Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- ELEC2 - Module 2 - Asset Based ValuationDokument27 SeitenELEC2 - Module 2 - Asset Based ValuationMaricar Pineda100% (1)

- Mercury Athletic Footwear - Valuing The Opportunity: FINS 3625 - Case Study Written ComponentDokument9 SeitenMercury Athletic Footwear - Valuing The Opportunity: FINS 3625 - Case Study Written ComponentBharat KoiralaNoch keine Bewertungen

- PWC Basics of Mining Accounting UsDokument133 SeitenPWC Basics of Mining Accounting Ussharanabasappa baliger100% (1)

- Intermediate Accounting 15th Edition Kieso Test Bank 1Dokument48 SeitenIntermediate Accounting 15th Edition Kieso Test Bank 1pauline100% (40)

- IMF Madura Chapter 01 PDFDokument27 SeitenIMF Madura Chapter 01 PDFMushfiq RafidNoch keine Bewertungen

- Bank ValuationDokument9 SeitenBank ValuationHarshil SinghalNoch keine Bewertungen

- CreateReportSAPTreas Risk MGTDokument159 SeitenCreateReportSAPTreas Risk MGTDevendra HajareNoch keine Bewertungen

- Statement On Accounting Theory and Theory AcceptanceDokument36 SeitenStatement On Accounting Theory and Theory AcceptanceAprilia Suandi100% (3)

- Calendar Effects in US Stock MarketsDokument26 SeitenCalendar Effects in US Stock MarketsMickey KoenNoch keine Bewertungen

- M10Dokument61 SeitenM10Mickey KoenNoch keine Bewertungen

- Call For A Little Extra:: A Study of How People Make Sense of An Organizational Change InitiativeDokument90 SeitenCall For A Little Extra:: A Study of How People Make Sense of An Organizational Change InitiativeMickey KoenNoch keine Bewertungen

- Calendar Effects in Global Markets: An Empirical Study (1987-2006)Dokument54 SeitenCalendar Effects in Global Markets: An Empirical Study (1987-2006)Mickey KoenNoch keine Bewertungen

- M&A Deals During A Financial CrisisDokument50 SeitenM&A Deals During A Financial CrisisMickey KoenNoch keine Bewertungen

- M23Dokument98 SeitenM23Mickey KoenNoch keine Bewertungen

- Calendar Anomalies in The Foreign Exchange MarketDokument31 SeitenCalendar Anomalies in The Foreign Exchange MarketMickey KoenNoch keine Bewertungen

- Calendar Effects and Foreign Exchange MarketsDokument55 SeitenCalendar Effects and Foreign Exchange MarketsMickey KoenNoch keine Bewertungen

- C8 PDFDokument76 SeitenC8 PDFMickey KoenNoch keine Bewertungen

- Academic Paper: M&As, Industry Structure and M&A PerformanceDokument48 SeitenAcademic Paper: M&As, Industry Structure and M&A PerformanceMickey KoenNoch keine Bewertungen

- Calculation of First Sales ForecastsDokument29 SeitenCalculation of First Sales ForecastsMickey KoenNoch keine Bewertungen

- Master Thesis: M.Sc. in Business Administration With A Specialization in "Strategy and Organization"Dokument56 SeitenMaster Thesis: M.Sc. in Business Administration With A Specialization in "Strategy and Organization"Mickey KoenNoch keine Bewertungen

- M&A waves in the US - comparing the 5th and 6th wavesDokument43 SeitenM&A waves in the US - comparing the 5th and 6th wavesMickey KoenNoch keine Bewertungen

- M6Dokument57 SeitenM6Mickey KoenNoch keine Bewertungen

- M-Commerce:: Effects of Mobile Perceived Convenience and Enjoyment On The Mobile Purchase IntentionDokument48 SeitenM-Commerce:: Effects of Mobile Perceived Convenience and Enjoyment On The Mobile Purchase IntentionMickey KoenNoch keine Bewertungen

- M&A integration approaches along industry life cyclesDokument37 SeitenM&A integration approaches along industry life cyclesMickey KoenNoch keine Bewertungen

- R&D Alliance Governance: A Cultural Perspective: Bachelor ThesisDokument24 SeitenR&D Alliance Governance: A Cultural Perspective: Bachelor ThesisMickey KoenNoch keine Bewertungen

- M2Dokument37 SeitenM2Mickey KoenNoch keine Bewertungen

- Just Bought A New #Gucci Handbag: Study About eWOM and Impression Management On InstagramDokument92 SeitenJust Bought A New #Gucci Handbag: Study About eWOM and Impression Management On InstagramMickey KoenNoch keine Bewertungen

- The 1737 UN Sanctions Regime: Lawful or A Political Move?Dokument137 SeitenThe 1737 UN Sanctions Regime: Lawful or A Political Move?Mickey KoenNoch keine Bewertungen

- R&D Driven Innovation in Emerging Markets: The Moderating Role of Institutional VoidsDokument39 SeitenR&D Driven Innovation in Emerging Markets: The Moderating Role of Institutional VoidsMickey KoenNoch keine Bewertungen

- WEEK SIX Bond Valuation Part-2Dokument12 SeitenWEEK SIX Bond Valuation Part-2kazi A.R RafiNoch keine Bewertungen

- BIWS Courses Resume InstructionsDokument13 SeitenBIWS Courses Resume InstructionsClaptrapjackNoch keine Bewertungen

- Chapter Four StockDokument16 SeitenChapter Four Stockሔርሞን ይድነቃቸው100% (1)

- Test Bank For Principles of Managerial Finance Arab World Edition Pack Lawrence J Gitman Chad J Zutter Wajeeh Elali Amer Al Roubaie 2Dokument35 SeitenTest Bank For Principles of Managerial Finance Arab World Edition Pack Lawrence J Gitman Chad J Zutter Wajeeh Elali Amer Al Roubaie 2bibberbombycid.p13z100% (38)

- Karnataka Iron Ore Mine AuctionDokument106 SeitenKarnataka Iron Ore Mine AuctionRachit Kumar StudentNoch keine Bewertungen

- Government Bonds Bond - IN0020190362 Bond - IN0020170026Dokument4 SeitenGovernment Bonds Bond - IN0020190362 Bond - IN0020170026Arif AhmedNoch keine Bewertungen

- Valuation of SharesDokument10 SeitenValuation of SharesMeraj HassanNoch keine Bewertungen

- WMUU Poultry Newcomer OutlookDokument18 SeitenWMUU Poultry Newcomer OutlookVictorioNoch keine Bewertungen

- Professional Stock Market Training Course by Shakti Shiromani ShuklaDokument12 SeitenProfessional Stock Market Training Course by Shakti Shiromani ShuklaShakti ShuklaNoch keine Bewertungen

- QEIC Tech - CGI Group Pitch - FinalDokument16 SeitenQEIC Tech - CGI Group Pitch - FinalAnonymous Ht0MIJNoch keine Bewertungen

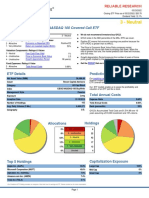

- 3 - Neutral: Global X Funds: Global X NASDAQ 100 Covered Call ETFDokument3 Seiten3 - Neutral: Global X Funds: Global X NASDAQ 100 Covered Call ETFphysicallen1791Noch keine Bewertungen

- 300Dokument26 Seiten300Rinni JainNoch keine Bewertungen

- Cost of Capital FYBAF Sem I Old F. M. 1644486598Dokument26 SeitenCost of Capital FYBAF Sem I Old F. M. 1644486598maggiemali092Noch keine Bewertungen

- Term Net Premium Reserve (NPR) Calculation: by Tim Cardinal, FSA, CERA, MAAA Principal, Actuarial CompassDokument6 SeitenTerm Net Premium Reserve (NPR) Calculation: by Tim Cardinal, FSA, CERA, MAAA Principal, Actuarial Compassswatisin93Noch keine Bewertungen

- Chapter 2 Fair Value Measurement IFRS 13Dokument21 SeitenChapter 2 Fair Value Measurement IFRS 13johnegnNoch keine Bewertungen

- Auditing Assurance MCQ B Com SDokument26 SeitenAuditing Assurance MCQ B Com SBhavan YadavNoch keine Bewertungen

- Marcato Capital - Letter To Lifetime Fitness BoardDokument13 SeitenMarcato Capital - Letter To Lifetime Fitness BoardCanadianValueNoch keine Bewertungen

- VALUATION GUIDELINES LAID BY HIGH COURTSDokument48 SeitenVALUATION GUIDELINES LAID BY HIGH COURTSdevNoch keine Bewertungen

- Pricing and Hedging Electricity Supply Contracts ADokument39 SeitenPricing and Hedging Electricity Supply Contracts AAldimIrfaniVikriNoch keine Bewertungen

- Calculate ending inventory using Retail Inventory MethodDokument3 SeitenCalculate ending inventory using Retail Inventory MethodHasanah BalatifNoch keine Bewertungen

- 2019 Year in Review: Key Southeast Asian startup trends and investmentsDokument57 Seiten2019 Year in Review: Key Southeast Asian startup trends and investmentsMark Del RosarioNoch keine Bewertungen

- Tata Corus DealDokument39 SeitenTata Corus DealdhavalkurveyNoch keine Bewertungen