Das könnte Ihnen auch gefallen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Course Business LawDokument8 SeitenCourse Business LawghsjgjNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Childhood Gender Nonconformity and Children's Past-Life MemoriesDokument10 SeitenChildhood Gender Nonconformity and Children's Past-Life MemoriesghsjgjNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Chapter 1663Dokument26 SeitenChapter 1663ghsjgjNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Course Structure - NMIMS Navi Mumbai Campus BBA (2017 - 2020)Dokument2 SeitenCourse Structure - NMIMS Navi Mumbai Campus BBA (2017 - 2020)ghsjgjNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Sybba FDokument1 SeiteSybba FghsjgjNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Chapter 4 Retirement or Death of A PartnerDokument2 SeitenChapter 4 Retirement or Death of A PartnerghsjgjNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Oyster Mushrooms Humidity Control Based On Fuzzy Logic by Using Arduino Atmega238 MicrocontrollerDokument13 SeitenOyster Mushrooms Humidity Control Based On Fuzzy Logic by Using Arduino Atmega238 MicrocontrollerghsjgjNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- (I) Purpose (Ii) Scope: Maharashtra Debate Open 2020 Equity PolicyDokument11 Seiten(I) Purpose (Ii) Scope: Maharashtra Debate Open 2020 Equity PolicyghsjgjNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- BBA Course Structure 2020 - 23Dokument1 SeiteBBA Course Structure 2020 - 23ghsjgjNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Scanned With CamscannerDokument5 SeitenScanned With CamscannerghsjgjNoch keine Bewertungen

- FlipMoran - Origami Flowers - Book One (2004) - Michael LafosseDokument18 SeitenFlipMoran - Origami Flowers - Book One (2004) - Michael LafosseghsjgjNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Lunacy and Idiocy - The Old Law and Its IncubusDokument8 SeitenLunacy and Idiocy - The Old Law and Its IncubusghsjgjNoch keine Bewertungen

- Case Study Journey Into Self AwarenessDokument1 SeiteCase Study Journey Into Self Awarenessghsjgj100% (1)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Principles of Management ProjectDokument23 SeitenPrinciples of Management ProjectghsjgjNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Welcome - Freebie (Absurd - Design)Dokument6 SeitenWelcome - Freebie (Absurd - Design)ghsjgjNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Fffi:-Ffid Ffirffi F T T: FfitqtDokument4 SeitenFffi:-Ffid Ffirffi F T T: FfitqtghsjgjNoch keine Bewertungen

- Barriers To Effective ListeningDokument2 SeitenBarriers To Effective ListeningghsjgjNoch keine Bewertungen

- Align Yourself With The CompanyDokument2 SeitenAlign Yourself With The CompanyghsjgjNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Spirale PDFDokument1 SeiteSpirale PDFghsjgjNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Egistration: Learning OutcomesDokument56 SeitenEgistration: Learning OutcomesghsjgjNoch keine Bewertungen

- Guide To Tanzania Taxation SystemDokument3 SeitenGuide To Tanzania Taxation Systemhima100% (1)

- Quiz - Inventories Cut-Off Test 2Dokument1 SeiteQuiz - Inventories Cut-Off Test 2Ana Mae HernandezNoch keine Bewertungen

- Unitrans - Training Services - 08 Jul 2021Dokument4 SeitenUnitrans - Training Services - 08 Jul 2021Telvin BanzeNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Debit and Credit (Example)Dokument4 SeitenDebit and Credit (Example)Marjorie PeriferioNoch keine Bewertungen

- College Dues (July-Aug-SEP 2021) College Dues (July-Aug - SEP 2021) College Dues (July-Aug - SEP 2021)Dokument1 SeiteCollege Dues (July-Aug-SEP 2021) College Dues (July-Aug - SEP 2021) College Dues (July-Aug - SEP 2021)Shona ButtNoch keine Bewertungen

- Description From Currency To Currency Recipient Receive Exchange Rate Amount DueDokument1 SeiteDescription From Currency To Currency Recipient Receive Exchange Rate Amount DueJOMBANG TIMOERNoch keine Bewertungen

- Chapter 1 Audit of Cash and Cash EquivalentsDokument127 SeitenChapter 1 Audit of Cash and Cash EquivalentsAgatha de Castro81% (21)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- PDFDokument4 SeitenPDFAce MereriaNoch keine Bewertungen

- Accounting For Local Government Unit I. Basic Fatures and PoliciesDokument10 SeitenAccounting For Local Government Unit I. Basic Fatures and PoliciesChin-Chin Alvarez SabinianoNoch keine Bewertungen

- Growth of The Use of Plastic Money in IndiaDokument46 SeitenGrowth of The Use of Plastic Money in IndiaHarshitGupta81% (21)

- 2019 lm300 3 0 1 1713072Dokument4 Seiten2019 lm300 3 0 1 1713072Irshaad Ally Ashrafi GolapkhanNoch keine Bewertungen

- Metro de Madrid PresentationDokument39 SeitenMetro de Madrid PresentationMarton CavaniNoch keine Bewertungen

- Nordea BankDokument6 SeitenNordea Bankeureka.net24Noch keine Bewertungen

- Comenzi Tarife Amadeus ....Dokument12 SeitenComenzi Tarife Amadeus ....liudka_lionessNoch keine Bewertungen

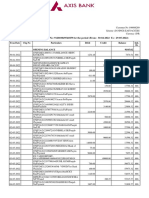

- Statement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Dokument5 SeitenStatement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Rahul BansalNoch keine Bewertungen

- Mi BillDokument1 SeiteMi BillJagannath MandalNoch keine Bewertungen

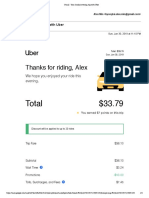

- Gmail - Your Sunday Evening Trip With Uber PDFDokument4 SeitenGmail - Your Sunday Evening Trip With Uber PDFAnonymous 0Rc3aqQNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 1575517183688JlPSe5QaAila2orp PDFDokument15 Seiten1575517183688JlPSe5QaAila2orp PDFPr Satish BethaNoch keine Bewertungen

- Act BillDokument2 SeitenAct BillSujith Reddy ThummalaNoch keine Bewertungen

- BillDokument1 SeiteBillFahadImranXhiekhNoch keine Bewertungen

- August 2020 DA-PA Updated Sites - Guest Posting SitesDokument12 SeitenAugust 2020 DA-PA Updated Sites - Guest Posting SitesРоман ГудименкоNoch keine Bewertungen

- 85th SLC MinutesDokument201 Seiten85th SLC MinutesSHANMUKHA INDUSTRIESNoch keine Bewertungen

- L3 Road TransportDokument62 SeitenL3 Road TransportCarmenn LouNoch keine Bewertungen

- Accounting For Non-Profit Organization: Presenting by Mohammed Nasih B.MDokument8 SeitenAccounting For Non-Profit Organization: Presenting by Mohammed Nasih B.MChandreshNoch keine Bewertungen

- Phung Van Cung: Spend Account StatementDokument2 SeitenPhung Van Cung: Spend Account StatementhienvvuNoch keine Bewertungen

- BL Miel PDFDokument4 SeitenBL Miel PDFWilmer DuarteNoch keine Bewertungen

- Materi Logistik ManagementDokument73 SeitenMateri Logistik ManagementsaridewiaNoch keine Bewertungen

- Forex Service Charges: Exports Bills Purchased /Discounted/NegotiatedDokument9 SeitenForex Service Charges: Exports Bills Purchased /Discounted/NegotiatedSameer GhogaleNoch keine Bewertungen

- Gst-Challan RCMDokument2 SeitenGst-Challan RCMCA Satish MotupalliNoch keine Bewertungen

- Mrunal Banking - Bharat Bill Payment System (BBPS) ExplainedDokument10 SeitenMrunal Banking - Bharat Bill Payment System (BBPS) ExplainedRahul KumarNoch keine Bewertungen

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsVon EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNoch keine Bewertungen

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantVon EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantBewertung: 4 von 5 Sternen4/5 (104)

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessVon EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessBewertung: 4.5 von 5 Sternen4.5/5 (4)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassVon EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNoch keine Bewertungen