Das könnte Ihnen auch gefallen

- Speech 140110Dokument6 SeitenSpeech 140110ratiNoch keine Bewertungen

- Proposal For ReDokument3 SeitenProposal For ReelvyannNoch keine Bewertungen

- Barclays' Strategic Position Regarding New Financial Market RegulationsDokument21 SeitenBarclays' Strategic Position Regarding New Financial Market Regulationskatarzena4228Noch keine Bewertungen

- Drfoong30 03 2009Dokument2 SeitenDrfoong30 03 2009Onisha GeorgeNoch keine Bewertungen

- World Economy Financial Repression 1Dokument9 SeitenWorld Economy Financial Repression 1dontmove14150Noch keine Bewertungen

- Financial Globalisation.1Dokument7 SeitenFinancial Globalisation.1Steeves DevaletNoch keine Bewertungen

- Standards For Crisis PreventionDokument17 SeitenStandards For Crisis Preventionanon_767585351Noch keine Bewertungen

- Government and Financial Market: Submitted ToDokument5 SeitenGovernment and Financial Market: Submitted ToMegh Nath RegmiNoch keine Bewertungen

- Regulatory BankerDokument5 SeitenRegulatory BankerFrnzie FrndzNoch keine Bewertungen

- Monetary Economics UZ Individual FinalDokument10 SeitenMonetary Economics UZ Individual FinalMilton ChinhoroNoch keine Bewertungen

- Globalisation of Financial MarketDokument17 SeitenGlobalisation of Financial MarketPiya SharmaNoch keine Bewertungen

- En Special Series On Covid 19 Central Bank Support To Financial Markets in The Coronavirus PandemicDokument12 SeitenEn Special Series On Covid 19 Central Bank Support To Financial Markets in The Coronavirus PandemicNavendu TripathiNoch keine Bewertungen

- Lessons of The Financial Crisis For Future Regulation of Financial Institutions and Markets and For Liquidity ManagementDokument27 SeitenLessons of The Financial Crisis For Future Regulation of Financial Institutions and Markets and For Liquidity ManagementrenysipNoch keine Bewertungen

- Regulation of Banking and Financial MarketsDokument37 SeitenRegulation of Banking and Financial Marketslegalmatters100% (5)

- Elucidate The Importance of International Finanace in This Era of GlobalisationDokument15 SeitenElucidate The Importance of International Finanace in This Era of GlobalisationAnsariMohammedShoaibNoch keine Bewertungen

- Analysis of Brazil's Derivatives MarketDokument3 SeitenAnalysis of Brazil's Derivatives MarketRaghav PokharelNoch keine Bewertungen

- The Influence of The Strong Economy On Financial Markets: All The Other Organs Take Their Tone."Dokument2 SeitenThe Influence of The Strong Economy On Financial Markets: All The Other Organs Take Their Tone."Ronalie Sustuedo100% (1)

- Crisis of CreditDokument4 SeitenCrisis of CreditRaven PicorroNoch keine Bewertungen

- Plcy 08 IDokument3 SeitenPlcy 08 ILam SameerNoch keine Bewertungen

- Monetary Economics UZ Individual AssignmentDokument9 SeitenMonetary Economics UZ Individual AssignmentMilton ChinhoroNoch keine Bewertungen

- Financial LiberalizationDokument45 SeitenFinancial LiberalizationazeemNoch keine Bewertungen

- Role of Government in Financial MarketDokument28 SeitenRole of Government in Financial MarketHaji Suleman Ali0% (1)

- Capital Controls by JomoDokument17 SeitenCapital Controls by Jomojoe abdullahNoch keine Bewertungen

- Global Financial CrisisDokument4 SeitenGlobal Financial CrisiswehsanNoch keine Bewertungen

- CH4 - CH 6 Edited - 2013Dokument6 SeitenCH4 - CH 6 Edited - 2013kirosNoch keine Bewertungen

- Transition EconomyDokument9 SeitenTransition EconomyDumitrita TabacaruNoch keine Bewertungen

- Chap 13Dokument5 SeitenChap 13Jade Marie FerrolinoNoch keine Bewertungen

- Chapter 6 FIMDokument5 SeitenChapter 6 FIMZerihun ReguNoch keine Bewertungen

- Policy Insight 68Dokument13 SeitenPolicy Insight 68unicycle1234Noch keine Bewertungen

- Impact of Globalization in Global Economic and Financial CrisisDokument7 SeitenImpact of Globalization in Global Economic and Financial CrisisHasibun ShuhadNoch keine Bewertungen

- Jean-Pierre Landau: Procyclicality - What It Means and What Could Be DoneDokument6 SeitenJean-Pierre Landau: Procyclicality - What It Means and What Could Be DoneSunil Kumar GaurNoch keine Bewertungen

- Stiglitz Financial System in DevelopmentDokument17 SeitenStiglitz Financial System in DevelopmentAmit BhushanNoch keine Bewertungen

- Chapter Five Regulation of Financial Markets and Institutions and Financial InnovationDokument22 SeitenChapter Five Regulation of Financial Markets and Institutions and Financial InnovationMikias DegwaleNoch keine Bewertungen

- Libéralisation Du Compte CapitalDokument4 SeitenLibéralisation Du Compte Capitalelyka.paintingNoch keine Bewertungen

- (Done) How Do Market Failures Justify Interventions in Rural Credit MarketsDokument21 Seiten(Done) How Do Market Failures Justify Interventions in Rural Credit MarketsVadimNoch keine Bewertungen

- Name: Olufisayo Babalola Matric Number: 169025002 Course: Fin 913 Question: Discuss The Indices of Financial DevelopmentDokument14 SeitenName: Olufisayo Babalola Matric Number: 169025002 Course: Fin 913 Question: Discuss The Indices of Financial Developmentfisayobabs11Noch keine Bewertungen

- International Business Management QBDokument12 SeitenInternational Business Management QBAnonymous qAegy6GNoch keine Bewertungen

- Unit 5Dokument9 SeitenUnit 5EYOB AHMEDNoch keine Bewertungen

- Financial Crisis: (Type The Company Name)Dokument5 SeitenFinancial Crisis: (Type The Company Name)Rahul KrishnaNoch keine Bewertungen

- Coping With The Crisis: Policy Options For Emerging Market CountriesDokument30 SeitenCoping With The Crisis: Policy Options For Emerging Market CountriesLinh HoNoch keine Bewertungen

- Eco Dev MidtermDokument6 SeitenEco Dev MidtermGlenn VeluzNoch keine Bewertungen

- The Advantages of International RelationsDokument5 SeitenThe Advantages of International Relationsrafunzel nathalieNoch keine Bewertungen

- Financial InstitutionDokument17 SeitenFinancial InstitutionAbhishek JaiswalNoch keine Bewertungen

- Management of Financial InstitutionDokument172 SeitenManagement of Financial InstitutionNeo Nageshwar Das50% (2)

- Theoretical FrameworkDokument3 SeitenTheoretical FrameworkJanella VictorinoNoch keine Bewertungen

- Chapter 5Dokument7 SeitenChapter 5Tasebe GetachewNoch keine Bewertungen

- 6 Paul A. VolckerDokument4 Seiten6 Paul A. VolckerShweta PrabhuNoch keine Bewertungen

- Finance and Fiscal Policy For DevelopmentDokument7 SeitenFinance and Fiscal Policy For DevelopmentLouise Phillip Labing-isaNoch keine Bewertungen

- IMF Liquidity AnalysisDokument34 SeitenIMF Liquidity AnalysisjantaNoch keine Bewertungen

- Capital Accounts - Liberalize or Not PDFDokument3 SeitenCapital Accounts - Liberalize or Not PDFsiaaiaNoch keine Bewertungen

- Capital Control and The Liberal DiscourseDokument4 SeitenCapital Control and The Liberal DiscourseacarkayaNoch keine Bewertungen

- Trading in Illusions: by Dani Rodrik - March 1, 2001Dokument9 SeitenTrading in Illusions: by Dani Rodrik - March 1, 2001Justine Jireh PerezNoch keine Bewertungen

- Enspecial Series On Covid19monetary and Financial Policy Responses For Emerging Market and DevelopinDokument5 SeitenEnspecial Series On Covid19monetary and Financial Policy Responses For Emerging Market and DevelopinAlip FajarNoch keine Bewertungen

- 2007 Meltdown of Structured FinanceDokument41 Seiten2007 Meltdown of Structured FinancejodiebrittNoch keine Bewertungen

- Resume Regulation of Banking and Financial MarketsDokument10 SeitenResume Regulation of Banking and Financial Marketsoktavia dewiNoch keine Bewertungen

- CH 1 - Scope of International FinanceDokument7 SeitenCH 1 - Scope of International Financepritesh_baidya269100% (3)

- Exchange Rate DeterminationDokument5 SeitenExchange Rate DeterminationSakshi LodhaNoch keine Bewertungen

- Chapter Five The Regulation of Financial Markets and Institutions 5.1. The Nature of Financial System RegulationDokument7 SeitenChapter Five The Regulation of Financial Markets and Institutions 5.1. The Nature of Financial System RegulationWondimu TadesseNoch keine Bewertungen

- Political Fallouts and Resignations: A Deep Dive Into Financial ScandalsVon EverandPolitical Fallouts and Resignations: A Deep Dive Into Financial ScandalsNoch keine Bewertungen

- The Diplomatic Consequences of Secessionist MovementsVon EverandThe Diplomatic Consequences of Secessionist MovementsNoch keine Bewertungen

- Amriteeshwar - Rai (CV)Dokument2 SeitenAmriteeshwar - Rai (CV)Amriteshwar RaiNoch keine Bewertungen

- HDFC Core BankingDokument23 SeitenHDFC Core Bankingakash_shah_42Noch keine Bewertungen

- HDFC PDFDokument43 SeitenHDFC PDFAbhijit SahooNoch keine Bewertungen

- Repoprt On Loans & Advances PDFDokument66 SeitenRepoprt On Loans & Advances PDFTitas Manower50% (4)

- Project of Banking Law: Central University of South BiharDokument12 SeitenProject of Banking Law: Central University of South BiharAnjali SinhaNoch keine Bewertungen

- Loan and Security AgreementDokument51 SeitenLoan and Security Agreementbefaj44984100% (1)

- Swot AnalysisDokument5 SeitenSwot AnalysisZara KhanNoch keine Bewertungen

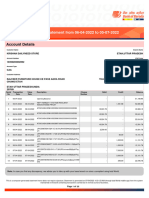

- Account StatementDokument83 SeitenAccount StatementAshwani KumarNoch keine Bewertungen

- Laws and Practice of General Banking (English) - LMPDokument35 SeitenLaws and Practice of General Banking (English) - LMPAshfia ZamanNoch keine Bewertungen

- 6-Cash Book Multiple Choice Questions With Answers PDFDokument14 Seiten6-Cash Book Multiple Choice Questions With Answers PDFHammadkhan Dj89Noch keine Bewertungen

- Black Book SiesDokument39 SeitenBlack Book SiesAmit Pandey100% (2)

- 03-Chapters - I-XIV Accounting ManualDokument115 Seiten03-Chapters - I-XIV Accounting ManualMarie AlejoNoch keine Bewertungen

- RAMCO - Bank ModuleDokument45 SeitenRAMCO - Bank ModuleMahdi AlaydrusNoch keine Bewertungen

- Final HBL PresentationDokument75 SeitenFinal HBL PresentationShehzaib Sunny100% (4)

- Assignment Meeting 7 (Rachel Gracia A021231082)Dokument5 SeitenAssignment Meeting 7 (Rachel Gracia A021231082)gantengenggar75Noch keine Bewertungen

- Centerview Partners January 2023 InternshipsDokument1 SeiteCenterview Partners January 2023 Internshipscharles alcaideNoch keine Bewertungen

- Shivankar Singh ResumeDokument3 SeitenShivankar Singh Resumeamanbhardwaj5Noch keine Bewertungen

- AP.3406 Audit of InvestmentsDokument5 SeitenAP.3406 Audit of InvestmentsMonica GarciaNoch keine Bewertungen

- Economy 1 PDFDokument163 SeitenEconomy 1 PDFAnil Kumar SudarsiNoch keine Bewertungen

- EBW SampleDokument8 SeitenEBW SampleArianna GarciaNoch keine Bewertungen

- Credit Card Master Circular PDFDokument29 SeitenCredit Card Master Circular PDFaNoch keine Bewertungen

- YES Prosperity Savings Account W.E.F. 1st March 2018 PDFDokument2 SeitenYES Prosperity Savings Account W.E.F. 1st March 2018 PDFJeyakumara Vel CNoch keine Bewertungen

- Schedule of Charges Fees and CommissionDokument10 SeitenSchedule of Charges Fees and CommissionAbdullah Al NomanNoch keine Bewertungen

- AK Gupta 4 PDFDokument38 SeitenAK Gupta 4 PDFकायथ रोहित100% (1)

- Neo BanksDokument10 SeitenNeo BanksanuclashofclanNoch keine Bewertungen

- Caiib Success Class-7 (BRBL Module-C Part-1) : 7 PM 6 Nov. 2023Dokument17 SeitenCaiib Success Class-7 (BRBL Module-C Part-1) : 7 PM 6 Nov. 2023Hari RajNoch keine Bewertungen

- Solution: (18,025 + 3,125 - 2,875 + 125) 18,400: Use The Following Information For The Next Three QuestionsDokument21 SeitenSolution: (18,025 + 3,125 - 2,875 + 125) 18,400: Use The Following Information For The Next Three QuestionsJovel Paycana100% (5)

- S4HANA Finance - Bank Account Management - NWBC - Without FioriDokument6 SeitenS4HANA Finance - Bank Account Management - NWBC - Without Fiorimannoj2001Noch keine Bewertungen

- 447096602-Preview-Falix-Pdf - BROWN +++Dokument5 Seiten447096602-Preview-Falix-Pdf - BROWN +++13KARATNoch keine Bewertungen

- CPFLMDokument4 SeitenCPFLMkyinekyineNoch keine Bewertungen