Das könnte Ihnen auch gefallen

- Total Clearing Time-Current Characteristic Curves: Smu Fuse Units For Voltage-Transformer Applications-S&C Standard SpeedDokument1 SeiteTotal Clearing Time-Current Characteristic Curves: Smu Fuse Units For Voltage-Transformer Applications-S&C Standard SpeedObed GarcíaNoch keine Bewertungen

- DES-101B: Multiple of Trip Rating PlugDokument1 SeiteDES-101B: Multiple of Trip Rating Plugjurica_2006Noch keine Bewertungen

- Des-095b - Long TimeDokument1 SeiteDes-095b - Long Timeshrikanth5singhNoch keine Bewertungen

- Multiples of Ground Fault Pickup SettingDokument1 SeiteMultiples of Ground Fault Pickup SettingjosehenriquezsotoNoch keine Bewertungen

- Total Clearing Time-Current Characteristic Curves: Fault Tamer Fuse LimitersDokument1 SeiteTotal Clearing Time-Current Characteristic Curves: Fault Tamer Fuse LimitersStoner WddNoch keine Bewertungen

- TCC Number 450 8 PDFDokument1 SeiteTCC Number 450 8 PDFjavier jimenez rodriguezNoch keine Bewertungen

- Model 9F54Dfc Series: Current in AmperesDokument1 SeiteModel 9F54Dfc Series: Current in AmperesPaulo H TavaresNoch keine Bewertungen

- Minimum Melting Time-Current Characteristic CurvesDokument1 SeiteMinimum Melting Time-Current Characteristic CurvesObed GarcíaNoch keine Bewertungen

- Ges 6194 PDFDokument2 SeitenGes 6194 PDFjurica_2006Noch keine Bewertungen

- Ge Tey3100 MCB ManualDokument1 SeiteGe Tey3100 MCB ManualPrathap KumarNoch keine Bewertungen

- 165 6 PDFDokument1 Seite165 6 PDFGonzalo Peñafiel CondoriNoch keine Bewertungen

- Rop Sinaw Cable & Water Line RouteDokument1 SeiteRop Sinaw Cable & Water Line RouteAkbar DahriNoch keine Bewertungen

- A005 DOORS Old Drawing FOR SPOT DETAIL ONLYDokument13 SeitenA005 DOORS Old Drawing FOR SPOT DETAIL ONLYJessica PerezNoch keine Bewertungen

- 2021 Nhap FPDokument1 Seite2021 Nhap FPChristine DavidNoch keine Bewertungen

- Kerja-Kerja Menaiktaraf Sistem Takungan Air Mentah Di Mukasauk Loji Rawatan Air (Lra) Kina Benuwa, Wilayah Persekutuan LabuanDokument1 SeiteKerja-Kerja Menaiktaraf Sistem Takungan Air Mentah Di Mukasauk Loji Rawatan Air (Lra) Kina Benuwa, Wilayah Persekutuan LabuanFarith AkbarNoch keine Bewertungen

- 165 6 2Dokument1 Seite165 6 2Carlos A. Carpio CárdenasNoch keine Bewertungen

- DES-095B: Approximately (0.784-Actual Pickup)Dokument1 SeiteDES-095B: Approximately (0.784-Actual Pickup)shrikanth5singhNoch keine Bewertungen

- Activity 2 - Floor Plan Rendering 2023 - 4Dokument1 SeiteActivity 2 - Floor Plan Rendering 2023 - 4Lourd Raphael Thaddeus EmataNoch keine Bewertungen

- Updated WindowsDokument1 SeiteUpdated Windowsfrancis sebastian lagamayoNoch keine Bewertungen

- Schedule of WindowsDokument1 SeiteSchedule of Windowsfrancis sebastian lagamayoNoch keine Bewertungen

- Second Floor Plumbing Layout: Landing LandingDokument1 SeiteSecond Floor Plumbing Layout: Landing Landingbea100% (1)

- Two Storey House Plan 1Dokument1 SeiteTwo Storey House Plan 1Edmar InietoNoch keine Bewertungen

- T&B DetailsDokument1 SeiteT&B DetailshelloNoch keine Bewertungen

- MALE AND FEMALE DORMITORY-augDokument1 SeiteMALE AND FEMALE DORMITORY-augRexner CandelarioNoch keine Bewertungen

- GES-6122C: Multiples of Current RatingDokument1 SeiteGES-6122C: Multiples of Current RatingAdolfo Sotomayor BurgosNoch keine Bewertungen

- GES-6121C: Multiples of Current RatingDokument1 SeiteGES-6121C: Multiples of Current RatingAdolfo Sotomayor BurgosNoch keine Bewertungen

- Available Three-Phase Symmetrical Short-Circuit Current (Kiloamps)Dokument1 SeiteAvailable Three-Phase Symmetrical Short-Circuit Current (Kiloamps)jurica_2006Noch keine Bewertungen

- Available Three-Phase Symmetrical Short-Circuit Current (Kiloamps)Dokument1 SeiteAvailable Three-Phase Symmetrical Short-Circuit Current (Kiloamps)Amr AhmedNoch keine Bewertungen

- Ges 6120d Thed GeDokument1 SeiteGes 6120d Thed GeBolivar MartinezNoch keine Bewertungen

- Ges 6108c Type TQD GeDokument1 SeiteGes 6108c Type TQD GeBolivar MartinezNoch keine Bewertungen

- Multiples of Current Rating: Molded Case Circuit Breakers Q LineDokument1 SeiteMultiples of Current Rating: Molded Case Circuit Breakers Q LineMUSIC ELECNoch keine Bewertungen

- Kolkata 700 001 7, Hare StreetDokument1 SeiteKolkata 700 001 7, Hare Streetkoushik42000Noch keine Bewertungen

- Office A1 PDFDokument1 SeiteOffice A1 PDFalfredo agsunodNoch keine Bewertungen

- Drawing ReferenceDokument1 SeiteDrawing ReferenceFIRMANSYAHNoch keine Bewertungen

- Multiples of Current Rating: Molded Case Circuit BreakersDokument1 SeiteMultiples of Current Rating: Molded Case Circuit BreakersAmr AhmedNoch keine Bewertungen

- Ges 6231aDokument1 SeiteGes 6231aAmr AhmedNoch keine Bewertungen

- Final ProjectDokument1 SeiteFinal ProjectIsraelNoch keine Bewertungen

- Platform Ölçüleri̇Dokument1 SeitePlatform Ölçüleri̇nrobisetiawan17Noch keine Bewertungen

- Aemax: Schedule of DoorsDokument1 SeiteAemax: Schedule of DoorsMary Mae MinaNoch keine Bewertungen

- Multiples of Current Rating: Molded Case Circuit Breakers Q LineDokument1 SeiteMultiples of Current Rating: Molded Case Circuit Breakers Q LineMUSIC ELECNoch keine Bewertungen

- Foundation PlanDokument1 SeiteFoundation PlanIbbe CaguiatNoch keine Bewertungen

- Demollation PlanDokument1 SeiteDemollation Planmurtaza.hashimi2013Noch keine Bewertungen

- ATUM (Rhamnosa E.coli)Dokument4 SeitenATUM (Rhamnosa E.coli)Ruth MichelleeNoch keine Bewertungen

- Section Aa' PlanDokument7 SeitenSection Aa' PlanMayuriNoch keine Bewertungen

- 155 - Flow Chart CV .8Dokument1 Seite155 - Flow Chart CV .8Mugywara luNoch keine Bewertungen

- PLAN - 17DC0187 Part 6 of 6Dokument4 SeitenPLAN - 17DC0187 Part 6 of 6NathanielNoch keine Bewertungen

- A 1Dokument1 SeiteA 1joseph arao-araoNoch keine Bewertungen

- P2 PlanDokument1 SeiteP2 PlanFrancis Lloyd MalganaNoch keine Bewertungen

- S-12 FCD Almeda 2 CanopyDokument1 SeiteS-12 FCD Almeda 2 CanopyAlvin SanvictoresNoch keine Bewertungen

- Ground Floor PlanDokument1 SeiteGround Floor PlanNana BarimaNoch keine Bewertungen

- Layout Kitchen Mang Engking Gubeng Oct 2022 OrderDokument1 SeiteLayout Kitchen Mang Engking Gubeng Oct 2022 OrderIlham Ibadul AzizNoch keine Bewertungen

- Plan at El (+) 16.200/el (+) 15.500M Level: Up UpDokument1 SeitePlan at El (+) 16.200/el (+) 15.500M Level: Up Upsubramanian SivaNoch keine Bewertungen

- 18 21 (Rev-00) - Abut-8Dokument4 Seiten18 21 (Rev-00) - Abut-8S.m. MoniruzzamanNoch keine Bewertungen

- Kitchen Library: 25,000 200 8,700 200 4,000 200 2,000 200 2,000 200 1,100 200 800 200 4,550 450 Rare ElevationDokument1 SeiteKitchen Library: 25,000 200 8,700 200 4,000 200 2,000 200 2,000 200 1,100 200 800 200 4,550 450 Rare ElevationBrian LubangakeneNoch keine Bewertungen

- Drawing For IMB-Gudang 60M X 30M-PT Detta Agro ServiceDokument4 SeitenDrawing For IMB-Gudang 60M X 30M-PT Detta Agro ServiceNugraha AkbarNoch keine Bewertungen

- E1 Sample Working DrawingDokument1 SeiteE1 Sample Working DrawingjasonNoch keine Bewertungen

- First Floor Lighting Layout Second Lighting Layout: Cyrus Construction Development GroupDokument1 SeiteFirst Floor Lighting Layout Second Lighting Layout: Cyrus Construction Development GroupCyrus RivasNoch keine Bewertungen

- ECI 2080lumbang UtilKit and Driveway Key Plan 04082024 LAYOUTDokument1 SeiteECI 2080lumbang UtilKit and Driveway Key Plan 04082024 LAYOUTjosh cuaNoch keine Bewertungen

- L8 On UCP600 Article 08 October 16 Intake PDFDokument27 SeitenL8 On UCP600 Article 08 October 16 Intake PDFAsadul HoqueNoch keine Bewertungen

- L1 On Introduction April Intake 16Dokument38 SeitenL1 On Introduction April Intake 16Asadul Hoque100% (1)

- L7 On UCP600 Article 07 October 16 Intake PDFDokument25 SeitenL7 On UCP600 Article 07 October 16 Intake PDFAsadul HoqueNoch keine Bewertungen

- L5 On UCP600 Article 04 and Article 05 October 16 Intake 16 Final PDFDokument21 SeitenL5 On UCP600 Article 04 and Article 05 October 16 Intake 16 Final PDFAsadul HoqueNoch keine Bewertungen

- L4 On UCP600 Article 03 October 16 Intake PDFDokument29 SeitenL4 On UCP600 Article 03 October 16 Intake PDFAsadul HoqueNoch keine Bewertungen

- Bangladesh BankDokument39 SeitenBangladesh BankAsadul HoqueNoch keine Bewertungen

- Problem Loan ManagementDokument13 SeitenProblem Loan ManagementAsadul HoqueNoch keine Bewertungen

- BB Focus WritingDokument28 SeitenBB Focus WritingAsadul HoqueNoch keine Bewertungen

- Role of Central Bank in BangladeshDokument20 SeitenRole of Central Bank in BangladeshAsadul HoqueNoch keine Bewertungen

- Bangladesh BankDokument16 SeitenBangladesh BankAsadul HoqueNoch keine Bewertungen

- ICMA Questions Dec 2011Dokument54 SeitenICMA Questions Dec 2011Asadul HoqueNoch keine Bewertungen

- Role of Central BankDokument32 SeitenRole of Central BankAsadul Hoque100% (3)

- Bangladesh Bank & Exim BankDokument58 SeitenBangladesh Bank & Exim BankAsadul HoqueNoch keine Bewertungen

- Principles of LendingDokument29 SeitenPrinciples of LendingAsadul HoqueNoch keine Bewertungen

- Principles of Problem Loan ManagementDokument22 SeitenPrinciples of Problem Loan ManagementAsadul Hoque100% (1)

- ICMA Questions Aug 2011Dokument57 SeitenICMA Questions Aug 2011Asadul Hoque100% (1)

- Form2a 1 Application Residential Other Minor - Catacutan Bldg.Dokument1 SeiteForm2a 1 Application Residential Other Minor - Catacutan Bldg.Karen MunozNoch keine Bewertungen

- Zuessy - TIMEDokument75 SeitenZuessy - TIMEcoupkoNoch keine Bewertungen

- AG - The Contract Management Benchmark Report, Sales Contracts - 200604Dokument26 SeitenAG - The Contract Management Benchmark Report, Sales Contracts - 200604Mounir100% (1)

- Economies of ScaleDokument15 SeitenEconomies of ScaleChandrasekhar BandaNoch keine Bewertungen

- Technological Services Ltd. TSL: Name Abbreviation Status Established Head OfficeDokument3 SeitenTechnological Services Ltd. TSL: Name Abbreviation Status Established Head OfficeTechnological ServicesNoch keine Bewertungen

- BS 2898Dokument16 SeitenBS 2898jiwani87Noch keine Bewertungen

- Biznet Technovillage BrochureDokument5 SeitenBiznet Technovillage BrochuregabriellaNoch keine Bewertungen

- Swink Chapter 1Dokument4 SeitenSwink Chapter 1Milo MinderbenderNoch keine Bewertungen

- Social Cost Benefit AnalysisDokument13 SeitenSocial Cost Benefit AnalysisMohammad Nayamat Ali Rubel100% (1)

- LaborDokument4 SeitenLaborVince LeidoNoch keine Bewertungen

- Boston Consulting Group Matrix (BCG Matrix)Dokument19 SeitenBoston Consulting Group Matrix (BCG Matrix)c-191786Noch keine Bewertungen

- Catchment AreaDokument3 SeitenCatchment AreaBaala MuraliNoch keine Bewertungen

- Soal EKONOMIDokument3 SeitenSoal EKONOMIIskandarIzulZulkarnainNoch keine Bewertungen

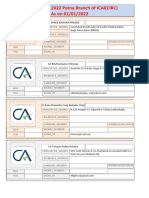

- E-Directory:: 2022 Patna Branch of ICAI (CIRC) As On 01/01/2022Dokument345 SeitenE-Directory:: 2022 Patna Branch of ICAI (CIRC) As On 01/01/2022Rekha MeghaniNoch keine Bewertungen

- Paypal Resolution PackageDokument46 SeitenPaypal Resolution PackageTavon LewisNoch keine Bewertungen

- The Kennedy Tree 2014Dokument9 SeitenThe Kennedy Tree 2014shaggypuppNoch keine Bewertungen

- Resume - Muhammad Aryzal Nuruzzaman - Production Planner Control & Production Process AnalystDokument2 SeitenResume - Muhammad Aryzal Nuruzzaman - Production Planner Control & Production Process AnalystAryzalNoch keine Bewertungen

- Stake Holder Analysis - ExxonmobilDokument8 SeitenStake Holder Analysis - Exxonmobilshalabhs4uNoch keine Bewertungen

- Project Management Professional (PMP) Training &NEWDokument792 SeitenProject Management Professional (PMP) Training &NEWAmer Rahmah100% (7)

- Final Gola Ganda Marketing PlanDokument40 SeitenFinal Gola Ganda Marketing PlansamiraZehra100% (3)

- Price List Scorpio NDokument1 SeitePrice List Scorpio NSHITESH KUMARNoch keine Bewertungen

- Indigo Flight Sample PDFDokument2 SeitenIndigo Flight Sample PDFRupam Dutta75% (4)

- Regional IntegrationDokument6 SeitenRegional IntegrationPeter DePointNoch keine Bewertungen

- Credit Application 2023Dokument1 SeiteCredit Application 2023Jean Pierre PerrierNoch keine Bewertungen

- J.P. Morgan Reiterates OREX With Overweight and $12 Price Target - May 8Dokument9 SeitenJ.P. Morgan Reiterates OREX With Overweight and $12 Price Target - May 8MayTepper100% (1)

- HabuDokument19 SeitenHabuEmie Delovino100% (2)

- Project FurnitureDokument29 SeitenProject FurnitureN sparklesNoch keine Bewertungen

- Problems and Solution 3Dokument6 SeitenProblems and Solution 3sachinremaNoch keine Bewertungen

- SLAuS 700 PDFDokument9 SeitenSLAuS 700 PDFnaveen pragash100% (1)

- Final DabbawalaDokument68 SeitenFinal DabbawalaVaishali MishraNoch keine Bewertungen