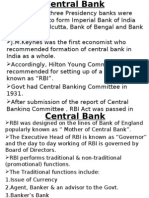

Das könnte Ihnen auch gefallen

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- Classification Banks NBFCsDokument16 SeitenClassification Banks NBFCsbhavyaNoch keine Bewertungen

- Banking India: Accepting Deposits for the Purpose of LendingVon EverandBanking India: Accepting Deposits for the Purpose of LendingNoch keine Bewertungen

- 03 Mrunal Economy Handout 2020Dokument43 Seiten03 Mrunal Economy Handout 2020Sicky SandilyaNoch keine Bewertungen

- Mrunal Handout 3 CSP20Dokument43 SeitenMrunal Handout 3 CSP20Margesh PatelNoch keine Bewertungen

- 03 Handouts Mrunal Economy Batch Code CSP20Dokument43 Seiten03 Handouts Mrunal Economy Batch Code CSP20dbiswajitNoch keine Bewertungen

- Module 5 BankingDokument42 SeitenModule 5 Bankingg.prasanna saiNoch keine Bewertungen

- Banking Law Notes PDFDokument64 SeitenBanking Law Notes PDFsoumya100% (2)

- Iare Birm Lecture NotesDokument188 SeitenIare Birm Lecture NotesSumit Kumar GautamNoch keine Bewertungen

- Unit-1 Introduction To Indian Banking SystemDokument40 SeitenUnit-1 Introduction To Indian Banking SystemKruti BhattNoch keine Bewertungen

- Structure of Indian BankingDokument12 SeitenStructure of Indian BankingYatin DhallNoch keine Bewertungen

- Assessments of BanksDokument94 SeitenAssessments of Bankskavita.m.yadavNoch keine Bewertungen

- Unit 1 BFSDokument83 SeitenUnit 1 BFSsyedmoin85Noch keine Bewertungen

- Welcome To IIBF's - JAIIB Virtual ClassesDokument63 SeitenWelcome To IIBF's - JAIIB Virtual ClassesGopinath KrishnanNoch keine Bewertungen

- Reserve Bank of IndiaDokument21 SeitenReserve Bank of IndiaAcchu BajajNoch keine Bewertungen

- Banking Unit 2Dokument10 SeitenBanking Unit 2queenboss lifestyleNoch keine Bewertungen

- Symbi Banking Lecture NotesDokument21 SeitenSymbi Banking Lecture NotesPankaj GahlawatNoch keine Bewertungen

- Role of RBI Under Banking Regulation Act, 1949Dokument5 SeitenRole of RBI Under Banking Regulation Act, 1949Jay Ram100% (1)

- Welcome To IIBF's - JAIIB Virtual Classes: K.ChockalingamDokument63 SeitenWelcome To IIBF's - JAIIB Virtual Classes: K.ChockalingamKunal PuriNoch keine Bewertungen

- Indian Banking Sector: BY Siddhant Jain 9595637843Dokument66 SeitenIndian Banking Sector: BY Siddhant Jain 9595637843sh_09708Noch keine Bewertungen

- Indian Banking SystemDokument36 SeitenIndian Banking SystemRohit Sharma100% (1)

- JAIIB - Principles and Practices of BankingDokument71 SeitenJAIIB - Principles and Practices of BankingKarthick Csk100% (8)

- Money and Banking System MBADokument29 SeitenMoney and Banking System MBABabasab Patil (Karrisatte)100% (1)

- Banking NotesDokument60 SeitenBanking NotesarunimaNoch keine Bewertungen

- Banking in IndiaDokument6 SeitenBanking in Indiajasim ansariNoch keine Bewertungen

- Role of RBI Under Banking Regulation Act, 1949Dokument11 SeitenRole of RBI Under Banking Regulation Act, 1949Jay Ram100% (1)

- Central BankDokument24 SeitenCentral BankShailesh RathodNoch keine Bewertungen

- Hamdard Institue of Legal Studies AND RESEARCH (2019-24)Dokument13 SeitenHamdard Institue of Legal Studies AND RESEARCH (2019-24)Ambreen ShamsiNoch keine Bewertungen

- Unit - 1: Introduction To Indian Banking SystemDokument109 SeitenUnit - 1: Introduction To Indian Banking SystemDr. S. Nellima KPRCAS-CommerceNoch keine Bewertungen

- Banking and Insurance Law Notes Part-2Dokument48 SeitenBanking and Insurance Law Notes Part-2Ridam GangwarNoch keine Bewertungen

- EF1B1 HDT Bank Classification PCB2Dokument26 SeitenEF1B1 HDT Bank Classification PCB2PrakritiRoyNoch keine Bewertungen

- Welcome To IIBF's - JAIIB Virtual Classes: K.ChockalingamDokument63 SeitenWelcome To IIBF's - JAIIB Virtual Classes: K.ChockalingamapoorvaNoch keine Bewertungen

- Central Bank Edit-1Dokument3 SeitenCentral Bank Edit-1Vanlalbiakdiki ChhangteNoch keine Bewertungen

- Project It in Bank-2Dokument66 SeitenProject It in Bank-2Rohan SoansNoch keine Bewertungen

- Indian Banking System Unit 1Dokument26 SeitenIndian Banking System Unit 1vandana kadamNoch keine Bewertungen

- RBFDokument8 SeitenRBFPankaj KamraNoch keine Bewertungen

- Module 3: Central BankDokument47 SeitenModule 3: Central Bankpoorvi agrawalNoch keine Bewertungen

- Banking and Financial Services: Unit 1Dokument48 SeitenBanking and Financial Services: Unit 1swarnalata JohnNoch keine Bewertungen

- Main WordDokument25 SeitenMain Wordvipul sutharNoch keine Bewertungen

- New Final ReportDokument33 SeitenNew Final Reportvarshinivars2223Noch keine Bewertungen

- Regulatory Framework of Financial ServicesDokument47 SeitenRegulatory Framework of Financial ServicesUrvashi Tody100% (3)

- 1 Banking System PDFDokument12 Seiten1 Banking System PDFNilu91Noch keine Bewertungen

- Banking System in IndiaDokument8 SeitenBanking System in IndiaShikha ShuklaNoch keine Bewertungen

- Retail Banking NotesDokument25 SeitenRetail Banking NotesTarun MaheshwariNoch keine Bewertungen

- The Law of Banking and The Negotiable Instruments: Marupaka Venkateshwarlu M.A, B.Ed, Llb. WWW - Thelegal.Co - inDokument14 SeitenThe Law of Banking and The Negotiable Instruments: Marupaka Venkateshwarlu M.A, B.Ed, Llb. WWW - Thelegal.Co - inDinakaar SNoch keine Bewertungen

- Project Report On The Reserve Bank of IndiaDokument64 SeitenProject Report On The Reserve Bank of IndiaAtharv VartakNoch keine Bewertungen

- Bank Ops PPT+Word Docs Unit 1-10Dokument39 SeitenBank Ops PPT+Word Docs Unit 1-10Anand PadhyeNoch keine Bewertungen

- Banking: History of Banking in IndiaDokument4 SeitenBanking: History of Banking in IndiatsfabmNoch keine Bewertungen

- History of Banking 5Dokument19 SeitenHistory of Banking 5Ravneet SinghNoch keine Bewertungen

- Seminar Presentation Write-Up: Prestige Institute of Management and Research, IndoreDokument29 SeitenSeminar Presentation Write-Up: Prestige Institute of Management and Research, IndoreSovran YadavNoch keine Bewertungen

- A Research Report On SbiDokument45 SeitenA Research Report On SbiSonu LovesforuNoch keine Bewertungen

- Banking System and Structure in India Evolution of Indian BanksDokument61 SeitenBanking System and Structure in India Evolution of Indian BanksTrilok IndiNoch keine Bewertungen

- 1 Banking SystemDokument12 Seiten1 Banking SystemkunalNoch keine Bewertungen

- Financial Institutions & MarketsDokument62 SeitenFinancial Institutions & MarketsSaurav UchilNoch keine Bewertungen

- Legal Framework of Banks in IndiaDokument18 SeitenLegal Framework of Banks in IndiaBinu.C.Kurian100% (1)

- Principles and Practice of BankingDokument27 SeitenPrinciples and Practice of Bankingrangudasar100% (2)

- Symbi Banking Lecture Notes 2012Dokument29 SeitenSymbi Banking Lecture Notes 2012Abhijit DeshpandeNoch keine Bewertungen

- Symbi Banking Lecture Notes 2012Dokument29 SeitenSymbi Banking Lecture Notes 2012Ankur ChauhanNoch keine Bewertungen

- Banking Financial Services Management: Ms. Jebakerupa Roslin Amirtharajan St. Joseph S College of Engineering MBADokument82 SeitenBanking Financial Services Management: Ms. Jebakerupa Roslin Amirtharajan St. Joseph S College of Engineering MBASvijayakanthan SelvarajNoch keine Bewertungen

- 26AprilIYER MOD-ADokument23 Seiten26AprilIYER MOD-AvardhinikumarNoch keine Bewertungen

- Important Banking Financial Terms For RBI Grade B Phase II NABARD DA Mains IBPS PO Mains PDFDokument21 SeitenImportant Banking Financial Terms For RBI Grade B Phase II NABARD DA Mains IBPS PO Mains PDFk vinayNoch keine Bewertungen

- IBPS ClerksIII Quick Reference GuideDokument54 SeitenIBPS ClerksIII Quick Reference GuideVivek Chand DubeyNoch keine Bewertungen

- Assignment 1Dokument12 SeitenAssignment 1Rajusingh RajpurohitNoch keine Bewertungen

- Sid DateDokument26 SeitenSid Datesunilsaran7892Noch keine Bewertungen

- Module 1Dokument5 SeitenModule 1Prajwal VasukiNoch keine Bewertungen

- Financial Inclusion Bank of Baroda: Summer Training Project ReportDokument102 SeitenFinancial Inclusion Bank of Baroda: Summer Training Project ReportHashmi SutariyaNoch keine Bewertungen

- March-April - The Indian Down UnderDokument60 SeitenMarch-April - The Indian Down UnderindiandownunderNoch keine Bewertungen

- Tamil Nadu National Law University: Course ObjectivesDokument4 SeitenTamil Nadu National Law University: Course ObjectivessriprasadNoch keine Bewertungen

- The Ketan Parekh Scam - Free Management Articles - Free Management Case Studies PDFDokument2 SeitenThe Ketan Parekh Scam - Free Management Articles - Free Management Case Studies PDFkimmiahujaNoch keine Bewertungen

- Mockstock News SlidesDokument20 SeitenMockstock News SlidesShubham VermaNoch keine Bewertungen

- RBI Working Paper No. 05/2019: Term Premium Spillover From The US To Indian MarketsDokument1 SeiteRBI Working Paper No. 05/2019: Term Premium Spillover From The US To Indian MarketsVasu Ram JayanthNoch keine Bewertungen

- Summer Internship ProjectDokument51 SeitenSummer Internship ProjectMahesh SatapathyNoch keine Bewertungen

- Mergers & Acquisitions HDFC-CBOP FinalDokument28 SeitenMergers & Acquisitions HDFC-CBOP Finalkrishna_bmsNoch keine Bewertungen

- SEBI On ReligareDokument29 SeitenSEBI On Religarevibha100% (1)

- RBI Act 1934 NDokument42 SeitenRBI Act 1934 NRohit SinghNoch keine Bewertungen

- GAR Point WiseDokument9 SeitenGAR Point WiseRAKESH100% (3)

- Merchant Banking in IndiaDokument55 SeitenMerchant Banking in IndiaMihir DeliwalaNoch keine Bewertungen

- Bond Market in IndiaDokument13 SeitenBond Market in Indiafernandesroshandaniel4962100% (1)

- Hexatech Global Sample Report12Dokument24 SeitenHexatech Global Sample Report12HexaTech GlobalNoch keine Bewertungen

- Financial Inclusion Using Pradhan Mantri Jan-Dhan Yojana - A Conceptual StudyDokument12 SeitenFinancial Inclusion Using Pradhan Mantri Jan-Dhan Yojana - A Conceptual StudyabhaybittuNoch keine Bewertungen

- A Critical Review of NPA in Indian Banking IndustryDokument12 SeitenA Critical Review of NPA in Indian Banking IndustryNavneet NandaNoch keine Bewertungen

- Final Project Report On Au Fin. JaipurDokument71 SeitenFinal Project Report On Au Fin. Jaipurkapiljjn100% (1)

- INTERNATIONAL BANKING - FOREX MANAGEMENT - BCOM 5 Sem Ebook and NotesDokument31 SeitenINTERNATIONAL BANKING - FOREX MANAGEMENT - BCOM 5 Sem Ebook and NotesMohammed Muzzamil82% (22)

- Q3FY24 TranscriptDokument21 SeitenQ3FY24 TranscriptAshu KumarNoch keine Bewertungen

- Role of Rbi & SebiDokument6 SeitenRole of Rbi & Sebiabhiarora07Noch keine Bewertungen

- Project On SBI BankDokument48 SeitenProject On SBI BankArvind Mahandhwal80% (5)

- Credit Audit FormatDokument14 SeitenCredit Audit FormatRAGAVINoch keine Bewertungen

- Services Marketing NotesDokument96 SeitenServices Marketing NotesKarthikNoch keine Bewertungen

- Debt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Dokument3 SeitenDebt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Kunwar AbhudayNoch keine Bewertungen

- LTMF Fy10Dokument44 SeitenLTMF Fy10Divisha_Jha_1529Noch keine Bewertungen