Das könnte Ihnen auch gefallen

- 50 Ways To Balance MagicDokument11 Seiten50 Ways To Balance MagicRodolfo AlencarNoch keine Bewertungen

- Complimentary JournalDokument58 SeitenComplimentary JournalMcKey ZoeNoch keine Bewertungen

- Annuity CommissionsDokument18 SeitenAnnuity CommissionsScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Hiring GuideDokument42 SeitenHiring GuidenalkhaNoch keine Bewertungen

- Fiduciary Duties and Obligations in Administering 457 (B) Plans Under California LawDokument21 SeitenFiduciary Duties and Obligations in Administering 457 (B) Plans Under California LawScott Dauenhauer100% (2)

- Data Analytics Healthcare ProvidersDokument17 SeitenData Analytics Healthcare Providersnilesh39100% (1)

- Disappearance of Madeleine McCannDokument36 SeitenDisappearance of Madeleine McCannCopernicNoch keine Bewertungen

- HR Quarterly PWCDokument19 SeitenHR Quarterly PWCaxitmNoch keine Bewertungen

- The 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesVon EverandThe 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesNoch keine Bewertungen

- Economics and The Theory of Games - Vega-Redondo PDFDokument526 SeitenEconomics and The Theory of Games - Vega-Redondo PDFJaime Andrés67% (3)

- Book3 79 111000 0000100120 DAH MPL RPT 000005 - ADokument101 SeitenBook3 79 111000 0000100120 DAH MPL RPT 000005 - ANassif Abi AbdallahNoch keine Bewertungen

- Health Information SystemDokument11 SeitenHealth Information SystemVineeta Jose100% (1)

- New Japa Retreat NotebookDokument48 SeitenNew Japa Retreat NotebookRob ElingsNoch keine Bewertungen

- Self ReflectivityDokument7 SeitenSelf ReflectivityJoseph Jajo100% (1)

- Untitled 1Dokument6 SeitenUntitled 1api-270402880Noch keine Bewertungen

- Comparison AnalysisDokument169 SeitenComparison AnalysissuccessinmpNoch keine Bewertungen

- CPABC Roundtable Spring 2004Dokument8 SeitenCPABC Roundtable Spring 2004cpabcNoch keine Bewertungen

- BUSI-2031-FA - Group Project ProposalDokument6 SeitenBUSI-2031-FA - Group Project Proposalvamshi20.2003Noch keine Bewertungen

- Annual Report 2010Dokument24 SeitenAnnual Report 2010Manisha SureshNoch keine Bewertungen

- Report On How To Recruit and Retain Riverside County EmployeesDokument5 SeitenReport On How To Recruit and Retain Riverside County EmployeesThe Press-Enterprise / pressenterprise.comNoch keine Bewertungen

- 3Dokument5 Seiten3vamshi20.2003Noch keine Bewertungen

- LEAKED: CBC Internal Employee Q&ADokument4 SeitenLEAKED: CBC Internal Employee Q&ACANADALANDNoch keine Bewertungen

- NTSAA Iowa TestimonyDokument16 SeitenNTSAA Iowa TestimonyScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Operational Plan for Bounce Fitness Pilot ProjectDokument5 SeitenOperational Plan for Bounce Fitness Pilot ProjectStacy ParkerNoch keine Bewertungen

- Latc Newsletter 2 May 2014Dokument4 SeitenLatc Newsletter 2 May 2014api-233449525Noch keine Bewertungen

- NTJN, Full Conference Program - FINALDokument60 SeitenNTJN, Full Conference Program - FINALtjprogramsNoch keine Bewertungen

- Hafa 2015 SummitDokument24 SeitenHafa 2015 Summitapi-282947512Noch keine Bewertungen

- HB Comp Study - CCRPC Executive Comm PresentationDokument18 SeitenHB Comp Study - CCRPC Executive Comm PresentationLazain ZulhamNoch keine Bewertungen

- Isle of Wight Council Corporate Peer ChallengeDokument23 SeitenIsle of Wight Council Corporate Peer ChallengeIWCPOnlineNoch keine Bewertungen

- Employee Engagement Initiatives: Financial ServicesDokument11 SeitenEmployee Engagement Initiatives: Financial ServicesaatishNoch keine Bewertungen

- SEAP Presentation August 2009Dokument42 SeitenSEAP Presentation August 2009terryboothNoch keine Bewertungen

- Canadian Men's Health Foundation 2015 Operating PlanDokument23 SeitenCanadian Men's Health Foundation 2015 Operating PlanGhie SorianoNoch keine Bewertungen

- SAC Minutes March 10 2010Dokument3 SeitenSAC Minutes March 10 2010Staff Advisory Council at DUNoch keine Bewertungen

- Successful Action For Lobby Day!: LocalDokument6 SeitenSuccessful Action For Lobby Day!: LocalForward GallopNoch keine Bewertungen

- Gateway: Building Real Solutions For Real Lives .Dokument28 SeitenGateway: Building Real Solutions For Real Lives .Transformed By YouNoch keine Bewertungen

- 2021 LTC Workforce Development ReportDokument89 Seiten2021 LTC Workforce Development ReportSammy DeeNoch keine Bewertungen

- NTSSA Cover Summer 2011Dokument3 SeitenNTSSA Cover Summer 2011Scott DauenhauerNoch keine Bewertungen

- Value For Money ResearchDokument2 SeitenValue For Money ResearchMikhail ArdenNoch keine Bewertungen

- SAC Minutes March 14 2012Dokument4 SeitenSAC Minutes March 14 2012Staff Advisory Council at DUNoch keine Bewertungen

- Faculty RegentDokument5 SeitenFaculty RegentRonilo Jose Danila FloresNoch keine Bewertungen

- Letter To Superintendent Harter 4.15.2014Dokument4 SeitenLetter To Superintendent Harter 4.15.2014alex_gronkeNoch keine Bewertungen

- Salem-Keizer Public Schools 2012-13 Budget Message (Draft)Dokument23 SeitenSalem-Keizer Public Schools 2012-13 Budget Message (Draft)Statesman JournalNoch keine Bewertungen

- PDD Family Forum PowerPoint PresentationDokument22 SeitenPDD Family Forum PowerPoint PresentationactionhallNoch keine Bewertungen

- Oxford Brookes Dissertation PrintingDokument4 SeitenOxford Brookes Dissertation PrintingCollegePaperWritingServicesSingapore100% (1)

- Hawkesbury Community Care Forum - Q and ADokument4 SeitenHawkesbury Community Care Forum - Q and Awscf_auNoch keine Bewertungen

- Busn 179 CCP RevisedDokument30 SeitenBusn 179 CCP Revisedapi-395972922Noch keine Bewertungen

- ESCC Disability Employment ReportDokument50 SeitenESCC Disability Employment Reportalam_haikleNoch keine Bewertungen

- Five Employment AspectsDokument7 SeitenFive Employment AspectsgerrymalgapoNoch keine Bewertungen

- PD - Global Payroll AnalystDokument2 SeitenPD - Global Payroll AnalystJosesitoleNoch keine Bewertungen

- Bcba CourseworkDokument8 SeitenBcba Courseworkafjwoamzdxwmct100% (2)

- Board Member Recruitment Project Resource ToolkitDokument24 SeitenBoard Member Recruitment Project Resource ToolkitAnonymous bXlDKsWysNoch keine Bewertungen

- John Kerry Ensured 2nd MeetingDokument8 SeitenJohn Kerry Ensured 2nd MeetingSyndicated NewsNoch keine Bewertungen

- NHRD HR Showcase 2020Dokument206 SeitenNHRD HR Showcase 2020Suraj TiwariNoch keine Bewertungen

- Job Description: Data Architect / Data Modeler Requisition ID: 15001465Dokument11 SeitenJob Description: Data Architect / Data Modeler Requisition ID: 15001465Simon BoyoNoch keine Bewertungen

- Moh New Employee Onboarding Checklist First Month v0.1Dokument3 SeitenMoh New Employee Onboarding Checklist First Month v0.1hannahcollinson3Noch keine Bewertungen

- Resume - J Lemon, Maria RDokument6 SeitenResume - J Lemon, Maria RMaria LemonNoch keine Bewertungen

- Nccs DissertationDokument7 SeitenNccs DissertationBuyPsychologyPapersSingapore100% (1)

- Introduction of The Solicitors Qualifying Examination:: March 2017Dokument63 SeitenIntroduction of The Solicitors Qualifying Examination:: March 2017Legal CheekNoch keine Bewertungen

- CMS Report 4Dokument9 SeitenCMS Report 4RecordTrac - City of OaklandNoch keine Bewertungen

- Afp Whitepaper FINALDokument17 SeitenAfp Whitepaper FINALManikantan NatarajanNoch keine Bewertungen

- Thesis About Service DeliveryDokument8 SeitenThesis About Service Deliveryfjncb9rp100% (2)

- Thesis Internship UsaDokument4 SeitenThesis Internship Usameghanhowardmanchester100% (2)

- Boota, Zinat Report v2012Dokument15 SeitenBoota, Zinat Report v2012Karolia ZinatNoch keine Bewertungen

- Description: Tags: Nrcflas-Pam2006-09Dokument66 SeitenDescription: Tags: Nrcflas-Pam2006-09anon-659674Noch keine Bewertungen

- Fleet Synch - Sailor of 2025 - FinalDokument19 SeitenFleet Synch - Sailor of 2025 - FinalCDR SalamanderNoch keine Bewertungen

- Taj Mahal India Photo 2010Dokument6 SeitenTaj Mahal India Photo 2010Mijail CastilloNoch keine Bewertungen

- Putting Data To Work Brief 11-10Dokument16 SeitenPutting Data To Work Brief 11-10Valerie F. LeonardNoch keine Bewertungen

- CPD updates in accounting professionDokument5 SeitenCPD updates in accounting professionKathreen Aya ExcondeNoch keine Bewertungen

- Extracted Guide Questions For Field TeamsDokument7 SeitenExtracted Guide Questions For Field TeamsIluminadaNoch keine Bewertungen

- Country Diagnostic Study on Long-Term Care in Sri LankaVon EverandCountry Diagnostic Study on Long-Term Care in Sri LankaNoch keine Bewertungen

- LSW Non-ERISA TripsDokument2 SeitenLSW Non-ERISA TripsScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- National Life Group DestinationsDokument6 SeitenNational Life Group DestinationsScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Teacher PostcardDokument2 SeitenTeacher PostcardScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- LSW Advisor ResourcesDokument1 SeiteLSW Advisor ResourcesScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- 19586-PS B RetirementPlanTrends HigherEducation LOWREZVIEWONLY FINAL 122315 Tcm73-55252Dokument32 Seiten19586-PS B RetirementPlanTrends HigherEducation LOWREZVIEWONLY FINAL 122315 Tcm73-55252Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Annuity Investors RevealedDokument1 SeiteAnnuity Investors RevealedScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- LSW 2018Dokument2 SeitenLSW 2018Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- LSW 2017Dokument2 SeitenLSW 2017Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- NLG Sicily Chairman's Club 2016 Qualification FlyerDokument2 SeitenNLG Sicily Chairman's Club 2016 Qualification FlyerScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- 2017 Cabos ConferenceDokument2 Seiten2017 Cabos ConferenceScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- AXA Methodological SummaryDokument6 SeitenAXA Methodological SummaryScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Ntsa SB 1297Dokument2 SeitenNtsa SB 1297Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Midland NL Premier Agent ClubDokument16 SeitenMidland NL Premier Agent ClubScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- MNL Bora Bora 2014Dokument1 SeiteMNL Bora Bora 2014Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- MNL Costa Rica TripDokument1 SeiteMNL Costa Rica TripScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- ValuTeachers Letter To SECDokument1 SeiteValuTeachers Letter To SECScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- 457 (B) Awareness MeetingDokument12 Seiten457 (B) Awareness MeetingScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- MNL Bora Bora 2014Dokument1 SeiteMNL Bora Bora 2014Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

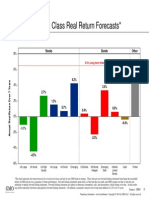

- GMO-Valuation Study and Forward ReturnsDokument8 SeitenGMO-Valuation Study and Forward Returnsstreettalk700Noch keine Bewertungen

- MNL Costa Rica TripDokument1 SeiteMNL Costa Rica TripScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- St. Vrain Plan Transition SummaryDokument2 SeitenSt. Vrain Plan Transition SummaryScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Midland NL Premier Agent ClubDokument16 SeitenMidland NL Premier Agent ClubScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- VL 19724 0510 1 1Dokument6 SeitenVL 19724 0510 1 1Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- TDS Group Sued by Former RepDokument66 SeitenTDS Group Sued by Former RepScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- GMO 7 Year Asset Forecast - Jan 2014Dokument1 SeiteGMO 7 Year Asset Forecast - Jan 2014CanadianValueNoch keine Bewertungen

- NTSAA Iowa TestimonyDokument16 SeitenNTSAA Iowa TestimonyScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- TDS Aspire LetterDokument8 SeitenTDS Aspire LetterScott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- Schools First Letter 10-14-09Dokument2 SeitenSchools First Letter 10-14-09Scott Dauenhauer, CFP, MSFP, AIFNoch keine Bewertungen

- T Cells & Autoimmunity, s3Dokument21 SeitenT Cells & Autoimmunity, s3LiaAriestaNoch keine Bewertungen

- Frequently Asked Questions: Wiring RulesDokument21 SeitenFrequently Asked Questions: Wiring RulesRashdan HarunNoch keine Bewertungen

- Lab Report AcetaminophenDokument5 SeitenLab Report Acetaminophenapi-487596846Noch keine Bewertungen

- Leks Concise Guide To Trademark Law in IndonesiaDokument16 SeitenLeks Concise Guide To Trademark Law in IndonesiaRahmadhini RialiNoch keine Bewertungen

- Science SimulationsDokument4 SeitenScience Simulationsgk_gbuNoch keine Bewertungen

- Sight Reduction Tables For Marine Navigation: B, R - D, D. SDokument12 SeitenSight Reduction Tables For Marine Navigation: B, R - D, D. SGeani MihaiNoch keine Bewertungen

- Ultimate Guide To Construction SubmittalsDokument10 SeitenUltimate Guide To Construction SubmittalsDavid ConroyNoch keine Bewertungen

- Activity 2Dokument5 SeitenActivity 2Kier VillegasNoch keine Bewertungen

- Quality Management - QuestionDokument4 SeitenQuality Management - QuestionLawzy Elsadig SeddigNoch keine Bewertungen

- Historical Source Author Date of The Event Objective of The Event Persons Involved Main ArgumentDokument5 SeitenHistorical Source Author Date of The Event Objective of The Event Persons Involved Main ArgumentMark Saldie RoncesvallesNoch keine Bewertungen

- SSRN Id26238Dokument21 SeitenSSRN Id26238Ayame KusuragiNoch keine Bewertungen

- Trishasti Shalaka Purusa Caritra 4 PDFDokument448 SeitenTrishasti Shalaka Purusa Caritra 4 PDFPratik ChhedaNoch keine Bewertungen

- Samuel Vizcaino: Professional ProfileDokument3 SeitenSamuel Vizcaino: Professional ProfileVizcaíno SamuelNoch keine Bewertungen

- Amway Final ReportDokument74 SeitenAmway Final ReportRadhika Malhotra75% (4)

- A. Hardened Concrete (Non-Destructive Tests) : The SAC Programme Is Managed by Enterprise SingaporeDokument2 SeitenA. Hardened Concrete (Non-Destructive Tests) : The SAC Programme Is Managed by Enterprise Singaporeng chee yongNoch keine Bewertungen

- Expt 1 Yarn Formation (Sherley Trash Analyser)Dokument7 SeitenExpt 1 Yarn Formation (Sherley Trash Analyser)Yashdeep Sharma0% (1)

- MacEwan APA 7th Edition Quick Guide - 1Dokument4 SeitenMacEwan APA 7th Edition Quick Guide - 1Lynn PennyNoch keine Bewertungen

- Short Answers Class 9thDokument14 SeitenShort Answers Class 9thRizwan AliNoch keine Bewertungen

- History shapes Philippine societyDokument4 SeitenHistory shapes Philippine societyMarvin GwapoNoch keine Bewertungen

- User Manual LCD Signature Pad Signotec SigmaDokument15 SeitenUser Manual LCD Signature Pad Signotec SigmaGael OmgbaNoch keine Bewertungen

- OTGNNDokument13 SeitenOTGNNAnh Vuong TuanNoch keine Bewertungen

- Robotic End Effectors - Payload Vs Grip ForceDokument8 SeitenRobotic End Effectors - Payload Vs Grip ForcesamirNoch keine Bewertungen