Das könnte Ihnen auch gefallen

- Paying Your Income Taxes Note Taking GuideDokument4 SeitenPaying Your Income Taxes Note Taking GuideMaggie ScottNoch keine Bewertungen

- Chapter 05 SolutionsDokument7 SeitenChapter 05 SolutionsShahnawaz KhanNoch keine Bewertungen

- Assignment 1 - 2021 - 2022Dokument4 SeitenAssignment 1 - 2021 - 2022Assya El MoukademNoch keine Bewertungen

- Acco 365 Review Class QuestionsDokument31 SeitenAcco 365 Review Class QuestionsHeyue XiaoNoch keine Bewertungen

- Dividend and BondsDokument3 SeitenDividend and BondsJanuary Ann Bete100% (1)

- Unit 1 - QuestionsDokument4 SeitenUnit 1 - QuestionsMohanNoch keine Bewertungen

- Intercorporate - Class Exercises - ANSWERSDokument5 SeitenIntercorporate - Class Exercises - ANSWERSKhushbooNoch keine Bewertungen

- Ratio Analysis Numericals Including Reverse RatiosDokument6 SeitenRatio Analysis Numericals Including Reverse RatiosFunny ManNoch keine Bewertungen

- Analysis of FSDokument28 SeitenAnalysis of FSHaseeb TariqNoch keine Bewertungen

- Tax On PartnershipDokument3 SeitenTax On PartnershipPrankyJellyNoch keine Bewertungen

- ACC 3013 Revision Material..Dokument22 SeitenACC 3013 Revision Material..falnuaimi001Noch keine Bewertungen

- Presented by Archana Gupta 0221031 Bharat Gaikwad 0221023Dokument12 SeitenPresented by Archana Gupta 0221031 Bharat Gaikwad 0221023Bharat GaikwadNoch keine Bewertungen

- Taxation of CompaniesDokument10 SeitenTaxation of CompaniesnikhilramaneNoch keine Bewertungen

- Solved Ballou Corporation Distributes 200 000 in Cash To Its Sharehold PDFDokument1 SeiteSolved Ballou Corporation Distributes 200 000 in Cash To Its Sharehold PDFAnbu jaromiaNoch keine Bewertungen

- Session 8 Intra-Group Transactions-8eDokument49 SeitenSession 8 Intra-Group Transactions-8eMedonka PeirisNoch keine Bewertungen

- Entity Tax ExamDokument7 SeitenEntity Tax ExamWesley JacksonNoch keine Bewertungen

- Managerial AccountingDokument1 SeiteManagerial AccountingMaribel ZafeNoch keine Bewertungen

- Tutorial 3Dokument4 SeitenTutorial 3bolaemil20Noch keine Bewertungen

- Special Allowable Itemized DeductionsDokument13 SeitenSpecial Allowable Itemized DeductionsSandia EspejoNoch keine Bewertungen

- FAWCM - Cash Flow 2Dokument29 SeitenFAWCM - Cash Flow 2Jake RoosenbloomNoch keine Bewertungen

- SARIEPHINE GRACE ARAS-ACTIVITY No 2 Corporate Income TaxDokument8 SeitenSARIEPHINE GRACE ARAS-ACTIVITY No 2 Corporate Income TaxSariephine Grace ArasNoch keine Bewertungen

- UNIT-4 - Income-From-BusinessDokument114 SeitenUNIT-4 - Income-From-BusinessGuinevereNoch keine Bewertungen

- Questions Number One P LTD and Its Subsidiary Consolidated Income Statement For The Year Ended 31 December 2003Dokument29 SeitenQuestions Number One P LTD and Its Subsidiary Consolidated Income Statement For The Year Ended 31 December 2003JOHN KAMANDANoch keine Bewertungen

- AK Mock MT ProbDokument7 SeitenAK Mock MT ProbJJCookieNoch keine Bewertungen

- PartnershipDokument13 SeitenPartnershipAdrian RamsundarNoch keine Bewertungen

- Common Size Statement AnalysisDokument2 SeitenCommon Size Statement AnalysisRevati ShindeNoch keine Bewertungen

- Seatwork 5: Application A. Owner's EquityDokument7 SeitenSeatwork 5: Application A. Owner's EquityAngela GarciaNoch keine Bewertungen

- Free Cash Flow From EBITDA Excel TemplateDokument5 SeitenFree Cash Flow From EBITDA Excel TemplatePhuongwater Le Thanh PhuongNoch keine Bewertungen

- What Are The Advantages To A Business of Being Formed As A Company? What Are The Disadvantages?Dokument12 SeitenWhat Are The Advantages To A Business of Being Formed As A Company? What Are The Disadvantages?Nguyễn HoàngNoch keine Bewertungen

- BBS 1st Year QuestionDokument2 SeitenBBS 1st Year Questionsatya100% (1)

- Cash Flow StatementDokument9 SeitenCash Flow StatementPiyush MalaniNoch keine Bewertungen

- Chapter 17 & 18 SolutionsDokument4 SeitenChapter 17 & 18 SolutionsSheena CarrouthersNoch keine Bewertungen

- Week 5 Class Tutorial Question 2220Dokument3 SeitenWeek 5 Class Tutorial Question 2220Aisyahrahyu HafilahNoch keine Bewertungen

- Dividend Policy Gorden, Walter & MM Model Practice QuestionsDokument1 SeiteDividend Policy Gorden, Walter & MM Model Practice QuestionsAmjad AliNoch keine Bewertungen

- Dividend Policy Gorden, Walter & MM Model Practice QuestionsDokument1 SeiteDividend Policy Gorden, Walter & MM Model Practice QuestionsAmjad AliNoch keine Bewertungen

- Assessment of CompaniesDokument5 SeitenAssessment of Companiesmohanraokp22790% (1)

- Seatwork Problem 1Dokument11 SeitenSeatwork Problem 1Zihr EllerycNoch keine Bewertungen

- AFM IBSB Leverages WordDokument16 SeitenAFM IBSB Leverages WordSangeetha K SNoch keine Bewertungen

- Exercises On Implementation of DCF ApproachDokument10 SeitenExercises On Implementation of DCF ApproachVincenzoPizzulliNoch keine Bewertungen

- Dividend Policy QuestionDokument3 SeitenDividend Policy Questionraju kumarNoch keine Bewertungen

- Buscom - Subsequent-To-The-Date-Of-Acquisition - Cost MethodDokument46 SeitenBuscom - Subsequent-To-The-Date-Of-Acquisition - Cost MethodJohn Stephen PendonNoch keine Bewertungen

- Income Taxation Answer ExamDokument5 SeitenIncome Taxation Answer Examyezaquera100% (1)

- CBSE Class 12 Accountancy Accounting Ratios WorksheetDokument3 SeitenCBSE Class 12 Accountancy Accounting Ratios WorksheetJenneil CarmichaelNoch keine Bewertungen

- Tax 1 1Dokument1 SeiteTax 1 1Krizel rochaNoch keine Bewertungen

- Amounting 5,00,000.: Exelusively Ordinary Company Equity Capital. Debentures. Can Raise Capital FinancingDokument10 SeitenAmounting 5,00,000.: Exelusively Ordinary Company Equity Capital. Debentures. Can Raise Capital FinancingMohit RanaNoch keine Bewertungen

- Traditional Theory Approach: Illustrations 1Dokument7 SeitenTraditional Theory Approach: Illustrations 1PRAMOD VNoch keine Bewertungen

- GAMDOORDokument2 SeitenGAMDOORRashpreet PandiNoch keine Bewertungen

- RDGRT 4 Erte 4Dokument3 SeitenRDGRT 4 Erte 4Lorelyn TriciaNoch keine Bewertungen

- Capital StructureDokument21 SeitenCapital StructureRameen Jawad MalikNoch keine Bewertungen

- M&M Capital Structure WACC & Value CreationDokument15 SeitenM&M Capital Structure WACC & Value CreationsdsdvdgNoch keine Bewertungen

- Tax DeductionsDokument4 SeitenTax DeductionsAnonymous LC5kFdtcNoch keine Bewertungen

- Forecasting ProblemsDokument3 SeitenForecasting ProblemsJimmyChaoNoch keine Bewertungen

- Total Assets Net Income Total Debt Interest Expense Income Tax Expense Total Owners EquityDokument29 SeitenTotal Assets Net Income Total Debt Interest Expense Income Tax Expense Total Owners EquityshabNoch keine Bewertungen

- HI 5020 Corporate Accounting: Session 8a Intra-Group TransactionsDokument15 SeitenHI 5020 Corporate Accounting: Session 8a Intra-Group TransactionsFeku RamNoch keine Bewertungen

- AYB320 0122 TrustsTutorialDokument20 SeitenAYB320 0122 TrustsTutorialLinh ĐanNoch keine Bewertungen

- Cash Flow (Exercise)Dokument5 SeitenCash Flow (Exercise)abhishekvora7598752100% (1)

- Exercise CorporationDokument3 SeitenExercise CorporationJefferson MañaleNoch keine Bewertungen

- IAS (7) Cashflow-6-3-2020Dokument32 SeitenIAS (7) Cashflow-6-3-2020Dana HasanNoch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- Omb No. 1545-0008 Omb No. 1545-0008Dokument2 SeitenOmb No. 1545-0008 Omb No. 1545-0008Luke NyeNoch keine Bewertungen

- Biswana TH Guha: I. R. Technology Services Pvt. LTDDokument1 SeiteBiswana TH Guha: I. R. Technology Services Pvt. LTDRoma BeheraNoch keine Bewertungen

- BIR Ruling (DA-392-98)Dokument3 SeitenBIR Ruling (DA-392-98)Jeffrey JosolNoch keine Bewertungen

- BE-Way Bill SystemDokument2 SeitenBE-Way Bill SystemKrishna Computer DakorNoch keine Bewertungen

- Income and Business TaxationDokument44 SeitenIncome and Business TaxationBeverly EroyNoch keine Bewertungen

- MW 507Dokument2 SeitenMW 507sosureyNoch keine Bewertungen

- Business and Transfer TaxationDokument22 SeitenBusiness and Transfer TaxationNicole Rivera100% (1)

- UST GN 2011 - Taxation Law IndexDokument2 SeitenUST GN 2011 - Taxation Law IndexGhost100% (1)

- 40 Nippon Life V CIRDokument2 Seiten40 Nippon Life V CIRMae SampangNoch keine Bewertungen

- Resale CertificateDokument1 SeiteResale CertificateplayerwheelNoch keine Bewertungen

- Pay Slip PDFDokument1 SeitePay Slip PDFasif MehmoodNoch keine Bewertungen

- .. .. PMZK Content TMP 1553744109-1649303844Dokument1 Seite.. .. PMZK Content TMP 1553744109-1649303844Nur AtiqahNoch keine Bewertungen

- Impact of GST On GDPDokument9 SeitenImpact of GST On GDPAnshaj GuptaNoch keine Bewertungen

- Income Tax Computation For Corporate TaxpayersDokument79 SeitenIncome Tax Computation For Corporate TaxpayersPATATASNoch keine Bewertungen

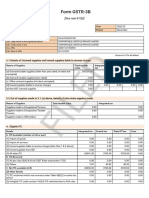

- Filed: Form GSTR-3BDokument2 SeitenFiled: Form GSTR-3Bkrishswat7912Noch keine Bewertungen

- 1 3+part+2Dokument28 Seiten1 3+part+2jaspreet kaurNoch keine Bewertungen

- Invitation Training TaxDokument1 SeiteInvitation Training TaxharoldpsbNoch keine Bewertungen

- Employee Pay SlipDokument1 SeiteEmployee Pay SlipTiyyagura RoofusreddyNoch keine Bewertungen

- InvoiceDokument1 SeiteInvoiceLAKHAN TRIVEDINoch keine Bewertungen

- Joijamison 2019taxes PDFDokument26 SeitenJoijamison 2019taxes PDFrose ownes100% (1)

- 030 - InV - Arise (Borescope)Dokument2 Seiten030 - InV - Arise (Borescope)Rony YudaNoch keine Bewertungen

- Salary Income Tax Calculation in EthiopiaDokument4 SeitenSalary Income Tax Calculation in EthiopiaMulatu Teshome95% (37)

- Tax Invoice: Enertech Electric Enterprises PVT LTD No S-2201073Dokument1 SeiteTax Invoice: Enertech Electric Enterprises PVT LTD No S-2201073karthik achudhanNoch keine Bewertungen

- NCH Customer Support Services, Inc. PayslipDokument1 SeiteNCH Customer Support Services, Inc. PayslipTrainer EntainNoch keine Bewertungen

- RMC 2019 No. 142 eDST Balance Adjustment As An Option For Recovery of Erroneously Deducted DSTDokument2 SeitenRMC 2019 No. 142 eDST Balance Adjustment As An Option For Recovery of Erroneously Deducted DSTBien Bowie A. CortezNoch keine Bewertungen

- 2.1 Visualization and Key Info For Capital Assets and CCADokument2 Seiten2.1 Visualization and Key Info For Capital Assets and CCABob BillyNoch keine Bewertungen

- Form 4A - GCT Returns PDFDokument2 SeitenForm 4A - GCT Returns PDFNicquainCTNoch keine Bewertungen

- TDS Story - CA Amit MahajanDokument6 SeitenTDS Story - CA Amit MahajanUday tomarNoch keine Bewertungen

- Non-Tax Filer Student 2021 Certification 23-24Dokument1 SeiteNon-Tax Filer Student 2021 Certification 23-24Kamal GroverNoch keine Bewertungen