Das könnte Ihnen auch gefallen

- SDSSU-Tandag ES2011Dokument4 SeitenSDSSU-Tandag ES2011Chard BhotonzNoch keine Bewertungen

- Bulacan State University Executive Summary 2017Dokument9 SeitenBulacan State University Executive Summary 2017Esther Minnie JulianNoch keine Bewertungen

- Cotabato Foundation College of Science and Technology Executive Summary 2013Dokument4 SeitenCotabato Foundation College of Science and Technology Executive Summary 2013Calvin LeeNoch keine Bewertungen

- CHMSC-R6 Es2011 PDFDokument5 SeitenCHMSC-R6 Es2011 PDFMaria Cristine D. AbsulioNoch keine Bewertungen

- VInceDokument3 SeitenVIncenathalie nathalieNoch keine Bewertungen

- Executive Summary: Municipality of Sta. MonicaDokument6 SeitenExecutive Summary: Municipality of Sta. MonicaGenevieve TersolNoch keine Bewertungen

- DepEd Financial Management Objective and Framework 1Dokument23 SeitenDepEd Financial Management Objective and Framework 1EDONNANoch keine Bewertungen

- Executive Summary: Government EquityDokument5 SeitenExecutive Summary: Government EquityIAS City of Sto TomasNoch keine Bewertungen

- San Agustin Executive Summary 2016Dokument7 SeitenSan Agustin Executive Summary 2016Ma. Danice Angela Balde-BarcomaNoch keine Bewertungen

- Special Provisions of GAA FY 2020 (R.A. No. 11465)Dokument2 SeitenSpecial Provisions of GAA FY 2020 (R.A. No. 11465)Kaitou KurobaNoch keine Bewertungen

- Philippine Reclamation Authority Executive Summary 2020Dokument4 SeitenPhilippine Reclamation Authority Executive Summary 2020frustratedlawstudentNoch keine Bewertungen

- Executive Summary: 2016 Gawad Pilipino Dangal NG Husay at Galing As Outstanding Educator of TheDokument6 SeitenExecutive Summary: 2016 Gawad Pilipino Dangal NG Husay at Galing As Outstanding Educator of Thejaymark camachoNoch keine Bewertungen

- 31btpartmtnt of Qebucation: L/epublit of Tbe .TlbilippineDokument5 Seiten31btpartmtnt of Qebucation: L/epublit of Tbe .TlbilippineDarwin AbesNoch keine Bewertungen

- Cindy M. Doria: Reaction PaperDokument4 SeitenCindy M. Doria: Reaction PaperLOWIE ATCHASONoch keine Bewertungen

- Sablayan Executive Summary 2016Dokument5 SeitenSablayan Executive Summary 2016Leo M. SalibioNoch keine Bewertungen

- Miag-Ao Iloilo ES2014Dokument5 SeitenMiag-Ao Iloilo ES2014Roi Baltazar BaylenNoch keine Bewertungen

- Pge 22-23Dokument9 SeitenPge 22-23ipncastillejaNoch keine Bewertungen

- Sipocot Executive Summary 2012Dokument6 SeitenSipocot Executive Summary 2012Tintin N. XiaoNoch keine Bewertungen

- Dolores Executive Summary 2013Dokument6 SeitenDolores Executive Summary 2013Lyrics DistrictNoch keine Bewertungen

- SAS Sample PolicyDokument5 SeitenSAS Sample PolicyGielynn Dave Bagsican Cloma-KatipunanNoch keine Bewertungen

- Ordinance Affirming Pateros TechnologicalDokument4 SeitenOrdinance Affirming Pateros TechnologicalJustin SanchoNoch keine Bewertungen

- All India Council For Technical EducationDokument31 SeitenAll India Council For Technical EducationSkillytek ServiceNoch keine Bewertungen

- Prosperidad ADS ES2016Dokument66 SeitenProsperidad ADS ES2016J JaNoch keine Bewertungen

- Malay Executive Summary 2017Dokument7 SeitenMalay Executive Summary 2017RM Rea RebNoch keine Bewertungen

- Mga Tao Sa KapehanDokument4 SeitenMga Tao Sa KapehanJoshua Lavega AbrinaNoch keine Bewertungen

- Josefina Executive Summary 2017Dokument8 SeitenJosefina Executive Summary 2017Virgo Philip Wasil ButconNoch keine Bewertungen

- Roxas Isabela ES2016Dokument4 SeitenRoxas Isabela ES2016J JaNoch keine Bewertungen

- Resource For Term PaperDokument5 SeitenResource For Term Paperasus7thgenNoch keine Bewertungen

- BinalonanWD-R1 ES2018Dokument4 SeitenBinalonanWD-R1 ES2018J JaNoch keine Bewertungen

- Abuki HRM Case StudyDokument14 SeitenAbuki HRM Case Studyabubeker negesaNoch keine Bewertungen

- San Miguel Executive Summary 2013Dokument7 SeitenSan Miguel Executive Summary 2013SharaJaenDinorogBagundolNoch keine Bewertungen

- Department of Information and Communications Technology Executive Summary 2016Dokument5 SeitenDepartment of Information and Communications Technology Executive Summary 2016Andrea-Gayle CoNoch keine Bewertungen

- La Paz Executive Summary 2019Dokument10 SeitenLa Paz Executive Summary 2019Rene BalloNoch keine Bewertungen

- Approved Financial ProceeduresDokument86 SeitenApproved Financial ProceeduresTebello Offney MabokaNoch keine Bewertungen

- 1449293287189medical Dental Guidelines 2016-17 To 2018-19 PDFDokument4 Seiten1449293287189medical Dental Guidelines 2016-17 To 2018-19 PDFVenkata Nagaraj MummadisettyNoch keine Bewertungen

- Moalboal Executive Summary 2014Dokument6 SeitenMoalboal Executive Summary 2014Horace CimafrancaNoch keine Bewertungen

- Commission On Audit Circular No. 2000-002: April 4, 2000Dokument3 SeitenCommission On Audit Circular No. 2000-002: April 4, 2000bolNoch keine Bewertungen

- Certificacion Js 2011-2012 15Dokument12 SeitenCertificacion Js 2011-2012 15marioNoch keine Bewertungen

- Bicol State College of Applied Sciences and Technology: (With Comparative Figures For CY 2017)Dokument14 SeitenBicol State College of Applied Sciences and Technology: (With Comparative Figures For CY 2017)jaymark camachoNoch keine Bewertungen

- Deputy Accounts Officer (DAO) Job Description C.V. Raman Global University, Bhubaneswar, OdishaDokument6 SeitenDeputy Accounts Officer (DAO) Job Description C.V. Raman Global University, Bhubaneswar, OdishauppaliNoch keine Bewertungen

- Guidelines For Study LeaveDokument2 SeitenGuidelines For Study LeaveLeroyNoch keine Bewertungen

- The Budget ProcessDokument86 SeitenThe Budget ProcessLeah Dianne SegunialNoch keine Bewertungen

- Umingan Pangasinan ES2013Dokument10 SeitenUmingan Pangasinan ES2013J JaNoch keine Bewertungen

- Kalayaan Executive Summary 2014Dokument6 SeitenKalayaan Executive Summary 2014Aira Kathrina PerezNoch keine Bewertungen

- Oton Executive Summary 2017Dokument5 SeitenOton Executive Summary 2017Franz FulhamNoch keine Bewertungen

- Guimbal Executive Summary 2013Dokument5 SeitenGuimbal Executive Summary 2013Jan M.Noch keine Bewertungen

- Executive SummaryDokument5 SeitenExecutive SummaryDanica GodornesNoch keine Bewertungen

- Quezon Executive Summary 2021 PDFDokument4 SeitenQuezon Executive Summary 2021 PDFEsnar de Castro Jr.Noch keine Bewertungen

- Iligan City Executive Summary 2016Dokument11 SeitenIligan City Executive Summary 2016crizeljane.enayudaNoch keine Bewertungen

- On Hazard Pay - bacoorFinanceTeamDokument10 SeitenOn Hazard Pay - bacoorFinanceTeamRoger DrioNoch keine Bewertungen

- 04-KalingaProvince2018 Executive SummaryDokument7 Seiten04-KalingaProvince2018 Executive SummaryMarcus SalvateroNoch keine Bewertungen

- WBUT Affiliation Process PDFDokument62 SeitenWBUT Affiliation Process PDFAniruddha GuptaNoch keine Bewertungen

- Employees Retension in Tanzania Public Educational Institutions: Educational Business Study Case of Tanzania Public Service College (TPSC)Dokument8 SeitenEmployees Retension in Tanzania Public Educational Institutions: Educational Business Study Case of Tanzania Public Service College (TPSC)International Journal of Innovative Science and Research TechnologyNoch keine Bewertungen

- Uyugan Executive Summary 2013Dokument5 SeitenUyugan Executive Summary 2013arlyne velayoNoch keine Bewertungen

- Rizal Executive Summary 2015Dokument4 SeitenRizal Executive Summary 2015Sittie RahmaNoch keine Bewertungen

- Mandatory Expenses: Presented By: Cheryl M. AsiaDokument19 SeitenMandatory Expenses: Presented By: Cheryl M. AsiaAdrian PanganNoch keine Bewertungen

- Executive Summary: in Thousands of PesosDokument6 SeitenExecutive Summary: in Thousands of PesosDAS MAGNoch keine Bewertungen

- Bureau of Fisheries and Aquatic Resources Executive Summary 2017Dokument9 SeitenBureau of Fisheries and Aquatic Resources Executive Summary 2017Kikz GusiNoch keine Bewertungen

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanVon EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNoch keine Bewertungen

- Financial Reporting under IFRS: A Topic Based ApproachVon EverandFinancial Reporting under IFRS: A Topic Based ApproachNoch keine Bewertungen

- WWWDokument6 SeitenWWWjaymark camachoNoch keine Bewertungen

- WWWDokument6 SeitenWWWjaymark camachoNoch keine Bewertungen

- Electrical Power Subsystem - v2Dokument63 SeitenElectrical Power Subsystem - v2jaymark camachoNoch keine Bewertungen

- Diego SilangDokument1 SeiteDiego Silangjaymark camachoNoch keine Bewertungen

- Electrical Safety and Electromagnetic CompatibilityDokument25 SeitenElectrical Safety and Electromagnetic Compatibilityjaymark camachoNoch keine Bewertungen

- VDokument16 SeitenVjaymark camachoNoch keine Bewertungen

- Commission On Audit Audit Team 4, Ngs-Sucs Bicol State College of Applied Sciences and Technology Naga CityDokument2 SeitenCommission On Audit Audit Team 4, Ngs-Sucs Bicol State College of Applied Sciences and Technology Naga Cityjaymark camachoNoch keine Bewertungen

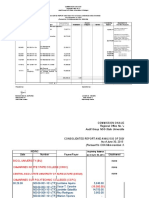

- Denomination Petty Cash Total Denomination PCF Gasoline PCF - Regular PCF - RM CH - No. 1889647 CH - No.694942 CH - No. 1867776 CH - No.1867778Dokument2 SeitenDenomination Petty Cash Total Denomination PCF Gasoline PCF - Regular PCF - RM CH - No. 1889647 CH - No.694942 CH - No. 1867776 CH - No.1867778jaymark camachoNoch keine Bewertungen

- Other Payables 2018Dokument19 SeitenOther Payables 2018jaymark camachoNoch keine Bewertungen

- January 2018 OR'S Febuary 2018 OR'SDokument21 SeitenJanuary 2018 OR'S Febuary 2018 OR'Sjaymark camachoNoch keine Bewertungen

- 02-PSU2016 Transmittal Letter To Board Of-RegentsDokument2 Seiten02-PSU2016 Transmittal Letter To Board Of-Regentsjaymark camachoNoch keine Bewertungen

- Commission On Audit Audit Team 4, Ngs-Sucs Bicol State College of Applied Sciences and Technology Naga CityDokument2 SeitenCommission On Audit Audit Team 4, Ngs-Sucs Bicol State College of Applied Sciences and Technology Naga Cityjaymark camachoNoch keine Bewertungen

- I.Settlement Patterns: A Settlement Pattern Means The Shape of A SettlementDokument5 SeitenI.Settlement Patterns: A Settlement Pattern Means The Shape of A Settlementjaymark camachoNoch keine Bewertungen

- Remittance Vs PayrollDokument2 SeitenRemittance Vs Payrolljaymark camachoNoch keine Bewertungen

- Purchase OrderDokument4 SeitenPurchase Orderjaymark camachoNoch keine Bewertungen

- Pangasinan State University: Republic of The PhilippinesDokument1 SeitePangasinan State University: Republic of The Philippinesjaymark camachoNoch keine Bewertungen

- Notes To Financial Statements ReferenceDokument32 SeitenNotes To Financial Statements Referencejaymark camachoNoch keine Bewertungen

- Observations and Recommendations: I. Financial and ComplianceDokument20 SeitenObservations and Recommendations: I. Financial and Compliancejaymark camachoNoch keine Bewertungen

- 11 PSU2016 - Part1 FSDokument664 Seiten11 PSU2016 - Part1 FSjaymark camachoNoch keine Bewertungen

- 14-PSU2016 Part3-Status of PYs RecommDokument16 Seiten14-PSU2016 Part3-Status of PYs Recommjaymark camachoNoch keine Bewertungen

- 08-PSU2016 FlyleavesDokument3 Seiten08-PSU2016 Flyleavesjaymark camachoNoch keine Bewertungen

- 03-PSU2016 Transmittal Letter To The PresidentDokument2 Seiten03-PSU2016 Transmittal Letter To The Presidentjaymark camachoNoch keine Bewertungen

- ESAP CB PR CB - Sample PDFDokument14 SeitenESAP CB PR CB - Sample PDFAdiyasa WardanaNoch keine Bewertungen

- Quiz Chapter 1 - AnswersDokument21 SeitenQuiz Chapter 1 - Answersbobbybobsmith12345Noch keine Bewertungen

- 4 - Case Study - The IMF and Ukraine's Economic CrisisDokument2 Seiten4 - Case Study - The IMF and Ukraine's Economic CrisisAhmerNoch keine Bewertungen

- The New Economic Geography Theory by Paul Krugman and Our Proposed Economic TheoryDokument36 SeitenThe New Economic Geography Theory by Paul Krugman and Our Proposed Economic TheoryEulalio NinaNoch keine Bewertungen

- BUS 2201 Principles of Marketing Unit 2 DADokument5 SeitenBUS 2201 Principles of Marketing Unit 2 DAMamu KamNoch keine Bewertungen

- ASSIGNMENTDokument3 SeitenASSIGNMENThusna harunaNoch keine Bewertungen

- Travel and Expense Policy Asia Pacific Addendum - 2016 Global - July2016Dokument46 SeitenTravel and Expense Policy Asia Pacific Addendum - 2016 Global - July2016HARENDRA SINGH BishtNoch keine Bewertungen

- Accounting 9 DCF ModelDokument1 SeiteAccounting 9 DCF ModelRica CatanguiNoch keine Bewertungen

- Labor Laws and CooperativeDokument11 SeitenLabor Laws and CooperativeMa Socorro U. MarquezNoch keine Bewertungen

- Rural Marketing FMCG Product Hindustan Unilever Limited: Master of Business Administration (MBA) Session 2019-20Dokument6 SeitenRural Marketing FMCG Product Hindustan Unilever Limited: Master of Business Administration (MBA) Session 2019-20Amit SinghNoch keine Bewertungen

- Chapter Four Payroll in ETHDokument11 SeitenChapter Four Payroll in ETHMiki AberaNoch keine Bewertungen

- Valley Bread IncDokument29 SeitenValley Bread IncMae Richelle D. DacaraNoch keine Bewertungen

- Akash Tiwari - 4 Year(s) 0 Month(s)Dokument4 SeitenAkash Tiwari - 4 Year(s) 0 Month(s)22827351Noch keine Bewertungen

- Digitalize Indonesia 2019 1 Siemens Smart InfrastructureDokument7 SeitenDigitalize Indonesia 2019 1 Siemens Smart InfrastructureronisusantoNoch keine Bewertungen

- PPT-Performance AppraisalDokument56 SeitenPPT-Performance Appraisalshiiba2287% (84)

- Part 1: 1-2 Terminology For Six Month Merchandise PlanDokument3 SeitenPart 1: 1-2 Terminology For Six Month Merchandise PlansiewspahNoch keine Bewertungen

- Financial Statement AnalysisDokument12 SeitenFinancial Statement AnalysisGail0% (1)

- Chap3 Market Opportunity Analysis and Consumer AnalysisDokument53 SeitenChap3 Market Opportunity Analysis and Consumer Analysisrachel100% (3)

- RESPONSIBILITY ACCOUNTING - A System of Accounting Wherein Performance, Based OnDokument8 SeitenRESPONSIBILITY ACCOUNTING - A System of Accounting Wherein Performance, Based OnHarvey AguilarNoch keine Bewertungen

- Company First Name Last Name Job TitleDokument35 SeitenCompany First Name Last Name Job Titleethanhunt3747Noch keine Bewertungen

- 06 Task PerformanceDokument2 Seiten06 Task PerformanceKatherine Borja67% (3)

- LISA Transfer Authority Form PDFDokument2 SeitenLISA Transfer Authority Form PDFAnonymous lHIUIweVNoch keine Bewertungen

- AN - ARCHITECTURE - GUIDE - Vol 2Dokument137 SeitenAN - ARCHITECTURE - GUIDE - Vol 2EL100% (1)

- Unit 3 - Security AnalysisDokument33 SeitenUnit 3 - Security AnalysisWasim DalviNoch keine Bewertungen

- Kotler Pom17e PPT 03Dokument28 SeitenKotler Pom17e PPT 03Trâm Anh BảoNoch keine Bewertungen

- Mergers & Acquisitions: Master in Management - Investment BankingDokument21 SeitenMergers & Acquisitions: Master in Management - Investment Bankingisaure badreNoch keine Bewertungen

- CIMB-i - CMP-Murabahah Facility-Agreement - FixedVariable-or-Variable - Eng PDFDokument65 SeitenCIMB-i - CMP-Murabahah Facility-Agreement - FixedVariable-or-Variable - Eng PDFBannupriya VeleysamyNoch keine Bewertungen

- Final Internship ReportDokument46 SeitenFinal Internship ReportwaseemNoch keine Bewertungen

- LEAN Production or Lean Manufacturing or Toyota Production System (TPS) - Doing More With Less (Free Business E-Coach)Dokument4 SeitenLEAN Production or Lean Manufacturing or Toyota Production System (TPS) - Doing More With Less (Free Business E-Coach)Amanpreet Singh AroraNoch keine Bewertungen

- Addis Ababa UniversityDokument6 SeitenAddis Ababa UniversityBereket KassahunNoch keine Bewertungen