Das könnte Ihnen auch gefallen

- Nanotech PresentationDokument11 SeitenNanotech Presentationapi-349157720Noch keine Bewertungen

- E Portfolio Post Reflective Worksheet Phil 1000Dokument3 SeitenE Portfolio Post Reflective Worksheet Phil 1000api-349157720Noch keine Bewertungen

- Paper 2 - 5wsofexist Phil 1000Dokument6 SeitenPaper 2 - 5wsofexist Phil 1000api-349157720Noch keine Bewertungen

- Paper 1 - Socrates Phil 1000Dokument6 SeitenPaper 1 - Socrates Phil 1000api-349157720Noch keine Bewertungen

- Group Theory Presentation - ShrekDokument14 SeitenGroup Theory Presentation - Shrekapi-349157720100% (1)

- CJ 1010 - Week 14 Homework Post-Assessment QuestionaireDokument3 SeitenCJ 1010 - Week 14 Homework Post-Assessment Questionaireapi-349157720Noch keine Bewertungen

- Group Theory Research Paper - ShrekDokument4 SeitenGroup Theory Research Paper - Shrekapi-349157720Noch keine Bewertungen

- Nanotechnology PaperDokument6 SeitenNanotechnology Paperapi-349157720Noch keine Bewertungen

- Personal Experience PaperDokument3 SeitenPersonal Experience Paperapi-349157720Noch keine Bewertungen

- Case Study Analysis - SweatshopsDokument6 SeitenCase Study Analysis - Sweatshopsapi-349157720Noch keine Bewertungen

- Semester Project - SirensDokument6 SeitenSemester Project - Sirensapi-349157720Noch keine Bewertungen

- Walker WarsDokument2 SeitenWalker Warsapi-349157720Noch keine Bewertungen

- Assignment 4 - Interest Group Essay CorrectedDokument5 SeitenAssignment 4 - Interest Group Essay Correctedapi-349157720Noch keine Bewertungen

- Essay On The Short StoryDokument4 SeitenEssay On The Short Storyapi-349157720Noch keine Bewertungen

- 250-One Word-Themed StoryDokument2 Seiten250-One Word-Themed Storyapi-349157720Noch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Series B - Paper 2 QPDokument12 SeitenSeries B - Paper 2 QPPatience MhakaNoch keine Bewertungen

- UzAuto Motors IFRS Report FY2022Dokument41 SeitenUzAuto Motors IFRS Report FY2022id00001875Noch keine Bewertungen

- An Over View Regarding AISDokument15 SeitenAn Over View Regarding AISDonia MohamedNoch keine Bewertungen

- Numerical Test 5 SolutionsDokument16 SeitenNumerical Test 5 Solutionslawrence ojuaNoch keine Bewertungen

- Hard Hat Q4 2015Dokument11 SeitenHard Hat Q4 2015ronNoch keine Bewertungen

- Value Chain Analysisof AmazonDokument4 SeitenValue Chain Analysisof Amazonjillchanura220Noch keine Bewertungen

- World Policy Journal: Bangladesh: A Labor ParadoxDokument11 SeitenWorld Policy Journal: Bangladesh: A Labor ParadoxPranto BaraiNoch keine Bewertungen

- Account Statement For The Account: 1926010003332: Branch DetailsDokument7 SeitenAccount Statement For The Account: 1926010003332: Branch DetailsOp MassNoch keine Bewertungen

- Social Media ReportDokument47 SeitenSocial Media ReportStella LeilaNoch keine Bewertungen

- Baseline Function List en CLDokument16 SeitenBaseline Function List en CLIván Andrés Marchant NúñezNoch keine Bewertungen

- HBL 295 - Fact 776Dokument1 SeiteHBL 295 - Fact 776ORLANDO GONZALEZNoch keine Bewertungen

- TikTok Shop PitchDokument30 SeitenTikTok Shop PitchAlmirzaqyNoch keine Bewertungen

- Blockchain and The Law The Rule of Code - Primavera - & - WrightDokument311 SeitenBlockchain and The Law The Rule of Code - Primavera - & - Wrightf_stones100% (1)

- 110606-9 KA26 GT26 Technology Update Vietnam - HandoutDokument68 Seiten110606-9 KA26 GT26 Technology Update Vietnam - Handouttrungnq_ktd97Noch keine Bewertungen

- Applied EconomicsDokument8 SeitenApplied EconomicsReynald AntasoNoch keine Bewertungen

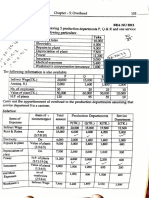

- Overheard Accounting MathDokument18 SeitenOverheard Accounting Mathfaraaz360Noch keine Bewertungen

- Fashion Business PlanDokument12 SeitenFashion Business PlanMAVERICK MONROE100% (1)

- Essential IT controls for risk managementDokument196 SeitenEssential IT controls for risk managementvishal jalanNoch keine Bewertungen

- High-Performance Human Resource Practices, Citizenship Behavior, and Organizational Performance - A Relational Perspective, Sun, Aryee, Law (2007)Dokument21 SeitenHigh-Performance Human Resource Practices, Citizenship Behavior, and Organizational Performance - A Relational Perspective, Sun, Aryee, Law (2007)Suryanarayan IyerNoch keine Bewertungen

- A3 2014 - Compliance Dept.: Focus: Labor Plan 2014Dokument12 SeitenA3 2014 - Compliance Dept.: Focus: Labor Plan 2014Yan RDNoch keine Bewertungen

- Oil & Gas Industry Glossary Training GuideDokument35 SeitenOil & Gas Industry Glossary Training GuidePriya ElangoNoch keine Bewertungen

- The 2021 Global Crypto Adoption Report: Vietnam Tops Index as P2P Platforms Drive Usage GrowthDokument133 SeitenThe 2021 Global Crypto Adoption Report: Vietnam Tops Index as P2P Platforms Drive Usage GrowthBucur Constanța - LiviaNoch keine Bewertungen

- VSA NotesDokument15 SeitenVSA Notesjunaid100% (1)

- Term-4 End Term Question PapersDokument93 SeitenTerm-4 End Term Question PapersParas KhuranaNoch keine Bewertungen

- Project Appraisal (Transport For APCOMS)Dokument7 SeitenProject Appraisal (Transport For APCOMS)yusrazzzNoch keine Bewertungen

- Question PapersDokument2 SeitenQuestion PapersPrachi PatilNoch keine Bewertungen

- GlossaryDokument3 SeitenGlossaryYug KhatanaNoch keine Bewertungen

- The First ICO With 200 Million Active SersDokument1 SeiteThe First ICO With 200 Million Active SersSunny DineshNoch keine Bewertungen

- IIM VISAKHAPATNAM CORPORATE FINANCE END-TERM EXAMDokument11 SeitenIIM VISAKHAPATNAM CORPORATE FINANCE END-TERM EXAMAyush FuseNoch keine Bewertungen

- Application Form M3M IFCDokument38 SeitenApplication Form M3M IFCDashmesh LandbaseNoch keine Bewertungen