Das könnte Ihnen auch gefallen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Lembar JawabanDokument28 SeitenLembar Jawabansusi mamaNoch keine Bewertungen

- Engagement & Quality Control Standards: CA Sarthak JainDokument48 SeitenEngagement & Quality Control Standards: CA Sarthak Jainzayn mallikNoch keine Bewertungen

- HDFC Focused 30 Fund PresentationDokument18 SeitenHDFC Focused 30 Fund PresentationYuvaNoch keine Bewertungen

- Credit Cards: Statement of AccountDokument4 SeitenCredit Cards: Statement of AccountLuis AngNoch keine Bewertungen

- A I T CLO E: February 2020Dokument54 SeitenA I T CLO E: February 2020Kunal Goel100% (1)

- Unit 5: Death of A PartnerDokument23 SeitenUnit 5: Death of A PartnerKARTIK CHADHANoch keine Bewertungen

- Correspondent BanksDokument4 SeitenCorrespondent BankscharrisedelarosaNoch keine Bewertungen

- Loan RatesDokument1 SeiteLoan RatesAndrew ChambersNoch keine Bewertungen

- A083 Chapter 9 Group 1Dokument8 SeitenA083 Chapter 9 Group 1MENESES, Trixie Ann TrapaNoch keine Bewertungen

- TEv B03 Hy OSHzi 3 RuDokument3 SeitenTEv B03 Hy OSHzi 3 RuAakash JamwalNoch keine Bewertungen

- Powerscreen InvoiceDokument1 SeitePowerscreen InvoiceJuan Felipe GómezNoch keine Bewertungen

- Conceptual Framework and Accounting Standards Quiz Reviewer PDFDokument26 SeitenConceptual Framework and Accounting Standards Quiz Reviewer PDFZeo AlcantaraNoch keine Bewertungen

- Lecture 2.1Dokument50 SeitenLecture 2.1Tuong Vi Nguyen PhanNoch keine Bewertungen

- Analyzing Transactions To Start A BusinessDokument22 SeitenAnalyzing Transactions To Start A BusinessPaula MabulukNoch keine Bewertungen

- التمويل بعقد المشاركة في المصارف الإسلاميةDokument20 Seitenالتمويل بعقد المشاركة في المصارف الإسلاميةNEXTWAY TECHNOLOGIENoch keine Bewertungen

- Quizzers 12Dokument13 SeitenQuizzers 12Niña Yna Franchesca PantallaNoch keine Bewertungen

- Test Bank For Fundamental Financial Accounting Concepts 8th Edition EdmondsDokument24 SeitenTest Bank For Fundamental Financial Accounting Concepts 8th Edition EdmondsHarryWilliamscwjbo100% (34)

- Charges & Fee - IDBI Bank Card Products: 1) Classic Debit Card/Women's Debit Card/Being Me Card/Kids CardDokument5 SeitenCharges & Fee - IDBI Bank Card Products: 1) Classic Debit Card/Women's Debit Card/Being Me Card/Kids Cardrose thomsan thomsanNoch keine Bewertungen

- Đề 2022 2023Dokument11 SeitenĐề 2022 2023buitrantuuyen2003Noch keine Bewertungen

- CHP 11Dokument41 SeitenCHP 11SUBA NANTINI A/P M.SUBRAMANIAMNoch keine Bewertungen

- Engineering Economics: InterestDokument3 SeitenEngineering Economics: InterestJm TangoNoch keine Bewertungen

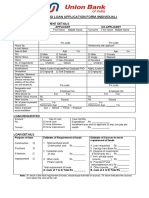

- Union Home Application FormDokument3 SeitenUnion Home Application FormHAINDAVI REDDY GUDDETINoch keine Bewertungen

- Accounting For Public Sector and Civil Society 2022 LatestDokument170 SeitenAccounting For Public Sector and Civil Society 2022 LatestZerai Hagos HailemariamNoch keine Bewertungen

- Nhmfc-Unregistered CosDokument5 SeitenNhmfc-Unregistered CosChris RetardoNoch keine Bewertungen

- Question 1-10-20 Marks Dan James Obtained His Cpa Designation 3 Months Ago After ArticlingDokument6 SeitenQuestion 1-10-20 Marks Dan James Obtained His Cpa Designation 3 Months Ago After ArticlingCharlotteNoch keine Bewertungen

- Abm Acctg Firm Section 2am 2Dokument40 SeitenAbm Acctg Firm Section 2am 2Diana Rosales CalNoch keine Bewertungen

- Tutorial Letter 102/3/2022: General Financial ReportingDokument110 SeitenTutorial Letter 102/3/2022: General Financial ReportingMelissaNoch keine Bewertungen

- Accounting Global 9th Edition Horngren Solutions ManualDokument12 SeitenAccounting Global 9th Edition Horngren Solutions Manualmrsamandareynoldsiktzboqwad100% (26)

- AFAR Review Midterm ExamDokument10 SeitenAFAR Review Midterm ExamZyrah Mae SaezNoch keine Bewertungen

- Tybaf - Dhruvil Jain - 038Dokument5 SeitenTybaf - Dhruvil Jain - 038DhruviNoch keine Bewertungen