFJose LaraNoch keine Bewertungen

- ACCA Paper F 8 AUDIT AND ASSURANCE SERVICES (INTERNATIONAL STREAM) Lecture 3 Audit Planning and Risk AssessmentDokument20 SeitenACCA Paper F 8 AUDIT AND ASSURANCE SERVICES (INTERNATIONAL STREAM) Lecture 3 Audit Planning and Risk AssessmentFahmi AbdullaNoch keine Bewertungen

- Amended ComplaintDokument38 SeitenAmended ComplaintDeadspinNoch keine Bewertungen

- Practical AuditingDokument61 SeitenPractical Auditinglloyd100% (1)

- Assurance Revision Notes Chapter OverviewDokument15 SeitenAssurance Revision Notes Chapter OverviewampriestNoch keine Bewertungen

- GE 03 - Fundamentals of Business Mathematics Time Series Analysis & ForecastingDokument8 SeitenGE 03 - Fundamentals of Business Mathematics Time Series Analysis & ForecastingAzizul AviNoch keine Bewertungen

- Arens Auditing16e SM 09Dokument28 SeitenArens Auditing16e SM 09김현중Noch keine Bewertungen

- Arens Auditing16e SM 12Dokument40 SeitenArens Auditing16e SM 12김현중Noch keine Bewertungen

- Assessment of Audit RiskDokument9 SeitenAssessment of Audit RiskAli KhanNoch keine Bewertungen

- The Risk-Based Audit ModelDokument2 SeitenThe Risk-Based Audit ModelJoshel MaeNoch keine Bewertungen

- Audit 1report On Audit Planning of Beximco Pharmaceuticals Ltd.Dokument29 SeitenAudit 1report On Audit Planning of Beximco Pharmaceuticals Ltd.nidal_adnanNoch keine Bewertungen

- Sap Fi/Co: Transaction CodesDokument51 SeitenSap Fi/Co: Transaction CodesReddaveni NagarajuNoch keine Bewertungen

- Comptronix Case FinalDokument9 SeitenComptronix Case FinalMarina KushilovskayaNoch keine Bewertungen

- Library Management System (Final)Dokument88 SeitenLibrary Management System (Final)Ariunbat Togtohjargal90% (30)

- Answer-Internal ControlDokument5 SeitenAnswer-Internal ControlKathlene BalicoNoch keine Bewertungen

- Audit Approach PDFDokument12 SeitenAudit Approach PDFfaisal gaziNoch keine Bewertungen

- Test of Control And/or Substantive Procedure, Developed To Assess The Efficacy of Controls inDokument4 SeitenTest of Control And/or Substantive Procedure, Developed To Assess The Efficacy of Controls inIsabell CastroNoch keine Bewertungen

- Week 1 and 2 QuestionsDokument3 SeitenWeek 1 and 2 QuestionsANGELI GRACE GALVANNoch keine Bewertungen

- Audit Risk FactorsDokument6 SeitenAudit Risk Factorsakii ramNoch keine Bewertungen

- AudTheo Compilation Chap9 14Dokument130 SeitenAudTheo Compilation Chap9 14Chris tine Mae MendozaNoch keine Bewertungen

- Auditing Book EditedDokument72 SeitenAuditing Book EditedJE SingianNoch keine Bewertungen

- AuditDokument6 SeitenAuditMOHAMED SLIMANINoch keine Bewertungen

- Expected Learning Outcomes: After Studying This Chapter, You Should Be Able ToDokument21 SeitenExpected Learning Outcomes: After Studying This Chapter, You Should Be Able ToMisshtaCNoch keine Bewertungen

- Chapter 8 AuditDokument22 SeitenChapter 8 AuditMisshtaCNoch keine Bewertungen

- Activity 6Dokument4 SeitenActivity 6Isabell CastroNoch keine Bewertungen

- Audit RisksDokument4 SeitenAudit RisksAliAwaisNoch keine Bewertungen

- Audit 2 SlidesDokument127 SeitenAudit 2 SlidesZAID ALKALHANoch keine Bewertungen

- Auditing fraud risksDokument3 SeitenAuditing fraud risksPhilip Jhon BayoNoch keine Bewertungen

- Knowledge Based QuestionsDokument17 SeitenKnowledge Based Questions5mh8cyfgt4Noch keine Bewertungen

- Audit Planning: 1. The Background of The EntityDokument16 SeitenAudit Planning: 1. The Background of The EntityHussain MustunNoch keine Bewertungen

- Audit Documentation GuideDokument12 SeitenAudit Documentation Guideagnymahajan100% (1)

- Mod 1Dokument15 SeitenMod 1Marie claire Delos santosNoch keine Bewertungen

- Chapter 3Dokument14 SeitenChapter 3Donald HollistNoch keine Bewertungen

- I. Definitions, Standards and PlanningDokument4 SeitenI. Definitions, Standards and PlanninglauraoldkwNoch keine Bewertungen

- Uploaded in Moodle As A Guide To Complete Your Assignment Apart From Your Other Sources.)Dokument6 SeitenUploaded in Moodle As A Guide To Complete Your Assignment Apart From Your Other Sources.)Derek GawiNoch keine Bewertungen

- Auditing - Chapter 3Dokument54 SeitenAuditing - Chapter 3Tesfaye SimeNoch keine Bewertungen

- 1 Discuss The Purposes of (1) Substantive Tests of Transactions, (2) Tests of Controls, and (3) Tests of Details of Balances. Give An Example of EachDokument3 Seiten1 Discuss The Purposes of (1) Substantive Tests of Transactions, (2) Tests of Controls, and (3) Tests of Details of Balances. Give An Example of EachSún HítNoch keine Bewertungen

- Auditing 1 Final Chapter 10Dokument7 SeitenAuditing 1 Final Chapter 10PaupauNoch keine Bewertungen

- Effective Internal Control - R: Procedures To Be Performed Are Matters For The Professional Judgment of The AuditorDokument5 SeitenEffective Internal Control - R: Procedures To Be Performed Are Matters For The Professional Judgment of The Auditorlorie anne valleNoch keine Bewertungen

- Tugas Audit Chpter9 Risk PrintDokument11 SeitenTugas Audit Chpter9 Risk PrintKazuyano DoniNoch keine Bewertungen

- Chapter 8,9 AT 1Dokument3 SeitenChapter 8,9 AT 1De Nev OelNoch keine Bewertungen

- Consideration of Internal ControlDokument4 SeitenConsideration of Internal ControlFritzie Ann ZartigaNoch keine Bewertungen

- CH 9 Assessing The Risk of Material MisstatementDokument7 SeitenCH 9 Assessing The Risk of Material MisstatementNada An-NaurahNoch keine Bewertungen

- Chapter 1-3 SummaryDokument10 SeitenChapter 1-3 SummaryLovely Jane Raut CabiltoNoch keine Bewertungen

- Audit Risk & Internal ControlsDokument51 SeitenAudit Risk & Internal ControlsRalfNoch keine Bewertungen

- Aud Theo - 3Dokument5 SeitenAud Theo - 3Cyra EllaineNoch keine Bewertungen

- Difficulties, If There Are Concerns With Compliance, It Implies There Are ProblemsDokument4 SeitenDifficulties, If There Are Concerns With Compliance, It Implies There Are ProblemsBrian GoNoch keine Bewertungen

- Accounting 1Dokument44 SeitenAccounting 1Kristan John ZernaNoch keine Bewertungen

- F8 ACCA Summary + Revision Notes 2017Dokument148 SeitenF8 ACCA Summary + Revision Notes 2017Arbab JhangirNoch keine Bewertungen

- AT Quiz 1 - B1Dokument15 SeitenAT Quiz 1 - B1AMNoch keine Bewertungen

- What Are The Three Types of Audit Risk.Dokument3 SeitenWhat Are The Three Types of Audit Risk.Yasir RafiqNoch keine Bewertungen

- 5 PlanningDokument20 Seiten5 PlanningSayraj Siddiki AnikNoch keine Bewertungen

- At IntroDokument13 SeitenAt IntrocmpaguntalanNoch keine Bewertungen

- Auditing One 03 OKDokument28 SeitenAuditing One 03 OKRObel demisNoch keine Bewertungen

- Essay On AuditingDokument7 SeitenEssay On AuditingAndy Rdz0% (1)

- Acc12 - PrelimsDokument5 SeitenAcc12 - PrelimsLuise MauieNoch keine Bewertungen

- Principles of Auditing - Chapter - 5Dokument35 SeitenPrinciples of Auditing - Chapter - 5Wijdan Saleem EdwanNoch keine Bewertungen

- Audit Practice and Assurance Services - A1.4 PDFDokument94 SeitenAudit Practice and Assurance Services - A1.4 PDFFRANCOIS NKUNDIMANANoch keine Bewertungen

- School of Business, Economics and Management Bps430: Audit Practice and Performance Review Chapter 4: The Theory of AuditingDokument73 SeitenSchool of Business, Economics and Management Bps430: Audit Practice and Performance Review Chapter 4: The Theory of AuditingChibwe ChinyamaNoch keine Bewertungen

- Week 1 Overview of Audit - ACTG411 Assurance Principles, Professional Ethics & Good GovDokument6 SeitenWeek 1 Overview of Audit - ACTG411 Assurance Principles, Professional Ethics & Good GovMarilou PanisalesNoch keine Bewertungen

- Sabid - MC Neill - Bsma - 4 - I Am Lost! I Know I UnderstandDokument11 SeitenSabid - MC Neill - Bsma - 4 - I Am Lost! I Know I UnderstandMC NEILL SABIDNoch keine Bewertungen

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsVon EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNoch keine Bewertungen

- Storyline Missions: - Checkpoint Charlie (Checkpoint Race)Dokument1 SeiteStoryline Missions: - Checkpoint Charlie (Checkpoint Race)Azizul AviNoch keine Bewertungen

- Tax CalculatorDokument1 SeiteTax CalculatorAzizul AviNoch keine Bewertungen

- IFRS 10 SummaryDokument8 SeitenIFRS 10 SummarykonyatanNoch keine Bewertungen

- Hot Topics in TP Audits November 2018Dokument28 SeitenHot Topics in TP Audits November 2018Azizul AviNoch keine Bewertungen

- Sonali Bank's Internal Control & Compliance PolicyDokument91 SeitenSonali Bank's Internal Control & Compliance PolicyAzizul AviNoch keine Bewertungen

- Nvestment Nvironment: 1.1. Introduction To InvestmentDokument12 SeitenNvestment Nvironment: 1.1. Introduction To InvestmentAzizul AviNoch keine Bewertungen

- Model TestDokument35 SeitenModel TestAzizul AviNoch keine Bewertungen

- Nvestment Nvironment: 1.1. Introduction To InvestmentDokument12 SeitenNvestment Nvironment: 1.1. Introduction To InvestmentAzizul AviNoch keine Bewertungen

- Letter of Transmittal and Term Paper ReportDokument4 SeitenLetter of Transmittal and Term Paper ReportAzizul AviNoch keine Bewertungen

- Evsjv 'K M Ru: Iwr÷Vw© Bs WW G-1Dokument20 SeitenEvsjv 'K M Ru: Iwr÷Vw© Bs WW G-1Azizul AviNoch keine Bewertungen

- Computer BasicsDokument11 SeitenComputer BasicsAzizul AviNoch keine Bewertungen

- Letter of Transmittal: Submission of Term Paper Report EntitledDokument3 SeitenLetter of Transmittal: Submission of Term Paper Report EntitledAzizul AviNoch keine Bewertungen

- Cover PageDokument1 SeiteCover PageAzizul AviNoch keine Bewertungen

- Advanced Accounting II Managerial AccountingDokument1 SeiteAdvanced Accounting II Managerial AccountingAzizul AviNoch keine Bewertungen

- Letter of Transmittal: Submission of Term Paper Report EntitledDokument3 SeitenLetter of Transmittal: Submission of Term Paper Report EntitledAzizul AviNoch keine Bewertungen

- Back CoverDokument1 SeiteBack CoverAzizul AviNoch keine Bewertungen

- FormulasDokument19 SeitenFormulasAzizul AviNoch keine Bewertungen

- Front CoverDokument1 SeiteFront CoverAzizul AviNoch keine Bewertungen

- Audit Approach & BibliographyDokument1 SeiteAudit Approach & BibliographyAzizul AviNoch keine Bewertungen

- Front CoverDokument1 SeiteFront CoverAzizul AviNoch keine Bewertungen

- Syllabus of Application Level For ICAB PDFDokument27 SeitenSyllabus of Application Level For ICAB PDFcric6688Noch keine Bewertungen

- Forensic Accounting ArticleDokument8 SeitenForensic Accounting ArticleAzizul AviNoch keine Bewertungen

- Syllabus of Knowledge Level For ICABDokument24 SeitenSyllabus of Knowledge Level For ICABhridimamalik100% (2)

- Financial Accounting Syllabus PDFDokument6 SeitenFinancial Accounting Syllabus PDFAzizul AviNoch keine Bewertungen

- Weekend & Weekday Class ScheduleDokument1 SeiteWeekend & Weekday Class ScheduleAzizul AviNoch keine Bewertungen

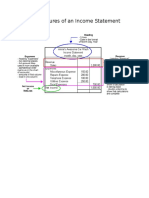

- Key Features in Come StatDokument1 SeiteKey Features in Come StatAzizul AviNoch keine Bewertungen

- Brightline Guiding PrinciplesDokument16 SeitenBrightline Guiding PrinciplesdjozinNoch keine Bewertungen

- 2 - Nested IFDokument8 Seiten2 - Nested IFLoyd DefensorNoch keine Bewertungen

- Terminología Sobre Reducción de Riesgo de DesastresDokument43 SeitenTerminología Sobre Reducción de Riesgo de DesastresJ. Mario VeraNoch keine Bewertungen

- Letter of Recommendation For Nicolas Hallett From Big Ten Network's Casey Peterson.Dokument1 SeiteLetter of Recommendation For Nicolas Hallett From Big Ten Network's Casey Peterson.Nic HallettNoch keine Bewertungen

- C - Official Coast HandbookDokument15 SeitenC - Official Coast HandbookSofia FreundNoch keine Bewertungen

- A Research About The Canteen SatisfactioDokument50 SeitenA Research About The Canteen SatisfactioJakeny Pearl Sibugan VaronaNoch keine Bewertungen

- PNW 0605Dokument12 SeitenPNW 0605sunf496Noch keine Bewertungen

- Lirik and Chord LaguDokument5 SeitenLirik and Chord LaguRyan D'Stranger UchihaNoch keine Bewertungen

- Entrepreneurship and EconomicDokument2 SeitenEntrepreneurship and EconomicSukruti BajajNoch keine Bewertungen

- Diagram of Thermal RunawayDokument9 SeitenDiagram of Thermal RunawayVeera ManiNoch keine Bewertungen

- For-tea Tea Parlour Marketing Strategy Targets 40+ DemographicDokument7 SeitenFor-tea Tea Parlour Marketing Strategy Targets 40+ Demographicprynk_cool2702Noch keine Bewertungen

- Amos Code SystemDokument17 SeitenAmos Code SystemViktor KarlashevychNoch keine Bewertungen

- TransformerDokument50 SeitenTransformerبنیاد پرست100% (8)

- United States Court of Appeals, Third CircuitDokument3 SeitenUnited States Court of Appeals, Third CircuitScribd Government DocsNoch keine Bewertungen

- MT R 108 000 0 000000-0 DHHS B eDokument68 SeitenMT R 108 000 0 000000-0 DHHS B eRafal WojciechowskiNoch keine Bewertungen

- Norms and specifications for distribution transformer, DG set, street light poles, LED lights and high mast lightDokument4 SeitenNorms and specifications for distribution transformer, DG set, street light poles, LED lights and high mast lightKumar AvinashNoch keine Bewertungen

- Company Profi Le: IHC HytopDokument13 SeitenCompany Profi Le: IHC HytopHanzil HakeemNoch keine Bewertungen

- Fluke - Dry Well CalibratorDokument24 SeitenFluke - Dry Well CalibratorEdy WijayaNoch keine Bewertungen

- Broschuere Unternehmen Screen PDFDokument16 SeitenBroschuere Unternehmen Screen PDFAnonymous rAFSAGDAEJNoch keine Bewertungen

- What Role Can IS Play in The Pharmaceutical Industry?Dokument4 SeitenWhat Role Can IS Play in The Pharmaceutical Industry?Đức NguyễnNoch keine Bewertungen

- Structures Module 3 Notes FullDokument273 SeitenStructures Module 3 Notes Fulljohnmunjuga50Noch keine Bewertungen

- EE3331C Feedback Control Systems L1: Overview: Arthur TAYDokument28 SeitenEE3331C Feedback Control Systems L1: Overview: Arthur TAYpremsanjith subramani0% (1)

- DSP Lab Record Convolution ExperimentsDokument25 SeitenDSP Lab Record Convolution ExperimentsVishwanand ThombareNoch keine Bewertungen