Das könnte Ihnen auch gefallen

- Financial UnderwritingDokument19 SeitenFinancial UnderwritingPritish PatnaikNoch keine Bewertungen

- Recruitment of Advisors in IciciDokument77 SeitenRecruitment of Advisors in Icicipadamheena123Noch keine Bewertungen

- Blood Pressure Log 04Dokument2 SeitenBlood Pressure Log 04Yousab KaldasNoch keine Bewertungen

- Strategic Audit For Transportation and Engineering Company For Tires (Trenco)Dokument16 SeitenStrategic Audit For Transportation and Engineering Company For Tires (Trenco)Yousab KaldasNoch keine Bewertungen

- Strategic Audit WorksheetDokument1 SeiteStrategic Audit WorksheetYousab KaldasNoch keine Bewertungen

- Challan Form OEC App Fee 500 PDFDokument1 SeiteChallan Form OEC App Fee 500 PDFsaleem_hazim100% (1)

- CLAIM Managment in LICDokument61 SeitenCLAIM Managment in LICChetan Godambe67% (3)

- Underwriting & Claim ManagementDokument222 SeitenUnderwriting & Claim ManagementPutin PhyNoch keine Bewertungen

- Reading Material - Insurance Business Barter Exchange HFC and Mutual Fund Busines Set IIIDokument75 SeitenReading Material - Insurance Business Barter Exchange HFC and Mutual Fund Busines Set IIIdhruv khandelwalNoch keine Bewertungen

- Que 1Dokument3 SeitenQue 1Sammy SamNoch keine Bewertungen

- Insurance Industry OverviewDokument42 SeitenInsurance Industry OverviewAkhilesh desaiNoch keine Bewertungen

- 18 Pages Summary - Book PDFDokument18 Seiten18 Pages Summary - Book PDFSanjeev SinghNoch keine Bewertungen

- Tbe Revision 20181019Dokument66 SeitenTbe Revision 20181019Sarah MadzliNoch keine Bewertungen

- Executive SummaryDokument25 SeitenExecutive SummaryRitika MahenNoch keine Bewertungen

- ReInsurance FinalDokument93 SeitenReInsurance FinalArushi Agrawal Garg100% (3)

- Insurance Risk ManagementDokument17 SeitenInsurance Risk ManagementWong Wu SeanNoch keine Bewertungen

- General Insurance UwDokument90 SeitenGeneral Insurance UwsushantducatiNoch keine Bewertungen

- Irda Ic 33 EnglishDokument8 SeitenIrda Ic 33 EnglishlicarvindNoch keine Bewertungen

- How Covid Is Changing The Indian Life Insurance Industry?Dokument11 SeitenHow Covid Is Changing The Indian Life Insurance Industry?03 Archit Babel SYBBINoch keine Bewertungen

- Indian Insurance SectorDokument32 SeitenIndian Insurance Sectorbanirumi100% (2)

- Critical Analysis of Life and General Insurance Proposal Form and Policy DocumentsDokument23 SeitenCritical Analysis of Life and General Insurance Proposal Form and Policy Documentssaritha jainNoch keine Bewertungen

- POI MaterialDokument11 SeitenPOI MaterialMukesh ChoudharyNoch keine Bewertungen

- Research Project ReportDokument85 SeitenResearch Project ReportSujeet GuptaNoch keine Bewertungen

- Basics of Insurance HandoutDokument11 SeitenBasics of Insurance Handoutsumit.zara1993Noch keine Bewertungen

- Summer Training Project Report ON Selection and Recruitment: Shah Satnam Ji P.G. Girl'S College, Sirsa (Haryana)Dokument86 SeitenSummer Training Project Report ON Selection and Recruitment: Shah Satnam Ji P.G. Girl'S College, Sirsa (Haryana)Paras SukhijaNoch keine Bewertungen

- Understanding Life Insurance Underwriting BasicsDokument24 SeitenUnderstanding Life Insurance Underwriting BasicsswatishouryaNoch keine Bewertungen

- Bajaj AllanceDokument92 SeitenBajaj AllanceRajat KatimaniNoch keine Bewertungen

- Insurance Secuirity, Withdrawal NotesDokument50 SeitenInsurance Secuirity, Withdrawal NotesWong Wu SeanNoch keine Bewertungen

- How Covid Is Changing The Indian Life Insurance Industry?Dokument10 SeitenHow Covid Is Changing The Indian Life Insurance Industry?03 Archit Babel SYBBINoch keine Bewertungen

- Customer Satisfaction Level of Lic ProductsDokument90 SeitenCustomer Satisfaction Level of Lic ProductsPiyush Soni100% (2)

- UUM-BWRR3033: Risk Management-Chapter 08 Risk FinancingDokument14 SeitenUUM-BWRR3033: Risk Management-Chapter 08 Risk FinancingRodziah AhmadNoch keine Bewertungen

- Frauds in Life Insurance and IrdaDokument59 SeitenFrauds in Life Insurance and IrdaVishal MulchandaniNoch keine Bewertungen

- ©rahul MahatoDokument3 Seiten©rahul MahatoE-TECH SOFTWARE SOLUTIONS PVT L.T.DNoch keine Bewertungen

- ProjectDokument52 SeitenProjectPranali WahaneNoch keine Bewertungen

- CHAPTER 1 IntroductionDokument6 SeitenCHAPTER 1 IntroductionPrerana AroraNoch keine Bewertungen

- Assign 1Dokument11 SeitenAssign 1Rakshi BegumNoch keine Bewertungen

- Promotional StrategiesDokument43 SeitenPromotional StrategiesDhruv RajpalNoch keine Bewertungen

- Insurance BusinessDokument69 SeitenInsurance BusinessMittal Kirti MukeshNoch keine Bewertungen

- Underwriting of General InsuranceDokument42 SeitenUnderwriting of General InsurancevandanaNoch keine Bewertungen

- Project Report ON: University of MumbaiDokument55 SeitenProject Report ON: University of MumbaiNayak SandeshNoch keine Bewertungen

- A Brief Overview of Impact of Pandemic On Insurance Industry in PakistanDokument2 SeitenA Brief Overview of Impact of Pandemic On Insurance Industry in PakistanAhsan NisarNoch keine Bewertungen

- Re InsuranceDokument5 SeitenRe Insurancenetishrai88Noch keine Bewertungen

- Risk Management Lecture Note CH 3-7Dokument77 SeitenRisk Management Lecture Note CH 3-7Meklit TenaNoch keine Bewertungen

- Arti RaniDokument73 SeitenArti Raniarpita1790Noch keine Bewertungen

- Icici Bank Project ReportDokument68 SeitenIcici Bank Project ReportNeeraj PurohitNoch keine Bewertungen

- Dbfi303 - Principles and Practices of InsuranceDokument10 SeitenDbfi303 - Principles and Practices of Insurancevikash rajNoch keine Bewertungen

- Consumer Awareness Regarding PNB MetlifeDokument51 SeitenConsumer Awareness Regarding PNB MetlifeKirti Jindal100% (1)

- Banking RPDokument12 SeitenBanking RPElsa ShaikhNoch keine Bewertungen

- 7 InsuranceDokument10 Seiten7 InsuranceLynner Anne DeytaNoch keine Bewertungen

- Benefits of Insurance PoliciesDokument17 SeitenBenefits of Insurance PoliciesSaksham MathurNoch keine Bewertungen

- Why Life Insuranceshouldbe MandatoryDokument6 SeitenWhy Life Insuranceshouldbe MandatoryMaduwanthanNoch keine Bewertungen

- Basics of Insurance HandoutDokument10 SeitenBasics of Insurance HandoutPradeep NadarNoch keine Bewertungen

- Improving effectiveness of ULIP policies in Insurance IndustryDokument8 SeitenImproving effectiveness of ULIP policies in Insurance IndustrymanojlongNoch keine Bewertungen

- Chapter 9 10Dokument9 SeitenChapter 9 10alessiamenNoch keine Bewertungen

- MF0018Dokument9 SeitenMF0018anahheed salahNoch keine Bewertungen

- SUMMER TRAINING REPORT. MoniDokument73 SeitenSUMMER TRAINING REPORT. MoniManideepa DeyNoch keine Bewertungen

- Insurance Advisor Summer Training ReportDokument40 SeitenInsurance Advisor Summer Training ReportSaroj KumarNoch keine Bewertungen

- Financial Risk ManagementDokument34 SeitenFinancial Risk Managementakash agarwalNoch keine Bewertungen

- Uncertainity in GI & Solvency Issues - PI MajmudarDokument15 SeitenUncertainity in GI & Solvency Issues - PI MajmudarRajendra SinghNoch keine Bewertungen

- Awareness of Micro Insurance Product in Patan District: Mr. Mitul M. Deliya Dr. Karshanbhai N. PatelDokument21 SeitenAwareness of Micro Insurance Product in Patan District: Mr. Mitul M. Deliya Dr. Karshanbhai N. PatelAnonymous 6x5cTCmNoch keine Bewertungen

- Comparitive Study ICICI & HDFCDokument94 SeitenComparitive Study ICICI & HDFCshah faisal75% (16)

- Bhuvaneshwar ReporytDokument65 SeitenBhuvaneshwar Reporytrahulsogani123Noch keine Bewertungen

- RM Project On IciciDokument55 SeitenRM Project On IciciRaj RanveerNoch keine Bewertungen

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterVon EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNoch keine Bewertungen

- Blood Pressure Log 02Dokument1 SeiteBlood Pressure Log 02Yousab KaldasNoch keine Bewertungen

- Tri Calcium Phosphate FsDokument4 SeitenTri Calcium Phosphate Fsdrg. Rifqie Al HarisNoch keine Bewertungen

- Watercolor Brush Precision Practice Sheet by Nourane OwaisDokument1 SeiteWatercolor Brush Precision Practice Sheet by Nourane OwaisYousab KaldasNoch keine Bewertungen

- Basic Leadership Skills PDFDokument36 SeitenBasic Leadership Skills PDFnouman1981Noch keine Bewertungen

- Blood Pressure Log 30Dokument2 SeitenBlood Pressure Log 30Yousab KaldasNoch keine Bewertungen

- Blood Pressure Log 31Dokument1 SeiteBlood Pressure Log 31Yousab KaldasNoch keine Bewertungen

- Blood Pressure Log 03Dokument1 SeiteBlood Pressure Log 03Yousab KaldasNoch keine Bewertungen

- Blood Pressure Log 18Dokument1 SeiteBlood Pressure Log 18Yousab KaldasNoch keine Bewertungen

- A Case Study Strategic Audit: (XYZ Company Inc.)Dokument27 SeitenA Case Study Strategic Audit: (XYZ Company Inc.)abraamNoch keine Bewertungen

- 0 Amazon PresentationDokument9 Seiten0 Amazon PresentationYousab KaldasNoch keine Bewertungen

- Yasmina Answer Model-Final EditionDokument21 SeitenYasmina Answer Model-Final EditionYousab KaldasNoch keine Bewertungen

- First: Generic Strategies Generic Competitive Strategies:: Product DifferentiationDokument8 SeitenFirst: Generic Strategies Generic Competitive Strategies:: Product DifferentiationYousab KaldasNoch keine Bewertungen

- Tamer Shawer Strategic MGMT V3 - 02Dokument35 SeitenTamer Shawer Strategic MGMT V3 - 02Yousab KaldasNoch keine Bewertungen

- Strat I GiesDokument11 SeitenStrat I GiesYousab KaldasNoch keine Bewertungen

- Corporate Culture Dimensions & Hofstede's ModelDokument4 SeitenCorporate Culture Dimensions & Hofstede's ModelMina Awad FouadNoch keine Bewertungen

- The Functional Structure 2. Divisional Structure 3. The Strategic Business Unit (SBU) Structure 4. The Matrix StructureDokument17 SeitenThe Functional Structure 2. Divisional Structure 3. The Strategic Business Unit (SBU) Structure 4. The Matrix StructureYousab KaldasNoch keine Bewertungen

- Key Financial Ratios (M.N) FinialDokument10 SeitenKey Financial Ratios (M.N) FinialYousab KaldasNoch keine Bewertungen

- Porters 5 ForcesDokument4 SeitenPorters 5 ForcesYousab KaldasNoch keine Bewertungen

- Marketing Plan (Dina)Dokument9 SeitenMarketing Plan (Dina)Yousab KaldasNoch keine Bewertungen

- HRM BriefDokument16 SeitenHRM BriefYousab KaldasNoch keine Bewertungen

- Some Types of CultureDokument10 SeitenSome Types of CultureYousab KaldasNoch keine Bewertungen

- Suggestions For Case AnalysisDokument27 SeitenSuggestions For Case AnalysisYousab KaldasNoch keine Bewertungen

- Grand StrategyDokument3 SeitenGrand StrategyYousab KaldasNoch keine Bewertungen

- Model For Solving Comprehensive ExamDokument23 SeitenModel For Solving Comprehensive ExamYousab KaldasNoch keine Bewertungen

- Internal ScanningDokument9 SeitenInternal ScanningYousab KaldasNoch keine Bewertungen

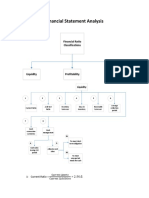

- Financial Statement AnalysisDokument5 SeitenFinancial Statement AnalysisYousab KaldasNoch keine Bewertungen

- Arab Academy For Science and Technology: Case Analysis: XYZ CompanyDokument16 SeitenArab Academy For Science and Technology: Case Analysis: XYZ CompanyYousab KaldasNoch keine Bewertungen

- Cub Cadet 1650 PDFDokument46 SeitenCub Cadet 1650 PDFkbrckac33% (3)

- E.Coli Coliforms Chromogenic Medium: CAT Nº: 1340Dokument2 SeitenE.Coli Coliforms Chromogenic Medium: CAT Nº: 1340Juan Manuel Ramos ReyesNoch keine Bewertungen

- Assessment: Bipolar DisorderDokument2 SeitenAssessment: Bipolar DisorderMirjana StevanovicNoch keine Bewertungen

- Checklist For HR Audit Policy and ProceduresDokument3 SeitenChecklist For HR Audit Policy and ProcedureskrovvidiprasadaraoNoch keine Bewertungen

- Course Title: Cost Accounting Course Code:441 BBA Program Lecture-3Dokument20 SeitenCourse Title: Cost Accounting Course Code:441 BBA Program Lecture-3Tanvir Ahmed ChowdhuryNoch keine Bewertungen

- ControllingDokument8 SeitenControllingAnjo Pasiolco Canicosa100% (2)

- Vaccination Consent Form: Tetanus, Diphtheria / Inactivated Polio Vaccine (DTP) & Meningococcal ACWY (Men ACWY)Dokument2 SeitenVaccination Consent Form: Tetanus, Diphtheria / Inactivated Polio Vaccine (DTP) & Meningococcal ACWY (Men ACWY)meghaliNoch keine Bewertungen

- Credit Card Statement: Payment Information Account SummaryDokument4 SeitenCredit Card Statement: Payment Information Account SummaryShawn McKennanNoch keine Bewertungen

- Reviewer in Intermediate Accounting IDokument9 SeitenReviewer in Intermediate Accounting ICzarhiena SantiagoNoch keine Bewertungen

- Volatility Clustering, Leverage Effects and Risk-Return Trade-Off in The Nigerian Stock MarketDokument14 SeitenVolatility Clustering, Leverage Effects and Risk-Return Trade-Off in The Nigerian Stock MarketrehanbtariqNoch keine Bewertungen

- Ward A. Thompson v. City of Lawrence, Kansas Ron Olin, Chief of Police Jerry Wells, District Attorney Frank Diehl, David Davis, Kevin Harmon, Mike Hall, Ray Urbanek, Jim Miller, Bob Williams, Craig Shanks, John Lewis, Jack Cross, Catherine Kelley, Dan Ward, James Haller, Dave Hubbell and Matilda Woody, Frances S. Wisdom v. City of Lawrence, Kansas Ron Olin, Chief of Police David Davis, Mike Hall, Jim Miller, Bob Williams, Craig Shanks, John L. Lewis, Jack Cross, Kevin Harmon, Catherine Kelley, Dan Ward and James Haller, Jr., 58 F.3d 1511, 10th Cir. (1995)Dokument8 SeitenWard A. Thompson v. City of Lawrence, Kansas Ron Olin, Chief of Police Jerry Wells, District Attorney Frank Diehl, David Davis, Kevin Harmon, Mike Hall, Ray Urbanek, Jim Miller, Bob Williams, Craig Shanks, John Lewis, Jack Cross, Catherine Kelley, Dan Ward, James Haller, Dave Hubbell and Matilda Woody, Frances S. Wisdom v. City of Lawrence, Kansas Ron Olin, Chief of Police David Davis, Mike Hall, Jim Miller, Bob Williams, Craig Shanks, John L. Lewis, Jack Cross, Kevin Harmon, Catherine Kelley, Dan Ward and James Haller, Jr., 58 F.3d 1511, 10th Cir. (1995)Scribd Government DocsNoch keine Bewertungen

- Importance of Time Management To Senior High School Honor StudentsDokument7 SeitenImportance of Time Management To Senior High School Honor StudentsBien LausaNoch keine Bewertungen

- No-Vacation NationDokument24 SeitenNo-Vacation NationCenter for Economic and Policy Research91% (54)

- ESS 4104 AssignmentDokument9 SeitenESS 4104 AssignmentSamlall RabindranauthNoch keine Bewertungen

- Apola Ose-Otura (Popoola PDFDokument2 SeitenApola Ose-Otura (Popoola PDFHowe JosephNoch keine Bewertungen

- International Waiver Attestation FormDokument1 SeiteInternational Waiver Attestation FormJiabao ZhengNoch keine Bewertungen

- BRT vs Light Rail Costs: Which is Cheaper to OperateDokument11 SeitenBRT vs Light Rail Costs: Which is Cheaper to Operatejas rovelo50% (2)

- Isha Hatha Yoga - Program Registration FormDokument2 SeitenIsha Hatha Yoga - Program Registration FormKeyur GadaNoch keine Bewertungen

- MASM Tutorial PDFDokument10 SeitenMASM Tutorial PDFShashankDwivediNoch keine Bewertungen

- The Beatles - Allan Kozinn Cap 8Dokument24 SeitenThe Beatles - Allan Kozinn Cap 8Keka LopesNoch keine Bewertungen

- Coal Bed Methane GasDokument10 SeitenCoal Bed Methane GasErrol SmytheNoch keine Bewertungen

- Motivate! 2 End-Of-Term Test Standard: Units 1-3Dokument6 SeitenMotivate! 2 End-Of-Term Test Standard: Units 1-3Oum Vibol SatyaNoch keine Bewertungen

- Corporate Process Management (CPM) & Control-EsDokument458 SeitenCorporate Process Management (CPM) & Control-EsKent LysellNoch keine Bewertungen

- Clique Pen's Marketing StrategyDokument10 SeitenClique Pen's Marketing StrategySAMBIT HALDER PGP 2018-20 BatchNoch keine Bewertungen

- European Vacancy and Recruitment Report 2012Dokument200 SeitenEuropean Vacancy and Recruitment Report 2012Joaquín Vicente Ramos RodríguezNoch keine Bewertungen

- Toyota TPMDokument23 SeitenToyota TPMchteo1976Noch keine Bewertungen

- Proceedings of The 2012 PNLG Forum: General AssemblyDokument64 SeitenProceedings of The 2012 PNLG Forum: General AssemblyPEMSEA (Partnerships in Environmental Management for the Seas of East Asia)Noch keine Bewertungen

- Alberta AwdNomineeDocs Case Circle BestMagazine NewTrailSpring2016Dokument35 SeitenAlberta AwdNomineeDocs Case Circle BestMagazine NewTrailSpring2016LucasNoch keine Bewertungen

- The Power of Compounding: Why It's the 8th Wonder of the WorldDokument5 SeitenThe Power of Compounding: Why It's the 8th Wonder of the WorldWaleed TariqNoch keine Bewertungen