Das könnte Ihnen auch gefallen

- LESSON 5 - THE AUDIT PROCESS-Planning and Quality ControlDokument7 SeitenLESSON 5 - THE AUDIT PROCESS-Planning and Quality Controlkipngetich392100% (1)

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeVon EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeBewertung: 5 von 5 Sternen5/5 (1)

- Auditing Assignment 1 #14526Dokument15 SeitenAuditing Assignment 1 #14526Mahiana MillieNoch keine Bewertungen

- Answer Key in Applied Auditing by Cabrera 2006 EditionDokument271 SeitenAnswer Key in Applied Auditing by Cabrera 2006 EditionGwyneth Ü Elipanio100% (14)

- Information Systems Auditing: The IS Audit Follow-up ProcessVon EverandInformation Systems Auditing: The IS Audit Follow-up ProcessBewertung: 2 von 5 Sternen2/5 (1)

- CAPIFUND MCA Training Material 2022Dokument11 SeitenCAPIFUND MCA Training Material 2022Carmelo PalaciosNoch keine Bewertungen

- Audit Problem (Aaconapps2 - Cash and ReceivablesDokument261 SeitenAudit Problem (Aaconapps2 - Cash and ReceivablesDawson Dela CruzNoch keine Bewertungen

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018Von EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Noch keine Bewertungen

- APPLIED AUDITING Module 1Dokument3 SeitenAPPLIED AUDITING Module 1Paul Fajardo CanoyNoch keine Bewertungen

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19Von EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19Noch keine Bewertungen

- Brian Christian S. Villaluz, Cpa Learning Advancement Review Center (Lead)Dokument6 SeitenBrian Christian S. Villaluz, Cpa Learning Advancement Review Center (Lead)Gillyn CalaguiNoch keine Bewertungen

- MODULE 6 - Audit PlanningDokument9 SeitenMODULE 6 - Audit PlanningRufina B VerdeNoch keine Bewertungen

- Role of A Nurse in Material ManagementDokument8 SeitenRole of A Nurse in Material ManagementVince100% (9)

- Audit Planning ProcessDokument7 SeitenAudit Planning ProcessDelelegn AyalikeNoch keine Bewertungen

- IMT - Supply Chain MGMT - Session 11&12Dokument49 SeitenIMT - Supply Chain MGMT - Session 11&12Himanish BhandariNoch keine Bewertungen

- Exam 3 Review Sheet Summer 09Dokument14 SeitenExam 3 Review Sheet Summer 09kpatel4uNoch keine Bewertungen

- Flipkart WiRED 4.0 - PPT TemplateDokument15 SeitenFlipkart WiRED 4.0 - PPT Templaterohit100% (1)

- PSADokument17 SeitenPSAMichelle de Guzman100% (1)

- Auditing Standards Summary DK-Dheeraj KukrejaDokument16 SeitenAuditing Standards Summary DK-Dheeraj KukrejaRajavati NadarNoch keine Bewertungen

- Discuss The Following Concepts in The Conduct of AuditDokument8 SeitenDiscuss The Following Concepts in The Conduct of Auditureka6arnicaNoch keine Bewertungen

- Lesson 5 Audit Planning and Audit RiskDokument13 SeitenLesson 5 Audit Planning and Audit Riskwambualucas74Noch keine Bewertungen

- Client Selection and RetentionDokument20 SeitenClient Selection and RetentionJurie MayNoch keine Bewertungen

- Audit Practice and Assurance Services - A1.4 PDFDokument94 SeitenAudit Practice and Assurance Services - A1.4 PDFFRANCOIS NKUNDIMANANoch keine Bewertungen

- AT Lecture 6 - Planning An Audit of FS June 2020Dokument8 SeitenAT Lecture 6 - Planning An Audit of FS June 2020Sophia TenorioNoch keine Bewertungen

- Chapter 3 AudDokument17 SeitenChapter 3 AudMoti BekeleNoch keine Bewertungen

- The Audit ProcessDokument20 SeitenThe Audit ProcessmavhikalucksonprofaccNoch keine Bewertungen

- Audit Chapter 3Dokument18 SeitenAudit Chapter 3Nur ShahiraNoch keine Bewertungen

- Chapter 9 Cabrera Applied AuditingDokument5 SeitenChapter 9 Cabrera Applied AuditingCristy Estrella50% (4)

- Auditing One 03 OKDokument28 SeitenAuditing One 03 OKRObel demisNoch keine Bewertungen

- Activity 4Dokument12 SeitenActivity 4Beatrice Ella DomingoNoch keine Bewertungen

- Overview of The Audit ProcessDokument4 SeitenOverview of The Audit Processneo14Noch keine Bewertungen

- LO1: Discuss Why Adequate Audit Planning Is Essential: The 8 Parts of Audit Planning Are As FollowsDokument17 SeitenLO1: Discuss Why Adequate Audit Planning Is Essential: The 8 Parts of Audit Planning Are As FollowsMahmoud AhmedNoch keine Bewertungen

- Module 6 - Audit PlanningDokument15 SeitenModule 6 - Audit PlanningMAG MAGNoch keine Bewertungen

- (Midterm) Aap - Module 4 Psa-200 - 210 - 240Dokument7 Seiten(Midterm) Aap - Module 4 Psa-200 - 210 - 24025 CUNTAPAY, FRENCHIE VENICE B.Noch keine Bewertungen

- AT - Lesson 2 - 1st Batch - MARPDokument17 SeitenAT - Lesson 2 - 1st Batch - MARPKile Rien MonsadaNoch keine Bewertungen

- Chapter 9-AuditDokument45 SeitenChapter 9-AuditMisshtaCNoch keine Bewertungen

- Knowledge Based QuestionsDokument17 SeitenKnowledge Based Questions5mh8cyfgt4Noch keine Bewertungen

- Au 00318 PDFDokument23 SeitenAu 00318 PDFAlyssa Hallasgo-Lopez AtabeloNoch keine Bewertungen

- AU-00314 Auditing A Business Risk ApproachDokument43 SeitenAU-00314 Auditing A Business Risk Approachredearth2929Noch keine Bewertungen

- Module 3 - AuditingDokument22 SeitenModule 3 - AuditingSophia Grace NiduazaNoch keine Bewertungen

- Tax 2 and Ism ProjetDokument22 SeitenTax 2 and Ism ProjetAngelica CastilloNoch keine Bewertungen

- CHAPTER 1. OVERVIEW OF THE AUDIT PROCESSxDokument26 SeitenCHAPTER 1. OVERVIEW OF THE AUDIT PROCESSxJerome_JadeNoch keine Bewertungen

- Agreed Upon ProceduresDokument3 SeitenAgreed Upon ProceduresSarala WdNoch keine Bewertungen

- Discuss The Following Concepts in The Conduct of Audit: Materiality, Reasonable Assurance, Professional Scepticism, and Professional JudgmentDokument8 SeitenDiscuss The Following Concepts in The Conduct of Audit: Materiality, Reasonable Assurance, Professional Scepticism, and Professional JudgmentJun Zen Ralph YapNoch keine Bewertungen

- ACCO 30043 Assignment No.3Dokument8 SeitenACCO 30043 Assignment No.3RoseanneNoch keine Bewertungen

- Chapter - 3Dokument8 SeitenChapter - 3dejen mengstieNoch keine Bewertungen

- Chapter-6: in An Effective Manner. Planning Consists of A Number of Elements. However, They Could Be Summarized AsDokument10 SeitenChapter-6: in An Effective Manner. Planning Consists of A Number of Elements. However, They Could Be Summarized AsNasir RifatNoch keine Bewertungen

- Philippine Standard On Related Services 4400Dokument10 SeitenPhilippine Standard On Related Services 4400JecNoch keine Bewertungen

- Cambodian Standard On Auditing - English VersionDokument51 SeitenCambodian Standard On Auditing - English Versionpostbox855100% (8)

- AAS 30 External ConfirmationsDokument9 SeitenAAS 30 External ConfirmationsRishabh GuptaNoch keine Bewertungen

- Before Planning Audit Programme: 3 Audit Checklist - For CompaniesDokument2 SeitenBefore Planning Audit Programme: 3 Audit Checklist - For CompaniesMudit KothariNoch keine Bewertungen

- Audit PlanningDokument12 SeitenAudit PlanningDeryl GalveNoch keine Bewertungen

- CH 3 6Dokument15 SeitenCH 3 6Gizachew MayebetNoch keine Bewertungen

- 20021ipcc Paper6 Vol1 Cp3Dokument49 Seiten20021ipcc Paper6 Vol1 Cp3kunalNoch keine Bewertungen

- Summary of SADokument22 SeitenSummary of SAEkansh GargNoch keine Bewertungen

- Chapter01 - Overview of The Audit ProcessDokument3 SeitenChapter01 - Overview of The Audit ProcessCristy Estrella0% (1)

- Audit StandardsDokument36 SeitenAudit StandardsPooja BaghelNoch keine Bewertungen

- Correct/ Incorrect Questions: Ch1 - Nature, Scope and Objectives of AuditDokument31 SeitenCorrect/ Incorrect Questions: Ch1 - Nature, Scope and Objectives of AuditNbut ddgfNoch keine Bewertungen

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsVon EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNoch keine Bewertungen

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsVon EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNoch keine Bewertungen

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18Von EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18Noch keine Bewertungen

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19Von EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19Noch keine Bewertungen

- Global DimensionsDokument45 SeitenGlobal DimensionsgeorgegeorgeNoch keine Bewertungen

- Mitc RupifiDokument13 SeitenMitc RupifiKARTHIKEYAN K.DNoch keine Bewertungen

- Nayatel BillDokument1 SeiteNayatel Billnr pakiNoch keine Bewertungen

- Master Module - Eresource 3GL ERP (ERP For Transportation)Dokument20 SeitenMaster Module - Eresource 3GL ERP (ERP For Transportation)Eresource EtradeNoch keine Bewertungen

- Central Bank of Bahrain Volume 3-Insurance PART BDokument26 SeitenCentral Bank of Bahrain Volume 3-Insurance PART BZaheer AhmadNoch keine Bewertungen

- Mock Call ScriptDokument2 SeitenMock Call ScriptDhan VelaNoch keine Bewertungen

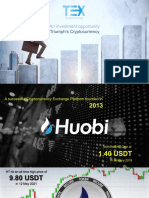

- An Investment Opportunity: Triumph's CryptocurrencyDokument25 SeitenAn Investment Opportunity: Triumph's Cryptocurrency- hermanNoch keine Bewertungen

- Returnsform Eng Rowpdf PDFDokument1 SeiteReturnsform Eng Rowpdf PDFXpnNoch keine Bewertungen

- Asav s2sDokument10 SeitenAsav s2sswtNoch keine Bewertungen

- S.No. Customer Circle Reason For Delay Due Date Sales Order DateDokument366 SeitenS.No. Customer Circle Reason For Delay Due Date Sales Order DatePriya SawantNoch keine Bewertungen

- T2135-Sales and Distribution ManagementDokument4 SeitenT2135-Sales and Distribution ManagementLOCKEY SQUADNoch keine Bewertungen

- PF Pension Settlement Form-TCSDokument4 SeitenPF Pension Settlement Form-TCSSridhara Krishna BodavulaNoch keine Bewertungen

- Ticket Types: CityxpressDokument4 SeitenTicket Types: Cityxpressspati2Noch keine Bewertungen

- Sample WBS A2 2017-18 - 2Dokument1 SeiteSample WBS A2 2017-18 - 2Kennedy BlessingNoch keine Bewertungen

- LTC Procedural Norms PDFDokument5 SeitenLTC Procedural Norms PDFsk_kannan26Noch keine Bewertungen

- TICKET202311291756081864485Dokument1 SeiteTICKET202311291756081864485nurshakiblimon2018Noch keine Bewertungen

- Policies and Practices For A Safer More ResponsiblDokument62 SeitenPolicies and Practices For A Safer More ResponsiblBobskinnyNoch keine Bewertungen

- Critical Information Summary - Long Expiry Pre-Paid MobileDokument1 SeiteCritical Information Summary - Long Expiry Pre-Paid MobileCalvin MaiNoch keine Bewertungen

- Auditing Notes.Dokument55 SeitenAuditing Notes.Viraja Guru50% (2)

- Acounting PDFDokument3 SeitenAcounting PDFashishNoch keine Bewertungen

- UIPM BlockchainDokument1 SeiteUIPM BlockchainArsaNoch keine Bewertungen

- Letter of Credit MaybankDokument3 SeitenLetter of Credit MaybankBuayaz GamingNoch keine Bewertungen

- Web Development Complete - BluehostDokument2 SeitenWeb Development Complete - BluehostroheelNoch keine Bewertungen

- Comandos Ccna SecurityDokument26 SeitenComandos Ccna SecurityRobtech opsNoch keine Bewertungen

- Fixed Deposit Rate ChartDokument3 SeitenFixed Deposit Rate ChartmoregauravNoch keine Bewertungen

- Acc Ch-7 Average Due Date SaDokument15 SeitenAcc Ch-7 Average Due Date SaShivaSrinivas100% (3)