Das könnte Ihnen auch gefallen

- Case Study Chapter 2Dokument1 SeiteCase Study Chapter 2Sceisa ScalaNoch keine Bewertungen

- Developing A Business CaseDokument10 SeitenDeveloping A Business CaseRuthNoch keine Bewertungen

- Patrickflood Dasa Assignments For EportfolioDokument8 SeitenPatrickflood Dasa Assignments For Eportfolioapi-323245411100% (5)

- Williamsport Hospital - Group Report Ver2Dokument3 SeitenWilliamsport Hospital - Group Report Ver2Ameya Pandit100% (1)

- Break-Even AnalysisDokument16 SeitenBreak-Even AnalysisRabena, Vinny Emmanuel T.Noch keine Bewertungen

- Croswell University HospitalDokument6 SeitenCroswell University HospitalIvander LatumetenNoch keine Bewertungen

- Should Physicians Be Allowed To Balance BillDokument20 SeitenShould Physicians Be Allowed To Balance BillVISHNU PandurangaduNoch keine Bewertungen

- Audit of Endotracheal Tube Suction in A Pediatric Intensive Care UnitDokument14 SeitenAudit of Endotracheal Tube Suction in A Pediatric Intensive Care UnitJuan SlaxNoch keine Bewertungen

- Census Report 2017: Program Anestisiologi Kementerian Kesihatan MalaysiaDokument47 SeitenCensus Report 2017: Program Anestisiologi Kementerian Kesihatan MalaysiaKino GaoNoch keine Bewertungen

- FSRH Guideline Emergency Contraception03dec2020 Amendedjuly2023 11julDokument68 SeitenFSRH Guideline Emergency Contraception03dec2020 Amendedjuly2023 11julmirunahorgaNoch keine Bewertungen

- JOAN 2019 BC UltrasoundDokument5 SeitenJOAN 2019 BC UltrasoundnzsargaziNoch keine Bewertungen

- FSRH Guideline Emergency Contraception03dec2020Dokument68 SeitenFSRH Guideline Emergency Contraception03dec2020soumyaydvNoch keine Bewertungen

- Medical & Dental Course Details - JIPMER PuducherryDokument2 SeitenMedical & Dental Course Details - JIPMER Puducherrykaran210997Noch keine Bewertungen

- European J of Heart Fail - 2019 - Verbrugge - Acetazolamide To Increase Natriuresis in Congestive Heart Failure at HighDokument8 SeitenEuropean J of Heart Fail - 2019 - Verbrugge - Acetazolamide To Increase Natriuresis in Congestive Heart Failure at HighAnnisa Tria FadillaNoch keine Bewertungen

- International Journal of Nursing and Health Services (IJNHS)Dokument7 SeitenInternational Journal of Nursing and Health Services (IJNHS)Dy RPNoch keine Bewertungen

- 2021 TDC Module Case Analysis GuidelinesDokument5 Seiten2021 TDC Module Case Analysis GuidelinesLeuqcar Ramos DonascoNoch keine Bewertungen

- MSG83 Epidural Analgesia in Labour PDFDokument18 SeitenMSG83 Epidural Analgesia in Labour PDFGrigore PopaNoch keine Bewertungen

- Excision of Endometriosis - OptimisingDokument8 SeitenExcision of Endometriosis - OptimisingRania AHNoch keine Bewertungen

- Issue 6Dokument8 SeitenIssue 6Deepak AgrawalNoch keine Bewertungen

- Jebah Hospital: The Crimson Press Curriculum Center The Crimson Group, IncDokument8 SeitenJebah Hospital: The Crimson Press Curriculum Center The Crimson Group, IncLian EspinoNoch keine Bewertungen

- Anorectal MalformationDokument17 SeitenAnorectal MalformationSilvester SikoraNoch keine Bewertungen

- Checklist For Esic/Esis HospitalsDokument6 SeitenChecklist For Esic/Esis HospitalssureesicNoch keine Bewertungen

- Evaluation of The Effect of Submucosal Vaginal Administration of Ketamine On Postoperative Pain in Ivf CandidatesDokument10 SeitenEvaluation of The Effect of Submucosal Vaginal Administration of Ketamine On Postoperative Pain in Ivf Candidatesindex PubNoch keine Bewertungen

- EsteticaDokument10 SeitenEsteticaMichele CarvalhoNoch keine Bewertungen

- Evaluating The Level of Pain During Office Hysteroscopy According To Menopausal Status, Parity, and Size of InstrumentDokument4 SeitenEvaluating The Level of Pain During Office Hysteroscopy According To Menopausal Status, Parity, and Size of InstrumentMaqsoodUlHassanChaudharyNoch keine Bewertungen

- Patient Functional Independence and Occupational Therapist Time-Use in Inpatient Services: Patient Demographic and Clinical CorrelatesDokument10 SeitenPatient Functional Independence and Occupational Therapist Time-Use in Inpatient Services: Patient Demographic and Clinical CorrelatesNataliaNoch keine Bewertungen

- Casemix and Information Systems: Health InformaticsDokument24 SeitenCasemix and Information Systems: Health InformaticsAchmad yudi ArifiyantoNoch keine Bewertungen

- Block Time Table For 2018 Batch (12.07.2021 To 31.07.2021)Dokument3 SeitenBlock Time Table For 2018 Batch (12.07.2021 To 31.07.2021)Kuldeep KumarNoch keine Bewertungen

- B - Methotrexate in Ectopic PregnancyDokument5 SeitenB - Methotrexate in Ectopic PregnancypremiumidxNoch keine Bewertungen

- The Hot Topic Right Now in Our Department Is Adaptive PlanningDokument2 SeitenThe Hot Topic Right Now in Our Department Is Adaptive Planningapi-645453685Noch keine Bewertungen

- Impact of Treatment Planning Quality Assurance SoftwareDokument6 SeitenImpact of Treatment Planning Quality Assurance SoftwareMuhammad Rizqi ArdiansyahNoch keine Bewertungen

- WHO - NPSA Generic Checklist PDFDokument3 SeitenWHO - NPSA Generic Checklist PDFShashwat IVF & Women's HospitalNoch keine Bewertungen

- Van Wessel Steffi - Optimizing Hysteroscopic TreatmentDokument178 SeitenVan Wessel Steffi - Optimizing Hysteroscopic TreatmentMatei EsanuNoch keine Bewertungen

- 08014B VTE Risk Assessment & Thrombophylaxis in Maternity 6.1Dokument22 Seiten08014B VTE Risk Assessment & Thrombophylaxis in Maternity 6.1Anonymous 9dVZCnTXSNoch keine Bewertungen

- Medical and HealthDokument16 SeitenMedical and HealthMUTHUMUNEESH WARANNoch keine Bewertungen

- Veterinary Guidelines For ECT For Superficial TumorsDokument16 SeitenVeterinary Guidelines For ECT For Superficial Tumorsstudio lNoch keine Bewertungen

- Journal Reading AnestesiDokument4 SeitenJournal Reading AnestesiVania RNoch keine Bewertungen

- The Role of The Tissue Viability11Dokument3 SeitenThe Role of The Tissue Viability11RazvannusNoch keine Bewertungen

- T.Hưng Saigon South HospitalDokument31 SeitenT.Hưng Saigon South HospitalTài TháiNoch keine Bewertungen

- Tata Kelola Klinis: (Clinical Governance)Dokument38 SeitenTata Kelola Klinis: (Clinical Governance)Devi TriyadiNoch keine Bewertungen

- Manejo PreoperatorioDokument8 SeitenManejo PreoperatorioMilton FabianNoch keine Bewertungen

- Prevention of Venous Thromboembolism In.35Dokument15 SeitenPrevention of Venous Thromboembolism In.35alodiarkNoch keine Bewertungen

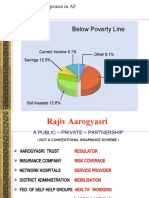

- Hospitalization Expenses in APDokument10 SeitenHospitalization Expenses in APSantosh GunduNoch keine Bewertungen

- Proton Beam Radiation Therapy SVDokument29 SeitenProton Beam Radiation Therapy SVtrieu leNoch keine Bewertungen

- Research Article: Prescription of Kampo Drugs in The Japanese Health Care Insurance ProgramDokument8 SeitenResearch Article: Prescription of Kampo Drugs in The Japanese Health Care Insurance ProgramNicolas CachaNoch keine Bewertungen

- Health Insurance SystemDokument39 SeitenHealth Insurance SystemᎷᏒ.ᏴᎬᎪᏚᎢ.Noch keine Bewertungen

- Information Sheet For Applicants For EmployersDokument13 SeitenInformation Sheet For Applicants For EmployersLhOi ParagasNoch keine Bewertungen

- FSRH Guideline Emergency Contraception 17mar2017 2Dokument65 SeitenFSRH Guideline Emergency Contraception 17mar2017 2blopper123100% (1)

- Jurnal Adenomiosis Dan MiomaDokument8 SeitenJurnal Adenomiosis Dan Miomaperussi pranadiptaNoch keine Bewertungen

- Dr. NTR Vaidya Seva: Quality Medicare For AllDokument48 SeitenDr. NTR Vaidya Seva: Quality Medicare For AllKiran Kumar BulikondaNoch keine Bewertungen

- A Case Study of Caesarean Sections in Referred CasDokument5 SeitenA Case Study of Caesarean Sections in Referred CasBNS 2022Noch keine Bewertungen

- Empanelled Hospitals CGHSDokument107 SeitenEmpanelled Hospitals CGHSankit.shrivastavaNoch keine Bewertungen

- Unit Cost of Inpatient Days in AfricaDokument5 SeitenUnit Cost of Inpatient Days in Africabarkiest24Noch keine Bewertungen

- Prolotherapy Platelet Rich Plasma TherapiesDokument22 SeitenProlotherapy Platelet Rich Plasma TherapiesFrancisco Antonio Vicent PachecoNoch keine Bewertungen

- Japanese Fee Schedule RevisionsDokument47 SeitenJapanese Fee Schedule RevisionsLogan BoehmNoch keine Bewertungen

- Randomised, Controlled Outcome Study of Active Mobilisation Compared With Collar Therapy For Whiplash InjuryDokument5 SeitenRandomised, Controlled Outcome Study of Active Mobilisation Compared With Collar Therapy For Whiplash Injuryririn rahmayeniNoch keine Bewertungen

- The Journal of Physical Therapy Science The Journal of Physical Therapy ScienceDokument4 SeitenThe Journal of Physical Therapy Science The Journal of Physical Therapy ScienceSafiyah SindiNoch keine Bewertungen

- Hospital Safety Index FormDokument45 SeitenHospital Safety Index FormhendraNoch keine Bewertungen

- Complementary Therapies in Clinical Practice: Raana Haj Najafi, Fan Xiao-NongDokument12 SeitenComplementary Therapies in Clinical Practice: Raana Haj Najafi, Fan Xiao-NongSofiaNoch keine Bewertungen

- Optimal Queue Length For Orthopaedic Surgery With Surgeon-Specific Queues and Maximum Waiting TimeDokument9 SeitenOptimal Queue Length For Orthopaedic Surgery With Surgeon-Specific Queues and Maximum Waiting Timeujangketul62Noch keine Bewertungen

- Learning Journal Unit 2Dokument1 SeiteLearning Journal Unit 2writer topNoch keine Bewertungen

- NURS FPX4060 GilliamMelissa - Assessment3 2Dokument9 SeitenNURS FPX4060 GilliamMelissa - Assessment3 2writer topNoch keine Bewertungen

- Week 3 QuizDokument3 SeitenWeek 3 Quizwriter topNoch keine Bewertungen

- MidtermDokument53 SeitenMidtermwriter topNoch keine Bewertungen

- t17 DQ 2Dokument1 Seitet17 DQ 2writer topNoch keine Bewertungen

- MidtermDokument18 SeitenMidtermwriter topNoch keine Bewertungen

- Impact of Corona and Investment Returns of Banks - EditedDokument24 SeitenImpact of Corona and Investment Returns of Banks - Editedwriter topNoch keine Bewertungen

- Unit IIDokument4 SeitenUnit IIwriter topNoch keine Bewertungen

- Topic 6 DQ 1Dokument1 SeiteTopic 6 DQ 1writer topNoch keine Bewertungen

- Social and Emotional Development FinishedDokument4 SeitenSocial and Emotional Development Finishedwriter topNoch keine Bewertungen

- JasciDokument10 SeitenJasciwriter topNoch keine Bewertungen

- 8404382Dokument1 Seite8404382writer topNoch keine Bewertungen

- T 6 DQ 2Dokument1 SeiteT 6 DQ 2writer topNoch keine Bewertungen

- MGT605 Ass 2 Part BDokument13 SeitenMGT605 Ass 2 Part Bwriter topNoch keine Bewertungen

- PPL 300 Critical AnalysisDokument4 SeitenPPL 300 Critical Analysiswriter topNoch keine Bewertungen

- Week 4 AssignmentDokument8 SeitenWeek 4 Assignmentwriter topNoch keine Bewertungen

- BUS560 Module 2 03222013Dokument12 SeitenBUS560 Module 2 03222013writer topNoch keine Bewertungen

- ACC 640 Milestone 3Dokument3 SeitenACC 640 Milestone 3writer topNoch keine Bewertungen

- Health Promotion in Minority Populations 1Dokument5 SeitenHealth Promotion in Minority Populations 1writer topNoch keine Bewertungen

- Assessment 2Dokument14 SeitenAssessment 2writer topNoch keine Bewertungen

- This Study Resource WasDokument2 SeitenThis Study Resource Waswriter topNoch keine Bewertungen

- Case Study Municipal Action On Food and Beverage Marketing To YouthDokument2 SeitenCase Study Municipal Action On Food and Beverage Marketing To Youthwriter topNoch keine Bewertungen

- Tax 650 Milestone 3Dokument5 SeitenTax 650 Milestone 3writer topNoch keine Bewertungen

- ACC 640 Milestone 3Dokument3 SeitenACC 640 Milestone 3writer topNoch keine Bewertungen

- Content Marketing Strategy Assignment CompleteDokument5 SeitenContent Marketing Strategy Assignment Completewriter topNoch keine Bewertungen

- This Study Resource WasDokument5 SeitenThis Study Resource Waswriter topNoch keine Bewertungen

- This Study Resource Was: Predictable To Those Who Know You Well. This PredictabilityDokument1 SeiteThis Study Resource Was: Predictable To Those Who Know You Well. This Predictabilitywriter topNoch keine Bewertungen

- HLTWHS002 AE KN 1of3 Katarina JosipovicDokument20 SeitenHLTWHS002 AE KN 1of3 Katarina Josipovicwriter top100% (1)

- HBSP Case Bancolombia Talent Culture and Value Creation Management in Mergers Questions PDFDokument1 SeiteHBSP Case Bancolombia Talent Culture and Value Creation Management in Mergers Questions PDFwriter topNoch keine Bewertungen

- HLTWHS002 AE1 Scenarios V1.0Dokument10 SeitenHLTWHS002 AE1 Scenarios V1.0writer topNoch keine Bewertungen

- Chiro Case Study Week 2Dokument6 SeitenChiro Case Study Week 2api-479754549Noch keine Bewertungen

- Sage Form 4 UsDokument5 SeitenSage Form 4 UsbhaskaaNoch keine Bewertungen

- Generic Name: Ondansetro N Brand Names: ZofranDokument1 SeiteGeneric Name: Ondansetro N Brand Names: ZofranLemuel GuevarraNoch keine Bewertungen

- Sire CrierDokument12 SeitenSire CrierhollyeNoch keine Bewertungen

- G.I. Quiz QuestionsDokument3 SeitenG.I. Quiz QuestionsTanya ViarsNoch keine Bewertungen

- Curry Leaves - A Medicinal Herb: ISSN-2231-5683 (Print) ISSN - 2231-5691 (Online)Dokument3 SeitenCurry Leaves - A Medicinal Herb: ISSN-2231-5683 (Print) ISSN - 2231-5691 (Online)Anand Srinivas RamanNoch keine Bewertungen

- SCI135 Research Project - EditedDokument4 SeitenSCI135 Research Project - EditedRachael KaburuNoch keine Bewertungen

- BreastfeedingDokument30 SeitenBreastfeedingEl Avion Noel100% (1)

- Case PresentationDokument7 SeitenCase PresentationGrace SamNoch keine Bewertungen

- Three Basic Spring Forest Qigong ExercisesDokument8 SeitenThree Basic Spring Forest Qigong Exercisesgaweshajeewani67% (3)

- Summary of Learning-Pulmo Hour-Tantoco, Justin LareeDokument1 SeiteSummary of Learning-Pulmo Hour-Tantoco, Justin LareeJustin TantocoNoch keine Bewertungen

- Psych Drugs - From MedbulletsDokument2 SeitenPsych Drugs - From MedbulletsFazeyfazeNoch keine Bewertungen

- A Cesarean SectionDokument9 SeitenA Cesarean SectionmejulNoch keine Bewertungen

- 37-Article Text-53-1-10-20191003Dokument9 Seiten37-Article Text-53-1-10-20191003Jainal JwNoch keine Bewertungen

- 2017 MP Starter Plan 5 To 9 Proposal - Complete RidersDokument17 Seiten2017 MP Starter Plan 5 To 9 Proposal - Complete RidersJoselle M. GaddiNoch keine Bewertungen

- Neuromuscular Disorders: Peripheral Nervous System/ Myelopathy Case SessionDokument3 SeitenNeuromuscular Disorders: Peripheral Nervous System/ Myelopathy Case Sessionamitm2012Noch keine Bewertungen

- 50 Ideas For Massage and Spa Promotion by Gael WoodDokument56 Seiten50 Ideas For Massage and Spa Promotion by Gael Woodnahv_08100% (2)

- What Causes Pain Behind The KneeDokument7 SeitenWhat Causes Pain Behind The KneeRatnaPrasadNalamNoch keine Bewertungen

- Keira Stampfly: Doctor of Physical Therapy (906) - 202-2523Dokument1 SeiteKeira Stampfly: Doctor of Physical Therapy (906) - 202-2523api-677928137Noch keine Bewertungen

- Hildegard Peplau's Theory of Interpersonal RelationsDokument20 SeitenHildegard Peplau's Theory of Interpersonal RelationsSofie May Nellas100% (2)

- A CBT Guide To ConcentrationDokument8 SeitenA CBT Guide To ConcentrationYamini DasguptaNoch keine Bewertungen

- Deep Margin ElevationDokument11 SeitenDeep Margin Elevationjarodzee100% (4)

- What Is TAHbsoDokument2 SeitenWhat Is TAHbsomiskidd100% (2)

- Wound Bioburden: (To Fulfill The Task of Wound Care Subject)Dokument24 SeitenWound Bioburden: (To Fulfill The Task of Wound Care Subject)Fransiska Marchelina HutabaratNoch keine Bewertungen

- A Report On How To Stay HealthyDokument3 SeitenA Report On How To Stay HealthyTharsmilaRamooNoch keine Bewertungen

- B32C08 Lab Report ProformaDokument13 SeitenB32C08 Lab Report Proformajtoh22Noch keine Bewertungen

- History of HypnosisDokument3 SeitenHistory of Hypnosisbutterfly975k100% (1)

- Stages in Orthodontic TreatmentDokument32 SeitenStages in Orthodontic TreatmentDavid FernandezNoch keine Bewertungen

- National Burn Care Referral Guidance: Specialised ServicesDokument10 SeitenNational Burn Care Referral Guidance: Specialised ServicesSrsblackieNoch keine Bewertungen