Das könnte Ihnen auch gefallen

- Computer Script1Dokument29 SeitenComputer Script1AbhinawNoch keine Bewertungen

- Introduction To Computer & Emerging TechnologiesDokument30 SeitenIntroduction To Computer & Emerging TechnologiesAmv MasterNoch keine Bewertungen

- Class 11th Computer Notes Ch1Dokument30 SeitenClass 11th Computer Notes Ch1ashutoshdwivedi968Noch keine Bewertungen

- Computarised Accounting BestDokument59 SeitenComputarised Accounting Bestwambualucas74Noch keine Bewertungen

- PC Package Unit 1 Introduction To ComputerDokument28 SeitenPC Package Unit 1 Introduction To ComputerrameshNoch keine Bewertungen

- How Computers Process Data to Derive Useful InformationDokument7 SeitenHow Computers Process Data to Derive Useful InformationMohd asimNoch keine Bewertungen

- Introduction to Computers and Their ApplicationsDokument13 SeitenIntroduction to Computers and Their ApplicationsuppaliNoch keine Bewertungen

- LN 1Dokument7 SeitenLN 1matarabdullah61Noch keine Bewertungen

- FOAC Unit-1Dokument16 SeitenFOAC Unit-1krishnapandey77733Noch keine Bewertungen

- Pptpresentationoncomputerfundamemntal 170831052423Dokument111 SeitenPptpresentationoncomputerfundamemntal 170831052423yaswanthNoch keine Bewertungen

- IT Application in BusinessDokument24 SeitenIT Application in Businesskodnya.meenuNoch keine Bewertungen

- Bcastudyguide Com Computer Fundamental Office Automation CfoaDokument10 SeitenBcastudyguide Com Computer Fundamental Office Automation Cfoadharmista p DumasiyaNoch keine Bewertungen

- Css 111 Lect - 1Dokument85 SeitenCss 111 Lect - 1Darren MgayaNoch keine Bewertungen

- Chapter - 2Dokument28 SeitenChapter - 2oplizoixnNoch keine Bewertungen

- Computer FundamentalDokument63 SeitenComputer Fundamentalpriyanka groverNoch keine Bewertungen

- Computer and Computerised Accounting System: ObjectivesDokument27 SeitenComputer and Computerised Accounting System: ObjectivesASILAZA FELIXNoch keine Bewertungen

- Computer - ApplicationsDokument61 SeitenComputer - ApplicationsJoji Ann UayanNoch keine Bewertungen

- Chapter - 1 - BaisDokument27 SeitenChapter - 1 - BaisNahom MelakuNoch keine Bewertungen

- Accountancy Notes Computer in AccountingDokument3 SeitenAccountancy Notes Computer in AccountingYashKhanijo100% (1)

- Introduction to Computer HardwareDokument27 SeitenIntroduction to Computer HardwareBiniyam DameneNoch keine Bewertungen

- Computer AssignmentDokument7 SeitenComputer Assignmentaroosh16Noch keine Bewertungen

- CIS FinalDokument103 SeitenCIS FinalAayush ShresthaNoch keine Bewertungen

- Comp. Hardware 1stDokument7 SeitenComp. Hardware 1stpriyanka groverNoch keine Bewertungen

- Itm 1Dokument24 SeitenItm 1chavsNoch keine Bewertungen

- Computer: Fundamentals of Computer and IT (BCAC0002) (MODULE-1)Dokument32 SeitenComputer: Fundamentals of Computer and IT (BCAC0002) (MODULE-1)Naman MalikNoch keine Bewertungen

- Living in The IT EraDokument12 SeitenLiving in The IT EraLilian May MalfartaNoch keine Bewertungen

- Fundamental Ch1Dokument12 SeitenFundamental Ch1SubhashreeswainNoch keine Bewertungen

- Learn Computer Fundamentals & Its ApplicationsDokument13 SeitenLearn Computer Fundamentals & Its ApplicationshotniliNoch keine Bewertungen

- M02-Connect Hardware PeripheralsDokument38 SeitenM02-Connect Hardware PeripheralsSolomon SBNoch keine Bewertungen

- Unit 1&2 - DCFDokument38 SeitenUnit 1&2 - DCF22itu218Noch keine Bewertungen

- KMB 108 Unit I: Computer Application & Management Information and SystemDokument15 SeitenKMB 108 Unit I: Computer Application & Management Information and SystemDeepankar singhNoch keine Bewertungen

- AGR315 (Repaired)Dokument36 SeitenAGR315 (Repaired)musaabdullaziz781Noch keine Bewertungen

- The Evolution of ComputersDokument12 SeitenThe Evolution of ComputersLakshmi SarvaniNoch keine Bewertungen

- Unit - 5 Computer and Computerised Accounting SystemDokument7 SeitenUnit - 5 Computer and Computerised Accounting SystemRobin SinghNoch keine Bewertungen

- UNIT Ichapter1 (Introduction To Computer)Dokument12 SeitenUNIT Ichapter1 (Introduction To Computer)Vinutha SanthoshNoch keine Bewertungen

- Computer Project SEM2 MBADokument42 SeitenComputer Project SEM2 MBAPriya PathariyaNoch keine Bewertungen

- Computer Concepts and C Programming ExplainedDokument70 SeitenComputer Concepts and C Programming ExplainedChinmayac CnNoch keine Bewertungen

- computer_introduction Unit1Dokument7 Seitencomputer_introduction Unit1mailtoprateekk30Noch keine Bewertungen

- Computer FundamentalDokument75 SeitenComputer Fundamentalapi-213911742Noch keine Bewertungen

- Basics of Computers - Quick Guide - TutorialspointDokument50 SeitenBasics of Computers - Quick Guide - TutorialspointJames MukhwanaNoch keine Bewertungen

- CPT211 Module 1Dokument31 SeitenCPT211 Module 1maxene jadeNoch keine Bewertungen

- IT Applications in Business UNIT I NOTESDokument50 SeitenIT Applications in Business UNIT I NOTESTanmay AgrawalNoch keine Bewertungen

- Chapter 1 Computer Fundamentals (XI)Dokument127 SeitenChapter 1 Computer Fundamentals (XI)Yohannes Busho100% (1)

- Basics of Computers - Quick GuideDokument47 SeitenBasics of Computers - Quick GuideChinmoyee BiswasNoch keine Bewertungen

- Basics of Computers - IntroDokument14 SeitenBasics of Computers - IntrosaraNoch keine Bewertungen

- Computer Quick Guide - HTMDokument10 SeitenComputer Quick Guide - HTMPrashant Khade100% (1)

- Basic ComDokument134 SeitenBasic ComRosli MohdNoch keine Bewertungen

- Booting Your Computer: A Guide to the Startup Process /TITLEDokument45 SeitenBooting Your Computer: A Guide to the Startup Process /TITLEJaren QueganNoch keine Bewertungen

- Part - 1-General IntroductionDokument19 SeitenPart - 1-General IntroductionhunexNoch keine Bewertungen

- Computer Fundamentals TutorialDokument93 SeitenComputer Fundamentals TutorialJoy MaryNoch keine Bewertungen

- Intro To Info TechDokument33 SeitenIntro To Info TechGrezel NiceNoch keine Bewertungen

- Basics of Computer and Its OperationsDokument11 SeitenBasics of Computer and Its OperationsKingashiqhussainPanhwerNoch keine Bewertungen

- Introduction to Computers: Input-Output, Hardware, Software & ApplicationsDokument23 SeitenIntroduction to Computers: Input-Output, Hardware, Software & ApplicationsDevid LuizNoch keine Bewertungen

- Computer Application Syllabus BreakdownDokument0 SeitenComputer Application Syllabus BreakdownHareesh YadavNoch keine Bewertungen

- Introduction To Computer Fundamental: April 2013Dokument200 SeitenIntroduction To Computer Fundamental: April 2013Beverly TaniongonNoch keine Bewertungen

- Computer FundamentalsDokument66 SeitenComputer FundamentalsAlieu BanguraNoch keine Bewertungen

- Understanding Computers, Smartphones and the InternetVon EverandUnderstanding Computers, Smartphones and the InternetBewertung: 5 von 5 Sternen5/5 (1)

- Accounting Treatment of Forfeiture of SharesDokument18 SeitenAccounting Treatment of Forfeiture of SharesMandy SinghNoch keine Bewertungen

- Reissue of Forfeited Shares AccountingDokument13 SeitenReissue of Forfeited Shares AccountingsandeepchintalpalliNoch keine Bewertungen

- Issue of SharesDokument26 SeitenIssue of SharesAmandeep Singh MankuNoch keine Bewertungen

- 320EL17Dokument21 Seiten320EL17hajihalvi100% (1)

- Admission of Partner Accounting TreatmentDokument40 SeitenAdmission of Partner Accounting TreatmentNitesh Matta100% (3)

- Company IntroDokument14 SeitenCompany IntroMehera SameeraNoch keine Bewertungen

- Retirement and Death of A PartnerDokument36 SeitenRetirement and Death of A PartnerArunima JainNoch keine Bewertungen

- Partnership Accounting for Profits, Losses and CapitalDokument25 SeitenPartnership Accounting for Profits, Losses and CapitalMuhammad Farid AsgharNoch keine Bewertungen

- Trial Balance Errors & Rectification 1Dokument21 SeitenTrial Balance Errors & Rectification 1Manju NathNoch keine Bewertungen

- 14 - Financial Statement - I (175 KB) PDFDokument21 Seiten14 - Financial Statement - I (175 KB) PDFramneekdadwalNoch keine Bewertungen

- Accounting Adjustments in Financial StatementsDokument26 SeitenAccounting Adjustments in Financial Statementsshaannivas100% (1)

- Trial BalanceDokument21 SeitenTrial BalanceRiza JauferNoch keine Bewertungen

- 320EL13Dokument26 Seiten320EL13Amit Kumar RaiNoch keine Bewertungen

- 16 - Not For Profit Organisation - An Introduction (134 KB) PDFDokument14 Seiten16 - Not For Profit Organisation - An Introduction (134 KB) PDFramneekdadwalNoch keine Bewertungen

- BRS Bank Reconcilation StatementDokument15 SeitenBRS Bank Reconcilation Statementbabluon22Noch keine Bewertungen

- 8) Special Purpose BooksDokument21 Seiten8) Special Purpose BooksRay ChNoch keine Bewertungen

- ModuleDokument26 SeitenModuleSantosh KumarNoch keine Bewertungen

- 1 - Accounting - An Introduction (167 KB)Dokument16 Seiten1 - Accounting - An Introduction (167 KB)Rajah ParanthamanNoch keine Bewertungen

- 320EL6Dokument19 Seiten320EL6Sachin RajguruNoch keine Bewertungen

- Cash BookDokument26 SeitenCash Booksagiinfo1100% (1)

- Plot Plan and Equipment LayoutDokument23 SeitenPlot Plan and Equipment Layoutravirawat15Noch keine Bewertungen

- Accounting ExampleDokument30 SeitenAccounting Exampleaqeelkhan7942Noch keine Bewertungen

- GAAP StandardsDokument13 SeitenGAAP StandardsAnkita MahajanNoch keine Bewertungen

- 5) JournalDokument24 Seiten5) JournalRay ChNoch keine Bewertungen

- CyberLock CatalogDokument16 SeitenCyberLock CatalogSarwat Naim SiddiquiNoch keine Bewertungen

- Ise Vi Software TestingDokument228 SeitenIse Vi Software Testingdavid satyaNoch keine Bewertungen

- Key Management ChecklistDokument5 SeitenKey Management ChecklistrajainfosysNoch keine Bewertungen

- English For IT StudentsDokument527 SeitenEnglish For IT StudentsGadkiy PonchikNoch keine Bewertungen

- VSDC Lac Test Keys v4 - 9Dokument2 SeitenVSDC Lac Test Keys v4 - 9c0ugar100% (2)

- Assignment Chapter 9Dokument3 SeitenAssignment Chapter 9Nur ArinahNoch keine Bewertungen

- PNB-1068 (R1) - Application Form For ATM DEBIT CardsDokument2 SeitenPNB-1068 (R1) - Application Form For ATM DEBIT CardsChandan GuptaNoch keine Bewertungen

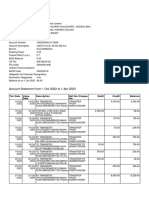

- Account Statement From 3 Jun 2020 To 3 Dec 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument4 SeitenAccount Statement From 3 Jun 2020 To 3 Dec 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePoonam UpadhyayNoch keine Bewertungen

- Koida GuideDokument23 SeitenKoida GuideRom PerezNoch keine Bewertungen

- Eyesweb Xmi 5.3.0 - User Manual: January 16, 2012Dokument1.333 SeitenEyesweb Xmi 5.3.0 - User Manual: January 16, 2012colettapNoch keine Bewertungen

- Welcome-KitDokument19 SeitenWelcome-Kitmohammad qadafiNoch keine Bewertungen

- Bank statement summary for Mr. Aman Kumar JaiswalDokument10 SeitenBank statement summary for Mr. Aman Kumar JaiswalAman JaiswalNoch keine Bewertungen

- SIM Swap ?updated 2Dokument6 SeitenSIM Swap ?updated 2gangNoch keine Bewertungen

- Pen Drive As An AtmDokument27 SeitenPen Drive As An AtmRahul Gupta33% (3)

- State Charts For Example ATM SystemDokument4 SeitenState Charts For Example ATM SystemMuhammad Yaqub Mohsin BhattiNoch keine Bewertungen

- Unemployment Insurance A Claimant HandbookDokument84 SeitenUnemployment Insurance A Claimant HandbookFloydNoch keine Bewertungen

- FEENICIA Response Codes 3.0Dokument13 SeitenFEENICIA Response Codes 3.0chipolitohNoch keine Bewertungen

- Account Statement From 1 Apr 2023 To 31 Oct 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument3 SeitenAccount Statement From 1 Apr 2023 To 31 Oct 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceBhavik NasitNoch keine Bewertungen

- ATM Response CodesDokument5 SeitenATM Response CodesSenthil KarthiNoch keine Bewertungen

- Credit Card StatementDokument4 SeitenCredit Card StatementSheikh ShoaibNoch keine Bewertungen

- Aci6007 Mount enDokument9 SeitenAci6007 Mount encacatmareNoch keine Bewertungen

- Test 3Dokument25 SeitenTest 3Alex PpnNoch keine Bewertungen

- Pay ShieldDokument2 SeitenPay ShieldsdadsdNoch keine Bewertungen

- Basic Computer SecurityDokument20 SeitenBasic Computer SecuritySachin ShawNoch keine Bewertungen

- Bank ManagementDokument198 SeitenBank ManagementSooraj Kallooppara0% (1)

- Sop GCC RevisedDokument16 SeitenSop GCC RevisedChandan SinghNoch keine Bewertungen

- Carding Info 2Dokument4 SeitenCarding Info 2djNoch keine Bewertungen

- Srs - ATM SampleDokument17 SeitenSrs - ATM SampleVahosNoch keine Bewertungen

- Bank of Maharashtra Branch MICR No. Serial Number Atm Card Application FormDokument2 SeitenBank of Maharashtra Branch MICR No. Serial Number Atm Card Application FormMohit RajputNoch keine Bewertungen

- BS en 726-3Dokument88 SeitenBS en 726-3engr_usman04Noch keine Bewertungen