Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Tax Remedies Under The NircDokument41 SeitenTax Remedies Under The NircCecille BautistaNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Bautista BarExam3Dokument3 SeitenBautista BarExam3Cecille BautistaNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- 1977 Bar Exam Question and Answer By: Bautista, Cecille Loie GDokument3 Seiten1977 Bar Exam Question and Answer By: Bautista, Cecille Loie GCecille BautistaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Bautista BArexam4Dokument26 SeitenBautista BArexam4Cecille BautistaNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Corporation Law Digest PDFDokument152 SeitenCorporation Law Digest PDFCecille BautistaNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Bautista CaseDigest1Dokument1 SeiteBautista CaseDigest1Cecille BautistaNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Bautista Casedigest4Dokument6 SeitenBautista Casedigest4Cecille BautistaNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Consolidated Cases (Articles 10-11) PDFDokument138 SeitenConsolidated Cases (Articles 10-11) PDFCecille BautistaNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Yapyuco Vs Sandiganbayan 674 Scra 420Dokument4 SeitenYapyuco Vs Sandiganbayan 674 Scra 420Cecille Bautista100% (2)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Burgos vs. Macapagal Arroyo FACTS (2010 Case)Dokument2 SeitenBurgos vs. Macapagal Arroyo FACTS (2010 Case)Cecille BautistaNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Mullane VS. Central Hanover Bank and Trust CO. FactsDokument2 SeitenMullane VS. Central Hanover Bank and Trust CO. FactsCecille BautistaNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The 10 Biggest Fintech Companies in AmericaDokument5 SeitenThe 10 Biggest Fintech Companies in Americafly ALTNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Earnings Statement: Hilton Management Lane TN 38117 Lane TN 38117 LLC 755 Crossover MemphisDokument2 SeitenEarnings Statement: Hilton Management Lane TN 38117 Lane TN 38117 LLC 755 Crossover MemphisSelina González HerreraNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Gifts For Him - Etsy UKDokument1 SeiteGifts For Him - Etsy UKlily - roseNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Buckingham 68Dokument4 SeitenBuckingham 68JPNoch keine Bewertungen

- Annual Report 2007-2008 (ENG) - 20100603063436Dokument89 SeitenAnnual Report 2007-2008 (ENG) - 20100603063436Rakshya ShresthaNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- TABELA Condicionador - de - Ar - Split - Hi - WallDokument84 SeitenTABELA Condicionador - de - Ar - Split - Hi - WallPatoneleNoch keine Bewertungen

- Tax Cheat Sheet Exam 2 - CH 7,8,10,11Dokument2 SeitenTax Cheat Sheet Exam 2 - CH 7,8,10,11tyg1992Noch keine Bewertungen

- 230 Short Sale Packet - BayviewDokument16 Seiten230 Short Sale Packet - BayviewrapiddocsNoch keine Bewertungen

- Estimated Difference in Subsidies Between The AHCA and The ACA by Zip CodeDokument21 SeitenEstimated Difference in Subsidies Between The AHCA and The ACA by Zip CodeNorth Star Policy InstituteNoch keine Bewertungen

- Nasdaq 100 IndexDokument9 SeitenNasdaq 100 IndexRenu EsraniNoch keine Bewertungen

- Reindustrializing America: A Proposal For Reviving U.S. Manufacturing and Creating Millions of Good JobsDokument18 SeitenReindustrializing America: A Proposal For Reviving U.S. Manufacturing and Creating Millions of Good JobsMark S MarkNoch keine Bewertungen

- U.S. Individual Income Tax Return: Filing StatusDokument9 SeitenU.S. Individual Income Tax Return: Filing Statuswalessadone50% (2)

- Legit LLC Seller PermitDokument1 SeiteLegit LLC Seller PermitAly BenNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Resume of Srpeak4Dokument2 SeitenResume of Srpeak4api-25647173Noch keine Bewertungen

- IRS Pub 15 - 1988Dokument56 SeitenIRS Pub 15 - 1988cluetusNoch keine Bewertungen

- Sheria Pay CHK 04-12-2019 2 PDFDokument1 SeiteSheria Pay CHK 04-12-2019 2 PDFLynn JonesNoch keine Bewertungen

- 81601CP575Notice 1692149599160Dokument3 Seiten81601CP575Notice 1692149599160FGHJJ FDJFHDNoch keine Bewertungen

- Ten Mile Day-SummaryDokument1 SeiteTen Mile Day-SummaryPsic. Ó. Bernardo Duarte B.100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- United States TIN PDFDokument2 SeitenUnited States TIN PDFAldo Rodrigo AlgandonaNoch keine Bewertungen

- Understanding The ACA's Health Care ExchangesDokument10 SeitenUnderstanding The ACA's Health Care ExchangesMarketingRCANoch keine Bewertungen

- Election Form and Compensation Reduction Agreement: Sagitec Solutions LLCDokument2 SeitenElection Form and Compensation Reduction Agreement: Sagitec Solutions LLCFinding FannyNoch keine Bewertungen

- Dr. Jagdish BhagwatiDokument3 SeitenDr. Jagdish Bhagwatilotus9831Noch keine Bewertungen

- 2022 TaxReturnDokument6 Seiten2022 TaxReturnLALLOUS KHOURY100% (3)

- Form W-4Dokument4 SeitenForm W-4CNBC.comNoch keine Bewertungen

- Letter of Request - Tax ExemptionDokument1 SeiteLetter of Request - Tax ExemptionSinchan NurukiNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- s307 InglesDokument176 Seitens307 InglesAna M. RodriguezNoch keine Bewertungen

- Lyft 1099K 1239385631162661398 2019 PDFDokument1 SeiteLyft 1099K 1239385631162661398 2019 PDFJohn Matthew Cruel100% (1)

- CPA Exam Room Assignment May 2019Dokument22 SeitenCPA Exam Room Assignment May 2019Shei La MhaeNoch keine Bewertungen

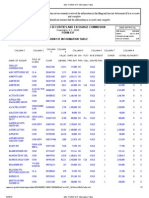

- SEC FORM 13-F Information TableDokument7 SeitenSEC FORM 13-F Information TableBecket AdamsNoch keine Bewertungen

- Why Bush Was So Bad at The End of His TermDokument2 SeitenWhy Bush Was So Bad at The End of His TermhcptombNoch keine Bewertungen