Das könnte Ihnen auch gefallen

- Portfolio Insurance Strategies - OBPI Versus CPPIDokument16 SeitenPortfolio Insurance Strategies - OBPI Versus CPPIKaushal ShahNoch keine Bewertungen

- Review Capital BudgetingDokument22 SeitenReview Capital BudgetingJamesno LumbNoch keine Bewertungen

- Cvp-Analysis PDFDokument11 SeitenCvp-Analysis PDFanon_901038567Noch keine Bewertungen

- Derivatives ChaptersDokument19 SeitenDerivatives Chapterslatiful188Noch keine Bewertungen

- Ch11 Test Bank For Intermediate Accounting Ifrs Edition 3eDokument40 SeitenCh11 Test Bank For Intermediate Accounting Ifrs Edition 3eakid windrayaNoch keine Bewertungen

- Ipsas 17 PpeDokument29 SeitenIpsas 17 PpeEZEKIELNoch keine Bewertungen

- Absorption and Variable CostingDokument8 SeitenAbsorption and Variable CostingGerard Beltran ArcaNoch keine Bewertungen

- ch11 PDFDokument39 Seitench11 PDFerylpaez89% (9)

- Afarq 2 Corporate LiquidationDokument4 SeitenAfarq 2 Corporate LiquidationCPANoch keine Bewertungen

- D. in Any of TheseDokument3 SeitenD. in Any of TheseAlrac Garcia100% (1)

- Position Paper FinalDokument57 SeitenPosition Paper FinalCPANoch keine Bewertungen

- Solved Problems Depreciation, Impairment and DepletionDokument22 SeitenSolved Problems Depreciation, Impairment and DepletionCassandra Dianne Ferolino MacadoNoch keine Bewertungen

- Woodward Life Cycle CostingDokument10 SeitenWoodward Life Cycle CostingmelatorNoch keine Bewertungen

- 1.3. Sales: Regulatory Framework For Business Transactions MadbolivarDokument9 Seiten1.3. Sales: Regulatory Framework For Business Transactions MadbolivarJims Leñar CezarNoch keine Bewertungen

- PPE Depreciation & ImpairmentDokument25 SeitenPPE Depreciation & ImpairmentSummer Star0% (1)

- CH 11Dokument40 SeitenCH 11Corliss Ko100% (1)

- Ms-08 Activity-Based Costing & Bala) Ed Scoregard: Resa ?4E Ret M Scae (At /Fun4'Tt4Aiqtfuararyrr RRT SenaarzDokument12 SeitenMs-08 Activity-Based Costing & Bala) Ed Scoregard: Resa ?4E Ret M Scae (At /Fun4'Tt4Aiqtfuararyrr RRT SenaarzJamesno LumbNoch keine Bewertungen

- Learning Advancement Cpa Review Center: Revenue From Contracts With CustomersDokument4 SeitenLearning Advancement Cpa Review Center: Revenue From Contracts With CustomersCPANoch keine Bewertungen

- Toa 333-3 PDFDokument1 SeiteToa 333-3 PDFCPANoch keine Bewertungen

- Chapter 14 1Dokument83 SeitenChapter 14 1Юлия КириченкоNoch keine Bewertungen

- Basic Principles On TaxationDokument23 SeitenBasic Principles On TaxationKath PostreNoch keine Bewertungen

- Ft:qufr Eiilfi F, FSQ Q ': AffirDokument12 SeitenFt:qufr Eiilfi F, FSQ Q ': AffirMansi Kaushik XI -ENoch keine Bewertungen

- Dividend Policy TheoryDokument14 SeitenDividend Policy Theorydennise16Noch keine Bewertungen

- Analysis and Interpretation of FSDokument5 SeitenAnalysis and Interpretation of FSRizia Feh EustaquioNoch keine Bewertungen

- Chapter 2 Fair Value Measurement: Learning ObjectivesDokument11 SeitenChapter 2 Fair Value Measurement: Learning Objectivessamuel_dwumfourNoch keine Bewertungen

- Fif, T n'1t : Q, o D.".-,". R, , 5-Il, L"!,' 2qC! 2) I Ti 2) JTDokument1 SeiteFif, T n'1t : Q, o D.".-,". R, , 5-Il, L"!,' 2qC! 2) I Ti 2) JTCPANoch keine Bewertungen

- Econ Art 1Dokument19 SeitenEcon Art 1Misganaw MarewNoch keine Bewertungen

- Government AccountingDokument6 SeitenGovernment AccountingroliNoch keine Bewertungen

- TNT' T Flhilcvt: Cott Hof, L Esitar LleDokument5 SeitenTNT' T Flhilcvt: Cott Hof, L Esitar Llecezyyyyyy100% (1)

- MS Quiz 4Dokument2 SeitenMS Quiz 4nikNoch keine Bewertungen

- Ch11 Kieso Ifrs Test BankDokument40 SeitenCh11 Kieso Ifrs Test BankTrinh LêNoch keine Bewertungen

- RR No. 20-2020 PDFDokument2 SeitenRR No. 20-2020 PDFBobby Olavides SebastianNoch keine Bewertungen

- ch11 Doc PDF - 2 PDFDokument39 Seitench11 Doc PDF - 2 PDFRenzo RamosNoch keine Bewertungen

- MC 67Dokument40 SeitenMC 67Hanuma ReddyNoch keine Bewertungen

- #Ih" ."Rit" It "O : " 'D"ingDokument1 Seite#Ih" ."Rit" It "O : " 'D"ingJp CombisNoch keine Bewertungen

- Pricing Strategies16022023161224Dokument21 SeitenPricing Strategies16022023161224Christine AlumNoch keine Bewertungen

- Variable Exam 2Dokument13 SeitenVariable Exam 2Claudine Puyao100% (1)

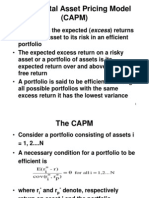

- The Capital Asset Pricing Model (CAPM)Dokument31 SeitenThe Capital Asset Pricing Model (CAPM)Tanmay AbhijeetNoch keine Bewertungen

- Contractor Registration Regulation-Aug.18 PDFDokument38 SeitenContractor Registration Regulation-Aug.18 PDFSaurabh DwivediNoch keine Bewertungen

- PpeDokument4 SeitenPpeRed DerrNoch keine Bewertungen

- At Preweek ReviewDokument24 SeitenAt Preweek ReviewJazerMolosNoch keine Bewertungen

- CREW: Department of Health and Human Services: Public Affairs Firms Documents: 04/04/07: HHS FOIA Response 2 of 5Dokument149 SeitenCREW: Department of Health and Human Services: Public Affairs Firms Documents: 04/04/07: HHS FOIA Response 2 of 5CREWNoch keine Bewertungen

- Portfolio ConstructionDokument27 SeitenPortfolio ConstructionAgnivesh JayaNoch keine Bewertungen

- Chap 005Dokument30 SeitenChap 005trinhbang100% (1)

- Cpar - Toa 07.27.13Dokument12 SeitenCpar - Toa 07.27.13Charry Ramos100% (3)

- Final - Asset Accounting ProcedureDokument38 SeitenFinal - Asset Accounting ProcedureSonianNareshNoch keine Bewertungen

- Upload Agreement - Neon Heights 3Dokument25 SeitenUpload Agreement - Neon Heights 3Amol DhanvijNoch keine Bewertungen

- MAS16Dokument12 SeitenMAS16Kyaw Htin Win50% (2)

- 1 Engineer's Certificate On Cost Incurred On Project (Form 2)Dokument3 Seiten1 Engineer's Certificate On Cost Incurred On Project (Form 2)Syed Umair MadniNoch keine Bewertungen

- (Freory Accounts: Assets Commodities I N-'Rentory Discouni: Gross GrossDokument12 Seiten(Freory Accounts: Assets Commodities I N-'Rentory Discouni: Gross GrossPhilip CastroNoch keine Bewertungen

- Tfie Review WF Acr, Wntancy: A Counting InstallmentDokument1 SeiteTfie Review WF Acr, Wntancy: A Counting InstallmentJohn Francis Raspado AnchetaNoch keine Bewertungen

- Ias 16 - PpeDokument4 SeitenIas 16 - Ppecar itselfNoch keine Bewertungen

- Solution Cost Carter Usry 13th Edition PDFDokument690 SeitenSolution Cost Carter Usry 13th Edition PDFNoel CaingletNoch keine Bewertungen

- Cost Behavior Analysis and UseDokument3 SeitenCost Behavior Analysis and Usepablopaul56Noch keine Bewertungen

- Borrowing Costs: Myanmar Accounting Standard 23Dokument5 SeitenBorrowing Costs: Myanmar Accounting Standard 23Kyaw Htin WinNoch keine Bewertungen

- Fully Vouched Contingent BillDokument2 SeitenFully Vouched Contingent BillVirendra MahalaNoch keine Bewertungen

- TOA CparDokument12 SeitenTOA CparHerald Gangcuangco100% (2)

- CHAPTER 10 Plant Assets and Intangibles: Objective 1: Measure The Cost of A Plant AssetDokument9 SeitenCHAPTER 10 Plant Assets and Intangibles: Objective 1: Measure The Cost of A Plant AssetAhmed RawyNoch keine Bewertungen

- CAG Circular On MT 05e61ddc6cc64e4 27692120 - 230526 - 110607Dokument3 SeitenCAG Circular On MT 05e61ddc6cc64e4 27692120 - 230526 - 110607Kartik SharmaNoch keine Bewertungen

- BA 114.1 Handout On PPEDokument5 SeitenBA 114.1 Handout On PPEHuarde SophiaNoch keine Bewertungen

- Acct 385 Blocher El1-33Dokument14 SeitenAcct 385 Blocher El1-33Queen Jean MielNoch keine Bewertungen

- LeadDokument46 SeitenLeadCPANoch keine Bewertungen

- Cpar AuditingDokument10 SeitenCpar AuditingCPANoch keine Bewertungen

- J "0 A. N,", o ,: UnitDokument1 SeiteJ "0 A. N,", o ,: UnitCPANoch keine Bewertungen

- MS 3412-3Dokument1 SeiteMS 3412-3CPANoch keine Bewertungen

- MS 3412-2Dokument1 SeiteMS 3412-2CPANoch keine Bewertungen

- Financial: " " 1" 2. 3. 4. 5. RetiosDokument1 SeiteFinancial: " " 1" 2. 3. 4. 5. RetiosCPANoch keine Bewertungen

- Fif, T n'1t : Q, o D.".-,". R, , 5-Il, L"!,' 2qC! 2) I Ti 2) JTDokument1 SeiteFif, T n'1t : Q, o D.".-,". R, , 5-Il, L"!,' 2qC! 2) I Ti 2) JTCPANoch keine Bewertungen

- MS 3412-8Dokument1 SeiteMS 3412-8CPANoch keine Bewertungen

- Rurnover: '.::::"" ':'U ' O, .-Ffhsffihr"ODokument1 SeiteRurnover: '.::::"" ':'U ' O, .-Ffhsffihr"OCPANoch keine Bewertungen

- Iht#I T:,Ffi, I:Trri ,:FFJLLLJ H:!:Iiiff: at ofDokument1 SeiteIht#I T:,Ffi, I:Trri ,:FFJLLLJ H:!:Iiiff: at ofCPANoch keine Bewertungen

- Handouts ConsolidationSubsequent To Date of AcquisitionDokument5 SeitenHandouts ConsolidationSubsequent To Date of AcquisitionCPANoch keine Bewertungen

- RFBT 34new-3Dokument1 SeiteRFBT 34new-3CPANoch keine Bewertungen

- Toa 334-2Dokument1 SeiteToa 334-2CPANoch keine Bewertungen

- Toa 334-1 PDFDokument1 SeiteToa 334-1 PDFCPANoch keine Bewertungen

- Regulatory Framework For Business Transactions Madbolivar: Quiz 2-ContractsDokument2 SeitenRegulatory Framework For Business Transactions Madbolivar: Quiz 2-ContractsCPANoch keine Bewertungen

- Toa 333-1Dokument1 SeiteToa 333-1CPANoch keine Bewertungen

- RFBT 34new-2Dokument1 SeiteRFBT 34new-2CPANoch keine Bewertungen

- Financial Accounting and Reporting MsvegaDokument2 SeitenFinancial Accounting and Reporting MsvegaCPANoch keine Bewertungen

- C. D. A. B. C. It D.: Il', I:TjrDokument1 SeiteC. D. A. B. C. It D.: Il', I:TjrCPANoch keine Bewertungen

- BDO CirDokument2 SeitenBDO CirCPANoch keine Bewertungen

- Handouts ConsolidationIntercompany Sale of Plant AssetsDokument3 SeitenHandouts ConsolidationIntercompany Sale of Plant AssetsCPANoch keine Bewertungen

- Audit of PpeDokument8 SeitenAudit of PpeCPANoch keine Bewertungen

- Special Power of AttorneyDokument2 SeitenSpecial Power of AttorneyCPANoch keine Bewertungen

- Handouts PartnershipDokument9 SeitenHandouts PartnershipCPANoch keine Bewertungen

- Position:: President TreasurerDokument5 SeitenPosition:: President TreasurerCPANoch keine Bewertungen