Das könnte Ihnen auch gefallen

- Basic Finance-An Introduction To Financial Institutions Investments and Management 10th Edition Mayo Test BankDokument10 SeitenBasic Finance-An Introduction To Financial Institutions Investments and Management 10th Edition Mayo Test BankRobinson MojicaNoch keine Bewertungen

- Falin-Math of Finance and Investment 3 PDFDokument97 SeitenFalin-Math of Finance and Investment 3 PDFAlfred alegadoNoch keine Bewertungen

- BankingDokument377 SeitenBankingUzma Shafi100% (3)

- ACCA P4 Key Point Notes June 2010Dokument148 SeitenACCA P4 Key Point Notes June 2010wakomoli100% (2)

- Extrajudicial ForeclosureDokument23 SeitenExtrajudicial Foreclosurewin winNoch keine Bewertungen

- Asset Securitization by HuDokument22 SeitenAsset Securitization by HucherryflavaNoch keine Bewertungen

- Gsis V CaDokument1 SeiteGsis V CaTAU MU OFFICIALNoch keine Bewertungen

- Macalintal Vs Pet DigestDokument3 SeitenMacalintal Vs Pet DigestLei MorteraNoch keine Bewertungen

- Chapter 1: Introduction To Financial PlanningDokument71 SeitenChapter 1: Introduction To Financial PlanningSarojkumar ChhuraNoch keine Bewertungen

- Solution - Handout - Cash and Cash Equivalents - Inclusions and ExclusionsDokument5 SeitenSolution - Handout - Cash and Cash Equivalents - Inclusions and ExclusionsMaricon BerjaNoch keine Bewertungen

- Gold Loan ABCDokument44 SeitenGold Loan ABCakhilNoch keine Bewertungen

- Mortgage Servicing Fraud Forum PDFDokument125 SeitenMortgage Servicing Fraud Forum PDFboytoy 9774100% (1)

- Sanlakas vs. Executive SecretaryDokument2 SeitenSanlakas vs. Executive SecretaryNessalyn Mae Rosales Valencia100% (2)

- LA 2 Construction Contracts PDFDokument3 SeitenLA 2 Construction Contracts PDFliliNoch keine Bewertungen

- Development Bank of The Philippines v. Felipe Arcilla, G.R. No. 161397, 161436, June 30, 2005 Case DigestDokument1 SeiteDevelopment Bank of The Philippines v. Felipe Arcilla, G.R. No. 161397, 161436, June 30, 2005 Case DigestDes GerardoNoch keine Bewertungen

- RFBT - Chapter 8 - Ease of Doing BusinessDokument15 SeitenRFBT - Chapter 8 - Ease of Doing Businesslaythejoylunas21Noch keine Bewertungen

- Marcos vs. Manglapus Case DigestDokument2 SeitenMarcos vs. Manglapus Case DigestFrancesMargaretQuitco96% (23)

- Taxation SituationalDokument113 SeitenTaxation SituationalMartin GragasinNoch keine Bewertungen

- Assignment Part 2 - Partnership Dissolution & Liquidation - 1Dokument8 SeitenAssignment Part 2 - Partnership Dissolution & Liquidation - 1ahyenn cabelloNoch keine Bewertungen

- CPAR B94 TAX Final PB Exam - QuestionsDokument14 SeitenCPAR B94 TAX Final PB Exam - QuestionsSilver LilyNoch keine Bewertungen

- Macalintal V PETDokument3 SeitenMacalintal V PETbro_maru100% (1)

- 1.senate V Ermita Case DigestDokument6 Seiten1.senate V Ermita Case Digestryusei100% (5)

- CPAR B94 TAX Final PB Exam - Answers - SolutionsDokument12 SeitenCPAR B94 TAX Final PB Exam - Answers - SolutionsSilver LilyNoch keine Bewertungen

- Osmeña Vs Orbos 1993Dokument1 SeiteOsmeña Vs Orbos 1993lckdscl100% (1)

- G.R. No. 108763, 13 February 1997 FactsDokument2 SeitenG.R. No. 108763, 13 February 1997 FactscyhaaangelaaaNoch keine Bewertungen

- Venue Effects of Stipulations On Venue Briones vs. Court of Appeals G.R. No. 204444 January 14, 2015 FactsDokument7 SeitenVenue Effects of Stipulations On Venue Briones vs. Court of Appeals G.R. No. 204444 January 14, 2015 FactscyhaaangelaaaNoch keine Bewertungen

- Bote NotesDokument45 SeitenBote NotesSuiNoch keine Bewertungen

- Withholding Tax: Taxation LawDokument21 SeitenWithholding Tax: Taxation LawB-an JavelosaNoch keine Bewertungen

- Case Digest - Siga-An Vs VillanuevaDokument2 SeitenCase Digest - Siga-An Vs Villanuevadanica100% (1)

- 11 DBP Vs ArcillaDokument12 Seiten11 DBP Vs ArcillaPam ChuaNoch keine Bewertungen

- Auditing and Assurance Exam MidtermDokument4 SeitenAuditing and Assurance Exam MidtermMica Ella San DiegoNoch keine Bewertungen

- Auditing TheoDokument27 SeitenAuditing TheoSherri BonquinNoch keine Bewertungen

- LQ 2 AnswersDokument21 SeitenLQ 2 Answersby ScribdNoch keine Bewertungen

- Set A Leases Problem SERANADokument6 SeitenSet A Leases Problem SERANASherri BonquinNoch keine Bewertungen

- Grace Corporation Confirmation of Bank Balances DECEMBER 31, 20X1Dokument2 SeitenGrace Corporation Confirmation of Bank Balances DECEMBER 31, 20X1Joshua ComerosNoch keine Bewertungen

- Pas 1Dokument5 SeitenPas 1Simon Marquis LUMBERANoch keine Bewertungen

- Acquire To Retire Discussion DocumentDokument11 SeitenAcquire To Retire Discussion DocumentShrasti VarshneyNoch keine Bewertungen

- Business CombinationDokument3 SeitenBusiness CombinationNicoleNoch keine Bewertungen

- AFAR Quiz 4 and 5Dokument5 SeitenAFAR Quiz 4 and 5Kyla DabalmatNoch keine Bewertungen

- ZknamcxDokument68 SeitenZknamcxdominic100% (1)

- Topic 1 Corporate Liquidation - ModuleDokument11 SeitenTopic 1 Corporate Liquidation - ModuleJenny LelisNoch keine Bewertungen

- FAR Final PreboardDokument13 SeitenFAR Final PreboardMarvin ClementeNoch keine Bewertungen

- MODULE 3-Short Problems (2.0)Dokument4 SeitenMODULE 3-Short Problems (2.0)asdasdaNoch keine Bewertungen

- PNB V Rodriguez Case DigestDokument17 SeitenPNB V Rodriguez Case DigestYasha Min HNoch keine Bewertungen

- Multiple Choice - Problems Part 1: A. Percentage TaxDokument8 SeitenMultiple Choice - Problems Part 1: A. Percentage TaxWearIt Co.Noch keine Bewertungen

- Bricktown Development vs. Amor Tierra DevelopmentDokument2 SeitenBricktown Development vs. Amor Tierra DevelopmentD. RamNoch keine Bewertungen

- Chapter 8 Quiz - InventoriesDokument8 SeitenChapter 8 Quiz - InventoriesDarleen CantiladoNoch keine Bewertungen

- SCM Finals - Extra CreditDokument16 SeitenSCM Finals - Extra CreditEnola HolmesNoch keine Bewertungen

- 6 Estate Tax Lecture - CompressDokument5 Seiten6 Estate Tax Lecture - CompressbrennaNoch keine Bewertungen

- Module 2 - Control Premium PDFDokument11 SeitenModule 2 - Control Premium PDFTherese AlmiraNoch keine Bewertungen

- ACC117-CON09 Module 3 ExamDokument16 SeitenACC117-CON09 Module 3 ExamMarlon LadesmaNoch keine Bewertungen

- BADVAC1X - 1T 2122 Q2 Finals PD (Preview) Microsoft FormsDokument12 SeitenBADVAC1X - 1T 2122 Q2 Finals PD (Preview) Microsoft FormsJopnerth Carl CortezNoch keine Bewertungen

- 07audit of PPEDokument9 Seiten07audit of PPEJeanette FormenteraNoch keine Bewertungen

- Tax 2 Part 3 Estate TaxDokument25 SeitenTax 2 Part 3 Estate TaxShane TorrieNoch keine Bewertungen

- Bond Valuation Exam 1Dokument2 SeitenBond Valuation Exam 1Ronah Abigail BejocNoch keine Bewertungen

- Ejercito vs. Sandiganbayan and People of The Philippines, 509 SCRA 190Dokument12 SeitenEjercito vs. Sandiganbayan and People of The Philippines, 509 SCRA 190samantha oxfordNoch keine Bewertungen

- Accounting ReportDokument19 SeitenAccounting ReportEdward Glenn BaguiNoch keine Bewertungen

- Article 1592Dokument1 SeiteArticle 1592Bhern BhernNoch keine Bewertungen

- Sale Price of Replaced Equipment P 40,000Dokument15 SeitenSale Price of Replaced Equipment P 40,000Jay GamboaNoch keine Bewertungen

- Franchise Accounting ProblemsDokument8 SeitenFranchise Accounting ProblemsCiarwena PangcogaNoch keine Bewertungen

- First Optima Realty Corporation vs. Securitron Security Services, Inc., 748 SCRA 534, January 28, 2015Dokument20 SeitenFirst Optima Realty Corporation vs. Securitron Security Services, Inc., 748 SCRA 534, January 28, 2015Mark ReyesNoch keine Bewertungen

- Derivatives and TranslationDokument3 SeitenDerivatives and TranslationVienna Corrine Q. AbucejoNoch keine Bewertungen

- Negros Oriental State University: Brett ClydeDokument4 SeitenNegros Oriental State University: Brett ClydeCORNADO, MERIJOY G.Noch keine Bewertungen

- KEY Level 2 QuestionsDokument5 SeitenKEY Level 2 QuestionsDarelle Hannah MarquezNoch keine Bewertungen

- Quiz 1 Lump Sum Liquidation Answer Key PeresDokument7 SeitenQuiz 1 Lump Sum Liquidation Answer Key PeresChelit LadylieGirl FernandezNoch keine Bewertungen

- How Much Is The Adjusted Book Disbursements For September?: Part Ii: Practical Problems Problem No.1Dokument8 SeitenHow Much Is The Adjusted Book Disbursements For September?: Part Ii: Practical Problems Problem No.1Raenessa FranciscoNoch keine Bewertungen

- MAS - 1416 Profit Planning - CVP AnalysisDokument24 SeitenMAS - 1416 Profit Planning - CVP AnalysisAzureBlazeNoch keine Bewertungen

- Fedillaga Case13Dokument19 SeitenFedillaga Case13Luke Ysmael FedillagaNoch keine Bewertungen

- SPOUSES ANTONIO BELTRAN AND FELISA BELTRAN, Petitioners, v. SPOUSES APOLONIO CANGAYDA, JR. AND LORETA E. CANGAYDADokument6 SeitenSPOUSES ANTONIO BELTRAN AND FELISA BELTRAN, Petitioners, v. SPOUSES APOLONIO CANGAYDA, JR. AND LORETA E. CANGAYDARIZZA MAE OLANONoch keine Bewertungen

- Baliwag Polytechnic College: Financial Accounting and Reporting A. AlmineDokument6 SeitenBaliwag Polytechnic College: Financial Accounting and Reporting A. AlmineElaiza RegaladoNoch keine Bewertungen

- Requirement 1: Problem 7 (Transfer Pricing)Dokument5 SeitenRequirement 1: Problem 7 (Transfer Pricing)Jane TuazonNoch keine Bewertungen

- Quiz - Solution - PAS - 1 - and - PAS - 2.pdf Filename - UTF-8''Quiz (Solution) % PDFDokument3 SeitenQuiz - Solution - PAS - 1 - and - PAS - 2.pdf Filename - UTF-8''Quiz (Solution) % PDFSamuel BandibasNoch keine Bewertungen

- Midterm ExamDokument9 SeitenMidterm ExamElla TuratoNoch keine Bewertungen

- Questions For SMEsDokument2 SeitenQuestions For SMEsAlaine DobleNoch keine Bewertungen

- The Role of Accountants in Nation Building Through TaxationDokument2 SeitenThe Role of Accountants in Nation Building Through TaxationJoshua Ryan CanatuanNoch keine Bewertungen

- Gsis V LopezDokument6 SeitenGsis V LopezJM CaupayanNoch keine Bewertungen

- Commission On Audit:: Government Accounting Manual (Gam) Pointers CA51027Dokument4 SeitenCommission On Audit:: Government Accounting Manual (Gam) Pointers CA51027Carl Dhaniel Garcia SalenNoch keine Bewertungen

- Estate Tax Assignment 1Dokument2 SeitenEstate Tax Assignment 1Heavenly Joy CuaresmaNoch keine Bewertungen

- DBP Vs ArcillaDokument15 SeitenDBP Vs ArcillaMikhailFAbzNoch keine Bewertungen

- GR No. 161397Dokument7 SeitenGR No. 161397woahae13Noch keine Bewertungen

- FactsDokument1 SeiteFactscyhaaangelaaaNoch keine Bewertungen

- Macalintal Vs Presidential Electoral Tribunal-2Dokument47 SeitenMacalintal Vs Presidential Electoral Tribunal-2cyhaaangelaaaNoch keine Bewertungen

- Gabriel N. Trinidad and Fernando Torrillo For Appellants. Ambrosio Santos For Appellee Gatmaitan. No Appearance For The Other AppelleesDokument4 SeitenGabriel N. Trinidad and Fernando Torrillo For Appellants. Ambrosio Santos For Appellee Gatmaitan. No Appearance For The Other AppelleesMichiko HakuraNoch keine Bewertungen

- Pormento v. EstradaDokument7 SeitenPormento v. EstradacyhaaangelaaaNoch keine Bewertungen

- Morigo y Cacho Vs People 422 SCRA 376Dokument7 SeitenMorigo y Cacho Vs People 422 SCRA 376Myco MemoNoch keine Bewertungen

- Republic of The Philippines VDokument3 SeitenRepublic of The Philippines VcyhaaangelaaaNoch keine Bewertungen

- FactsmDokument1 SeiteFactsmcyhaaangelaaaNoch keine Bewertungen

- Pimentel V. Joint Committee of Congress G.R. No. 163783, June 22, 2004 en Banc HeldDokument2 SeitenPimentel V. Joint Committee of Congress G.R. No. 163783, June 22, 2004 en Banc HeldcyhaaangelaaaNoch keine Bewertungen

- Immunity From SuitDokument7 SeitenImmunity From SuitcyhaaangelaaaNoch keine Bewertungen

- Rubrico v. Arroyo PDFDokument1 SeiteRubrico v. Arroyo PDFNeil ChuaNoch keine Bewertungen

- Chi Ming Tsoi v. CADokument7 SeitenChi Ming Tsoi v. CACessy Ciar KimNoch keine Bewertungen

- Marcos VS. Manglapus, Respondent (Part 1)Dokument4 SeitenMarcos VS. Manglapus, Respondent (Part 1)cyhaaangelaaaNoch keine Bewertungen

- MarcosDokument3 SeitenMarcoscyhaaangelaaaNoch keine Bewertungen

- CIR v. SantosDokument7 SeitenCIR v. SantoscyhaaangelaaaNoch keine Bewertungen

- FactsDokument1 SeiteFactscyhaaangelaaaNoch keine Bewertungen

- IssueDokument1 SeiteIssuecyhaaangelaaaNoch keine Bewertungen

- Morisino v. Morisino PDFDokument5 SeitenMorisino v. Morisino PDFcyhaaangelaaaNoch keine Bewertungen

- CseDokument2 SeitenCsecyhaaangelaaaNoch keine Bewertungen

- Neri Vs Senate Committee Class DigestDokument1 SeiteNeri Vs Senate Committee Class DigestcyhaaangelaaaNoch keine Bewertungen

- Tolentino v. Secretary of Finance - 249 SCRA 635Dokument2 SeitenTolentino v. Secretary of Finance - 249 SCRA 635cyhaaangelaaaNoch keine Bewertungen

- Bengzon V Senate Blue Ribbon Committee Digest G.R. No. 89914 November 20, 1991 Padilla, J.Dokument4 SeitenBengzon V Senate Blue Ribbon Committee Digest G.R. No. 89914 November 20, 1991 Padilla, J.cyhaaangelaaaNoch keine Bewertungen

- Royal Plains View Inc Vs Mejia PDFDokument19 SeitenRoyal Plains View Inc Vs Mejia PDFcyhaaangelaaaNoch keine Bewertungen

- Prospectus of First Security BankDokument123 SeitenProspectus of First Security BankKhalid FirozNoch keine Bewertungen

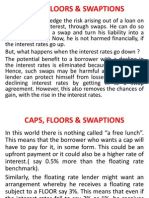

- Five-Caps, Floors & Swaptions 8Dokument8 SeitenFive-Caps, Floors & Swaptions 8Akhilesh SinghNoch keine Bewertungen

- Banco Espanol vs. Palanca, 37 Phil. 921Dokument17 SeitenBanco Espanol vs. Palanca, 37 Phil. 921thelawyer07100% (1)

- BIFRDokument3 SeitenBIFRkanchan_khadilkarNoch keine Bewertungen

- Power Finance CorporationDokument32 SeitenPower Finance Corporationangshu0020100% (2)

- Pretest (Clean)Dokument3 SeitenPretest (Clean)CharlesNoch keine Bewertungen

- OILBANK SecCert BOD Reso-Confirming T&CSDokument2 SeitenOILBANK SecCert BOD Reso-Confirming T&CSChristjohn VillaluzNoch keine Bewertungen

- CK 114Dokument21 SeitenCK 114varun v sNoch keine Bewertungen

- Banks and Customers Relation (1) - 2Dokument36 SeitenBanks and Customers Relation (1) - 2harshitha harshiNoch keine Bewertungen

- NABARDDokument19 SeitenNABARDNiravThakkarNoch keine Bewertungen

- Corporate Laws and Practices-Part 2Dokument2 SeitenCorporate Laws and Practices-Part 2gundapolaNoch keine Bewertungen

- Jurisdiction Anama vs. CitibankDokument4 SeitenJurisdiction Anama vs. CitibankMia de la FuenteNoch keine Bewertungen

- Breakeven ExerciseDokument8 SeitenBreakeven Exerciseapi-279578984Noch keine Bewertungen

- Concept of NPADokument40 SeitenConcept of NPAsonu_1986100% (2)

- Ching Handout 1Dokument27 SeitenChing Handout 1Christian Clyde Zacal ChingNoch keine Bewertungen

- Case Digest GuarantyDokument23 SeitenCase Digest GuarantyRachel AndreleeNoch keine Bewertungen

- Interest Rates: Options, Futures, and Other Derivatives 8th Edition, 1Dokument40 SeitenInterest Rates: Options, Futures, and Other Derivatives 8th Edition, 1Rahul KhandelwalNoch keine Bewertungen

- SPI-Property VALUATION UPDATE-VB Real Estate Services GmbH-Timisoara-74687m - 191112-FINA L PDFDokument39 SeitenSPI-Property VALUATION UPDATE-VB Real Estate Services GmbH-Timisoara-74687m - 191112-FINA L PDFPopescu GeorgeNoch keine Bewertungen