Das könnte Ihnen auch gefallen

- Made in JapanDokument14 SeitenMade in Japandurlit50% (4)

- Japanese Global CompaniesDokument20 SeitenJapanese Global CompaniesSesti Harkies FitrianiNoch keine Bewertungen

- Investment Theories.Dokument28 SeitenInvestment Theories.Sapna KumariNoch keine Bewertungen

- Daniels IBT 16e Final PPT 01Dokument48 SeitenDaniels IBT 16e Final PPT 01rola mohammadNoch keine Bewertungen

- Advise Zara On Cultural Tension and Negotiation With JapanDokument20 SeitenAdvise Zara On Cultural Tension and Negotiation With JapanCheco Martinez GaribayNoch keine Bewertungen

- Revision For Test Hadiff PDFDokument3 SeitenRevision For Test Hadiff PDFHadiff ZafriNoch keine Bewertungen

- 2.3.1 Investor BiasesDokument30 Seiten2.3.1 Investor BiasesdivyanshNoch keine Bewertungen

- Management: Managing Across CulturesDokument31 SeitenManagement: Managing Across CulturesMd HimelNoch keine Bewertungen

- Programme PublicDokument44 SeitenProgramme PublicaptureincNoch keine Bewertungen

- Finance Class Overview and Market InsightsDokument14 SeitenFinance Class Overview and Market Insightsharshit guptaNoch keine Bewertungen

- IBM CH 1 2Dokument43 SeitenIBM CH 1 2kirkostadeseNoch keine Bewertungen

- International Business The Challenge of Global Competition 13th Edition Ball Solutions ManualDokument25 SeitenInternational Business The Challenge of Global Competition 13th Edition Ball Solutions ManualStephenBowenbxtm100% (53)

- 5th Class Shorter VersionDokument15 Seiten5th Class Shorter Versionk61.2214560031Noch keine Bewertungen

- MGT 112 Global Business StrategyDokument38 SeitenMGT 112 Global Business StrategyOmar RiberiaNoch keine Bewertungen

- Dwnload Full International Business The Challenge of Global Competition 13th Edition Ball Solutions Manual PDFDokument35 SeitenDwnload Full International Business The Challenge of Global Competition 13th Edition Ball Solutions Manual PDFmorselhurly.qa26100% (7)

- Introduction To IBMDokument6 SeitenIntroduction To IBMCaroline MoforNoch keine Bewertungen

- NestleDokument28 SeitenNestlewazirsadiqNoch keine Bewertungen

- Chap5 Managing Across CulturesDokument30 SeitenChap5 Managing Across CulturesshoaibNoch keine Bewertungen

- Prof - Shikha Atri: International Finance Economics & Foreign ExchangeDokument28 SeitenProf - Shikha Atri: International Finance Economics & Foreign ExchangecoolpalakNoch keine Bewertungen

- Multinational Firms: Week 2: Multinationality Vs ExportingDokument43 SeitenMultinational Firms: Week 2: Multinationality Vs ExportinglinhtrunggNoch keine Bewertungen

- FINA 652 Private Equity: Class I Introduction To The Private Equity IndustryDokument53 SeitenFINA 652 Private Equity: Class I Introduction To The Private Equity IndustryHarsh SrivastavaNoch keine Bewertungen

- Cross Cultural Management Frank McDonaldDokument30 SeitenCross Cultural Management Frank McDonaldP100% (1)

- Reading-The-Global-Business-Environment-1Dokument19 SeitenReading-The-Global-Business-Environment-1jolar laraNoch keine Bewertungen

- Barriers and Preparation for International NegotiationsDokument36 SeitenBarriers and Preparation for International NegotiationsBenjamin Adelwini BugriNoch keine Bewertungen

- Mansourfar Et AlDokument7 SeitenMansourfar Et AlGurvinder Singh DhillonNoch keine Bewertungen

- Midterm NegotiationDokument3 SeitenMidterm Negotiationkhanh le hongNoch keine Bewertungen

- Globalization & The MNCDokument26 SeitenGlobalization & The MNCAllwynThomasNoch keine Bewertungen

- AOB - Session 9-10 (2) - Lecture NotesDokument63 SeitenAOB - Session 9-10 (2) - Lecture NotesNhiNoch keine Bewertungen

- Japanese Success Through Quality Focus and Efficient ProductionDokument34 SeitenJapanese Success Through Quality Focus and Efficient Productionnikhil yadavNoch keine Bewertungen

- Event - Global Pe-Final Empea - WK - 5709Dokument113 SeitenEvent - Global Pe-Final Empea - WK - 5709amitsh20072458Noch keine Bewertungen

- FIN3330 Alternative Investments OverviewDokument20 SeitenFIN3330 Alternative Investments OverviewjamesNoch keine Bewertungen

- International Finance Lecture on FX Markets and FX ForwardsDokument45 SeitenInternational Finance Lecture on FX Markets and FX ForwardsRaghavNoch keine Bewertungen

- International Business Course FullDokument22 SeitenInternational Business Course Fullarahman198450% (2)

- Introduction to International Financial ManagementDokument36 SeitenIntroduction to International Financial ManagementKamal KantNoch keine Bewertungen

- Bridges to Japanese Business Etiquette - Understanding Japan Cross-cultural Management: Bridges to Japanese Business Etiquette - Understanding Japan Cross-cultural ManagementVon EverandBridges to Japanese Business Etiquette - Understanding Japan Cross-cultural Management: Bridges to Japanese Business Etiquette - Understanding Japan Cross-cultural ManagementNoch keine Bewertungen

- Drivers and Triggers of Comparative HRMDokument6 SeitenDrivers and Triggers of Comparative HRMorangeshower0% (1)

- The 1997 - 1998 Asian Financial Crisis: Submitted By: Syed Mohd. ZaidDokument49 SeitenThe 1997 - 1998 Asian Financial Crisis: Submitted By: Syed Mohd. ZaidMohd Zaid SyedNoch keine Bewertungen

- Landscape and Challenges of International Business - INTE60006ADokument50 SeitenLandscape and Challenges of International Business - INTE60006Adhaval patelNoch keine Bewertungen

- IBM NotesDokument58 SeitenIBM NotesAkshaya N-2020Noch keine Bewertungen

- Foreign Exchange Management With Questions FIN 415Dokument5 SeitenForeign Exchange Management With Questions FIN 415Sayeda Ummul WaraNoch keine Bewertungen

- International BusinessDokument61 SeitenInternational BusinessHoàng Hạnh TrangNoch keine Bewertungen

- S-Chapter 1Dokument37 SeitenS-Chapter 1Minh LêNoch keine Bewertungen

- Wk1 - MK - Bisnis InternasionalDokument29 SeitenWk1 - MK - Bisnis InternasionalWulan AdityaNoch keine Bewertungen

- Transnational CorporationsDokument17 SeitenTransnational CorporationsbhuwanvikramNoch keine Bewertungen

- PM Ch04 Managing in The Global ArenaDokument22 SeitenPM Ch04 Managing in The Global ArenaHải Anh NguyễnNoch keine Bewertungen

- International Relations:: Unit V Chap 1Dokument14 SeitenInternational Relations:: Unit V Chap 1Suresh KumarNoch keine Bewertungen

- Week 01 - Global MarketDokument52 SeitenWeek 01 - Global MarketCesar BravoNoch keine Bewertungen

- Ihrm StudentsDokument47 SeitenIhrm StudentsNidhi AgarwalNoch keine Bewertungen

- 337751124-Chapter-1-Globalisation-SummaryDokument21 Seiten337751124-Chapter-1-Globalisation-Summarypink pinkNoch keine Bewertungen

- Leading The Effective Sales Force: The Asian Sales Force Management EnvironmentDokument82 SeitenLeading The Effective Sales Force: The Asian Sales Force Management EnvironmentMahmoud Abd El GwadNoch keine Bewertungen

- Fang, T. (2005, Book Chapter) - Chinese Business Style: A Regional Approach. in A. Macbean & D. Brown (Eds.), Cha..Dokument24 SeitenFang, T. (2005, Book Chapter) - Chinese Business Style: A Regional Approach. in A. Macbean & D. Brown (Eds.), Cha..mỹ linh lêNoch keine Bewertungen

- 商务英语视听说(第一册)unit 3Dokument34 Seiten商务英语视听说(第一册)unit 3Lynne CaoNoch keine Bewertungen

- CH 01Dokument17 SeitenCH 01gadox47306Noch keine Bewertungen

- Week 7 IBTDokument11 SeitenWeek 7 IBTThamuz LunoxNoch keine Bewertungen

- How Japanese Market Research Differs From US MethodsDokument5 SeitenHow Japanese Market Research Differs From US MethodsBilal SiddiquiNoch keine Bewertungen

- 01 IntroductionDokument57 Seiten01 Introductionsanthamoorthi kNoch keine Bewertungen

- FM 8 Module 2 Multinational Financial ManagementDokument35 SeitenFM 8 Module 2 Multinational Financial ManagementJasper Mortos VillanuevaNoch keine Bewertungen

- Japan's Economic Trap and Demographic ChallengeDokument8 SeitenJapan's Economic Trap and Demographic ChallengeManasvi BaliNoch keine Bewertungen

- 3-The Triad An International Business (International Business)Dokument4 Seiten3-The Triad An International Business (International Business)Asjad Jamshed80% (5)

- The Globalization of Chinese Companies: Strategies for Conquering International MarketsVon EverandThe Globalization of Chinese Companies: Strategies for Conquering International MarketsNoch keine Bewertungen

- Viability of Mixed-Use DevelopmentsDokument2 SeitenViability of Mixed-Use DevelopmentsogrimlookednightNoch keine Bewertungen

- Viability of Mixed-Use DevelopmentsDokument2 SeitenViability of Mixed-Use DevelopmentsogrimlookednightNoch keine Bewertungen

- Joint Venture Conflicts of InterestDokument4 SeitenJoint Venture Conflicts of InterestogrimlookednightNoch keine Bewertungen

- Taxation On Acquisition of Shares, Assign of PropertiesDokument2 SeitenTaxation On Acquisition of Shares, Assign of PropertiesogrimlookednightNoch keine Bewertungen

- Philippine Credit Rating MovementsDokument1 SeitePhilippine Credit Rating MovementsogrimlookednightNoch keine Bewertungen

- Digital Payment & TransactionsDokument91 SeitenDigital Payment & Transactionschaliya00767% (3)

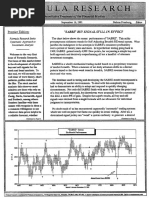

- Freeburg, Nelson - Formula Research NewsletterDokument544 SeitenFreeburg, Nelson - Formula Research NewsletterSenthil Kumar90% (10)

- Chapter 12 Marketing ChannelsDokument7 SeitenChapter 12 Marketing ChannelsTaylor KalinowskiNoch keine Bewertungen

- Corporate Governance CH.1Dokument123 SeitenCorporate Governance CH.1Mubeen WahlaNoch keine Bewertungen

- Argidius Call For BDS ProposalDokument8 SeitenArgidius Call For BDS ProposalEmmanuel Alenga MakhetiNoch keine Bewertungen

- Agrarian Law PrimerDokument9 SeitenAgrarian Law PrimerAngelo Raphael B. DelmundoNoch keine Bewertungen

- Idc Managed Services White Paper PDFDokument26 SeitenIdc Managed Services White Paper PDFمحمد الواثقNoch keine Bewertungen

- Blanchard Ch12 2011 1 C. GROTHDokument54 SeitenBlanchard Ch12 2011 1 C. GROTHikakkosNoch keine Bewertungen

- Organizational Management - FoodpandaDokument3 SeitenOrganizational Management - FoodpandaVveivvNoch keine Bewertungen

- A Review of Industrialised Building SystDokument5 SeitenA Review of Industrialised Building SystSHARIFAH ZARITH SOFIA WAN MALIKNoch keine Bewertungen

- Clark Jessica ResumeDokument1 SeiteClark Jessica Resumeapi-437607237Noch keine Bewertungen

- FS QuestionnaireDokument8 SeitenFS QuestionnaireFrancis J.Noch keine Bewertungen

- Project Manager - JG 4 - RPLN0077020Dokument5 SeitenProject Manager - JG 4 - RPLN0077020kkNoch keine Bewertungen

- Church Budget Template (Advanced) (Spanish)Dokument11 SeitenChurch Budget Template (Advanced) (Spanish)FrancexcoNoch keine Bewertungen

- Taguro Trucking FinancialsDokument5 SeitenTaguro Trucking FinancialsDavid GuevarraNoch keine Bewertungen

- Term Sheet For Sacramento ArenaDokument45 SeitenTerm Sheet For Sacramento ArenaIsaac GonzalezNoch keine Bewertungen

- National Seminar 11Dokument4 SeitenNational Seminar 11Sumit Shankar KunduNoch keine Bewertungen

- AEPEDADokument5 SeitenAEPEDAMufaddalNoch keine Bewertungen

- Rol Del Estado en Materia de Seguridad SocialDokument18 SeitenRol Del Estado en Materia de Seguridad SocialGabriel Nahuel LopezNoch keine Bewertungen

- Xi Grace Luo LinkedinDokument3 SeitenXi Grace Luo Linkedinapi-289180707Noch keine Bewertungen

- Vensa work order for construction of residential schoolDokument9 SeitenVensa work order for construction of residential schoolAshutosh Kumar DwivediNoch keine Bewertungen

- Devlpoment Class 10Dokument16 SeitenDevlpoment Class 10NILESH dangiNoch keine Bewertungen

- Mario Augusto de Castro - Fenway - Gillete Case AnalysisDokument7 SeitenMario Augusto de Castro - Fenway - Gillete Case AnalysisKiran RimalNoch keine Bewertungen

- GPP Meeting Highlights Fall 2014 Finance DeptDokument14 SeitenGPP Meeting Highlights Fall 2014 Finance DeptKabuRideNoch keine Bewertungen

- Delhi University Economics Dept Meeting Minutes on Macroeconomics CourseDokument2 SeitenDelhi University Economics Dept Meeting Minutes on Macroeconomics Coursedheeraj sehgalNoch keine Bewertungen

- Entrepreneurship Lecture Number 5 6 and 7Dokument36 SeitenEntrepreneurship Lecture Number 5 6 and 7UMAIR TARIQ L1F17BBAM0054Noch keine Bewertungen

- Problems 3 Prelim TaskDokument8 SeitenProblems 3 Prelim TaskJohn Francis Rosas100% (2)

- Final Agenda For 27th SCMDokument53 SeitenFinal Agenda For 27th SCMSohu DineshNoch keine Bewertungen

- TallyDokument8 SeitenTallyHarsh GuptaNoch keine Bewertungen

- ETax RegDokument1 SeiteETax Regkeerthibalan100% (1)