Das könnte Ihnen auch gefallen

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsVon EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNoch keine Bewertungen

- F M ADokument11 SeitenF M AAjay SahooNoch keine Bewertungen

- ExerciseDokument12 SeitenExercisesde.ofcl20Noch keine Bewertungen

- Yearly Ledger Changes: AssetsDokument8 SeitenYearly Ledger Changes: AssetsMiguel OrjuelaNoch keine Bewertungen

- Chapter 1 - Some Solved ProblemsDokument12 SeitenChapter 1 - Some Solved ProblemsBracu 2023Noch keine Bewertungen

- Asynchronous Statement of Financial Position XYZ CompanyDokument5 SeitenAsynchronous Statement of Financial Position XYZ CompanyDiana Fernandez MagnoNoch keine Bewertungen

- Practice Problems2Dokument48 SeitenPractice Problems2vipinkala1100% (1)

- Final AccountDokument7 SeitenFinal Accountswati100% (3)

- Penjabaran Lap Kaungan DLM Mata Uang Asing 2Dokument17 SeitenPenjabaran Lap Kaungan DLM Mata Uang Asing 2Muhammad TaufiqNoch keine Bewertungen

- Ujian 1 AdvDokument33 SeitenUjian 1 AdvaraNoch keine Bewertungen

- Assignment LDokument6 SeitenAssignment Lphprcffj2rNoch keine Bewertungen

- Additional InformationDokument7 SeitenAdditional InformationvasanthgurusamynsNoch keine Bewertungen

- CSS Ratio AnalysisDokument9 SeitenCSS Ratio AnalysisMasood Ahmad AadamNoch keine Bewertungen

- LQ3 FinalDokument6 SeitenLQ3 FinalRaz MahariNoch keine Bewertungen

- Presentation 1Dokument2 SeitenPresentation 1apolsoftNoch keine Bewertungen

- 5.ratio Analysis SumsDokument9 Seiten5.ratio Analysis Sumsvinay kumar nuwalNoch keine Bewertungen

- Final Account, Income Statement and Financial Analysis Practice QuestionsDokument36 SeitenFinal Account, Income Statement and Financial Analysis Practice QuestionsMansi GoelNoch keine Bewertungen

- Forex Translation Computational: Total P564,000Dokument6 SeitenForex Translation Computational: Total P564,000Elizabeth DumawalNoch keine Bewertungen

- Balance Sheet: Income StatementDokument6 SeitenBalance Sheet: Income StatementNiaz ShaikhNoch keine Bewertungen

- Answers To CH 2 - FTW ProblemsDokument14 SeitenAnswers To CH 2 - FTW ProblemsJuanito Jr. LagnoNoch keine Bewertungen

- Assignment 2Dokument3 SeitenAssignment 2Joe MajchrzakNoch keine Bewertungen

- Net Working Capital Current Assets - Current LiabilitiesDokument11 SeitenNet Working Capital Current Assets - Current LiabilitiesRahul YadavNoch keine Bewertungen

- Finding Operating and Free Cash FlowsDokument5 SeitenFinding Operating and Free Cash FlowsM.TalhaNoch keine Bewertungen

- Liquidity RatiosDokument3 SeitenLiquidity RatiosMckenzie PalaganasNoch keine Bewertungen

- Case 3 FS AnalysisDokument1 SeiteCase 3 FS AnalysisCABAHM San Sebastian CaviteNoch keine Bewertungen

- Transactions - Year 2015Dokument23 SeitenTransactions - Year 2015raeq109Noch keine Bewertungen

- Paper - 1: AccountingDokument18 SeitenPaper - 1: AccountingJerry HuffmanNoch keine Bewertungen

- Transaction Analysis Janelle'SRESTAURANTDokument2 SeitenTransaction Analysis Janelle'SRESTAURANTReana ReyesNoch keine Bewertungen

- WP - Forex Practice SetDokument8 SeitenWP - Forex Practice SetJester LimNoch keine Bewertungen

- Unit 3Dokument13 SeitenUnit 3hassan19951996hNoch keine Bewertungen

- Cash Flow Statement Problems PDFDokument32 SeitenCash Flow Statement Problems PDFnsrivastav180% (30)

- Financial Statements AnalysisDokument1 SeiteFinancial Statements AnalysisDELA CRUZ Jesseca V.Noch keine Bewertungen

- Hec Wood Ratio Analysis Input Worksheet 2/13/2012Dokument6 SeitenHec Wood Ratio Analysis Input Worksheet 2/13/2012Michael HakimNoch keine Bewertungen

- Study Unit Three Activity Ratios and Special IssuesDokument11 SeitenStudy Unit Three Activity Ratios and Special IssuessimarjeetNoch keine Bewertungen

- Cost Model Skeletal Approach Ans KeysDokument4 SeitenCost Model Skeletal Approach Ans KeysMelvin BagasinNoch keine Bewertungen

- Intermediate Accounting 3 - SolutionsDokument3 SeitenIntermediate Accounting 3 - Solutionssammie helsonNoch keine Bewertungen

- Balance Sheet: Assets DebtsDokument95 SeitenBalance Sheet: Assets DebtsThai VuNoch keine Bewertungen

- Accounting AssignmentDokument5 SeitenAccounting AssignmentVivek SinghNoch keine Bewertungen

- P4-12 AnswerDokument5 SeitenP4-12 AnswerPutri Apriliana100% (1)

- Dian Sari (A031171703) Tugas Akl IiDokument3 SeitenDian Sari (A031171703) Tugas Akl Iidian sariNoch keine Bewertungen

- Use The Following Information To Answer Items 5 - 7Dokument4 SeitenUse The Following Information To Answer Items 5 - 7acctg2012Noch keine Bewertungen

- Abaynesh Abate Advanced Financial AccountingDokument7 SeitenAbaynesh Abate Advanced Financial Accountingሔርሞን ይድነቃቸውNoch keine Bewertungen

- Quiz 02 Subsequent To Acquisition DateDokument1 SeiteQuiz 02 Subsequent To Acquisition DateErjohn PapaNoch keine Bewertungen

- Cash in Bank Accounts Receivable Kitchen Supplies Equipment Furniture & Fixtures No. AssetsDokument3 SeitenCash in Bank Accounts Receivable Kitchen Supplies Equipment Furniture & Fixtures No. AssetsJones Flores GuerreroNoch keine Bewertungen

- Corporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Dokument9 SeitenCorporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Eunice NanaNoch keine Bewertungen

- NPO SolutionsDokument6 SeitenNPO Solutionswhoaskedx69Noch keine Bewertungen

- Latihan Aklan 2 Lab UTSDokument10 SeitenLatihan Aklan 2 Lab UTSpermataayu31Noch keine Bewertungen

- GPV & SCF (Assignment)Dokument16 SeitenGPV & SCF (Assignment)Mica Moreen GuillermoNoch keine Bewertungen

- MAS ExerciseDokument9 SeitenMAS ExerciseAlaine Milka GosycoNoch keine Bewertungen

- Contoh Akuisisi 100% Dan 100% Metode Cost (Tan Lee)Dokument10 SeitenContoh Akuisisi 100% Dan 100% Metode Cost (Tan Lee)Kusnul WidiyaniNoch keine Bewertungen

- P3.5 Different Forms of Business CombinationDokument8 SeitenP3.5 Different Forms of Business CombinationAgnes CahyaNoch keine Bewertungen

- Mids Excel WorkDokument2 SeitenMids Excel WorkMuhammad EhtishamNoch keine Bewertungen

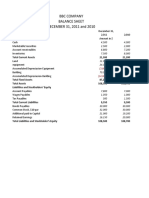

- BBC Company Balance Sheet DECEMBER 31, 2011 and 2010: AssetsDokument2 SeitenBBC Company Balance Sheet DECEMBER 31, 2011 and 2010: AssetsMuhammad EhtishamNoch keine Bewertungen

- Measures of Leverage: Abhishek SinhaDokument30 SeitenMeasures of Leverage: Abhishek Sinhadev guptaNoch keine Bewertungen

- Auditing Problem Quiz 2 Long Problem SolutionsDokument7 SeitenAuditing Problem Quiz 2 Long Problem Solutionsreina maica terradoNoch keine Bewertungen

- CHATTO - Finals - Summer 2022 - Cash Flows & Cap. BudgDokument6 SeitenCHATTO - Finals - Summer 2022 - Cash Flows & Cap. BudgJULLIE CARMELLE H. CHATTONoch keine Bewertungen

- Comparative Income StatementDokument12 SeitenComparative Income StatementBISHAL ROYNoch keine Bewertungen

- PR AKLII Bab 14 Dan 15 Sarah Puspita Anggraini (411796)Dokument15 SeitenPR AKLII Bab 14 Dan 15 Sarah Puspita Anggraini (411796)Satrio Saja67% (3)

- Chapter 15 - Capital BudgetiDokument66 SeitenChapter 15 - Capital BudgetiAnonymous qi4PZk0% (1)

- MCQ With AnswersDokument27 SeitenMCQ With AnswersAnonymous qi4PZkNoch keine Bewertungen

- TEST BANK-Auditing-ECDokument16 SeitenTEST BANK-Auditing-ECAnonymous qi4PZkNoch keine Bewertungen

- Chapter 34Dokument17 SeitenChapter 34Anonymous qi4PZkNoch keine Bewertungen

- For FDPB Posting-RizalDokument12 SeitenFor FDPB Posting-RizalMarieta AlejoNoch keine Bewertungen

- AMUL'S Every Function Involves Huge Human ResourcesDokument3 SeitenAMUL'S Every Function Involves Huge Human ResourcesRitu RajNoch keine Bewertungen

- Cat Hydo 10wDokument4 SeitenCat Hydo 10wWilbort Encomenderos RuizNoch keine Bewertungen

- Walt Whitman Video Worksheet. CompletedDokument1 SeiteWalt Whitman Video Worksheet. CompletedelizabethannelangehennigNoch keine Bewertungen

- A Practical Guide To Transfer Pricing Policy Design and ImplementationDokument11 SeitenA Practical Guide To Transfer Pricing Policy Design and ImplementationQiujun LiNoch keine Bewertungen

- Barangay AppointmentDokument2 SeitenBarangay AppointmentArlyn Gumahad CahanapNoch keine Bewertungen

- Placement TestDokument6 SeitenPlacement TestNovia YunitazamiNoch keine Bewertungen

- PropertycasesforfinalsDokument40 SeitenPropertycasesforfinalsRyan Christian LuposNoch keine Bewertungen

- Pigeon Racing PigeonDokument7 SeitenPigeon Racing Pigeonsundarhicet83Noch keine Bewertungen

- FCAPSDokument5 SeitenFCAPSPablo ParreñoNoch keine Bewertungen

- Emma The Easter BunnyDokument9 SeitenEmma The Easter BunnymagdaNoch keine Bewertungen

- Filehost - CIA - Mind Control Techniques - (Ebook 197602 .TXT) (TEC@NZ)Dokument52 SeitenFilehost - CIA - Mind Control Techniques - (Ebook 197602 .TXT) (TEC@NZ)razvan_9100% (1)

- ch-1 NewDokument11 Seitench-1 NewSAKIB MD SHAFIUDDINNoch keine Bewertungen

- 19-Microendoscopic Lumbar DiscectomyDokument8 Seiten19-Microendoscopic Lumbar DiscectomyNewton IssacNoch keine Bewertungen

- ENTRAPRENEURSHIPDokument29 SeitenENTRAPRENEURSHIPTanmay Mukherjee100% (1)

- Annual Report Aneka Tambang Antam 2015Dokument670 SeitenAnnual Report Aneka Tambang Antam 2015Yustiar GunawanNoch keine Bewertungen

- Frbiblio PDFDokument16 SeitenFrbiblio PDFreolox100% (1)

- Economics and Agricultural EconomicsDokument28 SeitenEconomics and Agricultural EconomicsM Hossain AliNoch keine Bewertungen

- Company Profile ESB Update May 2021 Ver 1Dokument9 SeitenCompany Profile ESB Update May 2021 Ver 1Nakaturi CoffeeNoch keine Bewertungen

- DH 0507Dokument12 SeitenDH 0507The Delphos HeraldNoch keine Bewertungen

- Landslide Hazard Manual: Trainer S HandbookDokument32 SeitenLandslide Hazard Manual: Trainer S HandbookMouhammed AbdallahNoch keine Bewertungen

- Dumont's Theory of Caste.Dokument4 SeitenDumont's Theory of Caste.Vikram Viner50% (2)

- Chemistry InvestigatoryDokument16 SeitenChemistry InvestigatoryVedant LadheNoch keine Bewertungen

- Foundations For Assisting in Home Care 1520419723Dokument349 SeitenFoundations For Assisting in Home Care 1520419723amasrurNoch keine Bewertungen

- OPSS 415 Feb90Dokument7 SeitenOPSS 415 Feb90Muhammad UmarNoch keine Bewertungen

- GooseberriesDokument10 SeitenGooseberriesmoobin.jolfaNoch keine Bewertungen

- Delegated Legislation in India: Submitted ToDokument15 SeitenDelegated Legislation in India: Submitted ToRuqaiyaNoch keine Bewertungen

- English 10-Dll-Week 3Dokument5 SeitenEnglish 10-Dll-Week 3Alyssa Grace Dela TorreNoch keine Bewertungen

- Community Service Learning IdeasDokument4 SeitenCommunity Service Learning IdeasMuneeb ZafarNoch keine Bewertungen

- Academic Decathlon FlyerDokument3 SeitenAcademic Decathlon FlyerNjeri GachNoch keine Bewertungen