Das könnte Ihnen auch gefallen

- Review of The Accounting Process Problems 2-1. (Tiger Company)Dokument5 SeitenReview of The Accounting Process Problems 2-1. (Tiger Company)Pauline Kisha CastroNoch keine Bewertungen

- Review of The Accounting Process Problems 2-1. (Tiger Company)Dokument5 SeitenReview of The Accounting Process Problems 2-1. (Tiger Company)Joana MagtuboNoch keine Bewertungen

- Review of The Accounting Process Problems 2-1. (Tiger Company)Dokument5 SeitenReview of The Accounting Process Problems 2-1. (Tiger Company)HohohoNoch keine Bewertungen

- Chapter 7Dokument18 SeitenChapter 7Din Rose Gonzales0% (1)

- Date Description PR Debit Credit Dec - 31 1. Prepaid InsuranceDokument4 SeitenDate Description PR Debit Credit Dec - 31 1. Prepaid InsuranceJackie EasterNoch keine Bewertungen

- Chapter 7Dokument18 SeitenChapter 7Francesz VirayNoch keine Bewertungen

- FIRST PB FAR Solutions PDFDokument6 SeitenFIRST PB FAR Solutions PDFStephanie Joy NogollosNoch keine Bewertungen

- Chapter 13 (Incomplete)Dokument22 SeitenChapter 13 (Incomplete)Dan ChuaNoch keine Bewertungen

- FAR Problem Quiz 2Dokument3 SeitenFAR Problem Quiz 2Ednalyn CruzNoch keine Bewertungen

- F7 - Mock A - AnswersDokument6 SeitenF7 - Mock A - AnswerspavishneNoch keine Bewertungen

- Chapter 10Dokument22 SeitenChapter 10Dan ChuaNoch keine Bewertungen

- AC3202 WK2 Exercises SolutionsDokument11 SeitenAC3202 WK2 Exercises SolutionsLong LongNoch keine Bewertungen

- Activity #6Dokument20 SeitenActivity #6JEWELL ANN PENARANDANoch keine Bewertungen

- Audit of Liabilities Answer KeyDokument2 SeitenAudit of Liabilities Answer KeyLyca MaeNoch keine Bewertungen

- Module 1 - Seatwork Answer KeyDokument3 SeitenModule 1 - Seatwork Answer KeyKATHRYN CLAUDETTE RESENTENoch keine Bewertungen

- Jay Cesar System Developer Worksheet DECEMBER 31 2019 Unadjusted Trial Balance REFDokument4 SeitenJay Cesar System Developer Worksheet DECEMBER 31 2019 Unadjusted Trial Balance REFAdam CuencaNoch keine Bewertungen

- Siklus AkuntansiDokument15 SeitenSiklus AkuntansiBachrul AlamNoch keine Bewertungen

- Abdirahman Assign 1Dokument8 SeitenAbdirahman Assign 1Mazlax YareNoch keine Bewertungen

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDokument7 SeitenSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

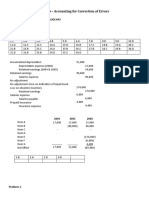

- Unit 4 - Accounting For Correction of Errors: Cabueñas, Brenton C. Bsa - 3 Audcap2 Problem 1 AnswersDokument14 SeitenUnit 4 - Accounting For Correction of Errors: Cabueñas, Brenton C. Bsa - 3 Audcap2 Problem 1 AnswersSel BarrantesNoch keine Bewertungen

- Jawaban Soal UTS Akuntansi Keu - MenengahDokument4 SeitenJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNoch keine Bewertungen

- Tum CompanyDokument4 SeitenTum CompanyNguyen My Khanh (K18 HCM)Noch keine Bewertungen

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDokument7 SeitenSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNoch keine Bewertungen

- FAR Final Preboard SolutionsDokument6 SeitenFAR Final Preboard SolutionsVillanueva, Mariella De VeraNoch keine Bewertungen

- Accountancy 12 - DS2 - Set - 1Dokument15 SeitenAccountancy 12 - DS2 - Set - 1Deepa Saravana KumarNoch keine Bewertungen

- Practice Exercises - Note PayableDokument2 SeitenPractice Exercises - Note PayableShane TabunggaoNoch keine Bewertungen

- Problem 8, 9, 14Dokument5 SeitenProblem 8, 9, 14Margarette Novem T. PaulinNoch keine Bewertungen

- Property, Plant, & Equipment Problem SetDokument3 SeitenProperty, Plant, & Equipment Problem SetSarah Nicole S. LagrimasNoch keine Bewertungen

- Quiz 9 FinacrDokument9 SeitenQuiz 9 FinacrJen Ner100% (5)

- QUIZ 9 fINACRDokument9 SeitenQUIZ 9 fINACRJen NerNoch keine Bewertungen

- Ia Forcadela Part IIIDokument5 SeitenIa Forcadela Part IIIMary Joanne forcadelaNoch keine Bewertungen

- Ia2 Ka & SolDokument31 SeitenIa2 Ka & SolCarlah Jeane BasinaNoch keine Bewertungen

- FAR Problem Quiz 1 SolDokument3 SeitenFAR Problem Quiz 1 SolEdnalyn CruzNoch keine Bewertungen

- Baysa ParcorChapter 1-5 Answer KeyDokument52 SeitenBaysa ParcorChapter 1-5 Answer KeymoonjianneNoch keine Bewertungen

- APC Ch1solDokument7 SeitenAPC Ch1solAnonymous LusWvyNoch keine Bewertungen

- CPAR B94 TAX Final PB Exam - Answers - SolutionsDokument12 SeitenCPAR B94 TAX Final PB Exam - Answers - SolutionsSilver LilyNoch keine Bewertungen

- Chapter 09Dokument12 SeitenChapter 09Dan ChuaNoch keine Bewertungen

- Batch 93 FAR First Preboard February 2023 - SolutionDokument5 SeitenBatch 93 FAR First Preboard February 2023 - SolutionlorenzNoch keine Bewertungen

- Chapter 10 - Cash To Accrual Basis of AccountingDokument3 SeitenChapter 10 - Cash To Accrual Basis of AccountingJEFFERSON CUTENoch keine Bewertungen

- Chapter 10 - Cash To Accrual Basis of AccountingDokument3 SeitenChapter 10 - Cash To Accrual Basis of AccountingXienaNoch keine Bewertungen

- GE 01.FCAB - .L Solution JUNE 2020 ExamDokument5 SeitenGE 01.FCAB - .L Solution JUNE 2020 ExamTameemmahmud rokibNoch keine Bewertungen

- Nguyen My Khanh - 25 - Mc1802Dokument6 SeitenNguyen My Khanh - 25 - Mc1802Biên KimNoch keine Bewertungen

- Homework SolutionsDokument5 SeitenHomework SolutionsAnonymous CuUAaRSNNoch keine Bewertungen

- Sol. Man. - Chapter 7 - Notes (Part 1)Dokument13 SeitenSol. Man. - Chapter 7 - Notes (Part 1)natalie clyde matesNoch keine Bewertungen

- Intermediate Accounting 2 Millan 221013 124345Dokument233 SeitenIntermediate Accounting 2 Millan 221013 124345Krazy Butterfly100% (1)

- Emilio Aguinaldo College - Cavite Campus School of Business AdministrationDokument9 SeitenEmilio Aguinaldo College - Cavite Campus School of Business AdministrationKarlayaanNoch keine Bewertungen

- Module 2Dokument81 SeitenModule 2Arra StypayhorliksonNoch keine Bewertungen

- 6 AccountingDokument5 Seiten6 AccountingRenz MoralesNoch keine Bewertungen

- (Chapter 1) Sol Man Intermediate Accounting 2 by Zeus MillanDokument8 Seiten(Chapter 1) Sol Man Intermediate Accounting 2 by Zeus MillanJonathan Villazon Rosales67% (3)

- Acctg 4 Serdan Quiz 3Dokument7 SeitenAcctg 4 Serdan Quiz 3Rica CatanguiNoch keine Bewertungen

- Chapter 1 - Contingent LiabilitiesDokument6 SeitenChapter 1 - Contingent LiabilitiesJoshua AbanalesNoch keine Bewertungen

- Sol. Man. - Chapter 1 - The Accounting Process - Ia Part 1a - 2020 EditionDokument12 SeitenSol. Man. - Chapter 1 - The Accounting Process - Ia Part 1a - 2020 EditionCharlene Mae MalaluanNoch keine Bewertungen

- Taxation Final Pre-Board - SolutionsDokument14 SeitenTaxation Final Pre-Board - SolutionsMischievous MaeNoch keine Bewertungen

- Gov't Grant, Depreciation, Revaluation and ImpairmentDokument6 SeitenGov't Grant, Depreciation, Revaluation and Impairment夜晨曦Noch keine Bewertungen

- Schaum's Outline of Principles of Accounting I, Fifth EditionVon EverandSchaum's Outline of Principles of Accounting I, Fifth EditionBewertung: 5 von 5 Sternen5/5 (3)

- Discounted Cash Flow: A Theory of the Valuation of FirmsVon EverandDiscounted Cash Flow: A Theory of the Valuation of FirmsNoch keine Bewertungen

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsVon EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNoch keine Bewertungen

- Forest Products: Advanced Technologies and Economic AnalysesVon EverandForest Products: Advanced Technologies and Economic AnalysesNoch keine Bewertungen

- VB - Chapter 8Dokument26 SeitenVB - Chapter 8Lian Blakely CousinNoch keine Bewertungen

- Untitled DocumentDokument5 SeitenUntitled DocumentLian Blakely CousinNoch keine Bewertungen

- Variable Costing: This Accounting Materials Are Brought To You byDokument18 SeitenVariable Costing: This Accounting Materials Are Brought To You byjeodhyNoch keine Bewertungen

- Christology and Discipleship (RELED 12) : The Study of Christ and His TeachingsDokument43 SeitenChristology and Discipleship (RELED 12) : The Study of Christ and His TeachingsLian Blakely CousinNoch keine Bewertungen

- Untitled DocumentDokument1 SeiteUntitled DocumentLian Blakely CousinNoch keine Bewertungen

- Exorcism As Psychotherapy: A Clinical Psychologist Examines So-Called Demonic PossessionDokument2 SeitenExorcism As Psychotherapy: A Clinical Psychologist Examines So-Called Demonic PossessionLian Blakely CousinNoch keine Bewertungen

- The AngelusDokument3 SeitenThe AngelusLian Blakely CousinNoch keine Bewertungen

- Cepillo and Medalla's CritiqueDokument1 SeiteCepillo and Medalla's CritiqueLian Blakely CousinNoch keine Bewertungen

- Michael Porter's: Five Forces ModelDokument17 SeitenMichael Porter's: Five Forces ModelLian Blakely CousinNoch keine Bewertungen

- Audit Program PURCH 01.28.11Dokument15 SeitenAudit Program PURCH 01.28.11Lian Blakely CousinNoch keine Bewertungen

- NameDokument2 SeitenNameLian Blakely CousinNoch keine Bewertungen

- PAL 17A Mar2011Dokument126 SeitenPAL 17A Mar2011Lian Blakely CousinNoch keine Bewertungen

- Working Capital FinanceDokument12 SeitenWorking Capital FinanceYeoh Mae100% (4)

- Working Capital FinanceDokument12 SeitenWorking Capital FinanceYeoh Mae100% (4)

- CH 8 AnswersDokument7 SeitenCH 8 AnswersLian Blakely CousinNoch keine Bewertungen

- CH 1 AnswersDokument2 SeitenCH 1 AnswersRonel BuhayNoch keine Bewertungen

- SolMan Finacc Ch10Dokument2 SeitenSolMan Finacc Ch10Pauline Kisha CastroNoch keine Bewertungen

- Answers 2014 Vol 3 CH 5Dokument6 SeitenAnswers 2014 Vol 3 CH 5El YangNoch keine Bewertungen

- Answers 2014 Vol 3 CH 4 PDFDokument8 SeitenAnswers 2014 Vol 3 CH 4 PDFLian Blakely CousinNoch keine Bewertungen

- CH 7 AnswersDokument5 SeitenCH 7 Answersthenikkitr0% (1)

- Answers 2014 Vol 3 CH 5Dokument6 SeitenAnswers 2014 Vol 3 CH 5El YangNoch keine Bewertungen

- Answers 2014 Vol 3 CH 5Dokument6 SeitenAnswers 2014 Vol 3 CH 5El YangNoch keine Bewertungen

- CircuitsDokument27 SeitenCircuitsLian Blakely CousinNoch keine Bewertungen

- Appendix 79 - Instructions - QRBADokument1 SeiteAppendix 79 - Instructions - QRBALian Blakely CousinNoch keine Bewertungen

- SolMan Finacc Ch10Dokument2 SeitenSolMan Finacc Ch10Pauline Kisha CastroNoch keine Bewertungen

- OM Chapter 15Dokument26 SeitenOM Chapter 15Lian Blakely CousinNoch keine Bewertungen

- Appendix 7B - Instructions - RROR - L or F Funded, DFGFDokument1 SeiteAppendix 7B - Instructions - RROR - L or F Funded, DFGFTesa GDNoch keine Bewertungen

- Appendix 1 - Instructions - GJDokument1 SeiteAppendix 1 - Instructions - GJLian Blakely CousinNoch keine Bewertungen

- Form Lab 25 Goal StrategyDokument6 SeitenForm Lab 25 Goal StrategyGenti MadhiNoch keine Bewertungen

- Vacational SchoolDokument11 SeitenVacational SchoolPatrick ArazoNoch keine Bewertungen

- Goldsikka Digital Gold PlanDokument2 SeitenGoldsikka Digital Gold PlanAravind KumarNoch keine Bewertungen

- 3 PLDokument6 Seiten3 PLAbhishek7705Noch keine Bewertungen

- Understanding Financial Highlights in The Financial Statements of Hedge FundsDokument3 SeitenUnderstanding Financial Highlights in The Financial Statements of Hedge Fundssoumyac100% (1)

- Another Exam IIDokument5 SeitenAnother Exam IIzaqmkoNoch keine Bewertungen

- Macroeconomics - Staicu&PopescuDokument155 SeitenMacroeconomics - Staicu&PopescuŞtefania Alice100% (1)

- 098765Dokument23 Seiten098765HadjieLimNoch keine Bewertungen

- 16 BibliographyDokument22 Seiten16 BibliographyANJALI JAMESNoch keine Bewertungen

- Marubetting CaseDokument7 SeitenMarubetting CaseNiteshNoch keine Bewertungen

- US Internal Revenue Service: p946 - 2005Dokument110 SeitenUS Internal Revenue Service: p946 - 2005IRSNoch keine Bewertungen

- Riksbanken Nat UpplagaDokument528 SeitenRiksbanken Nat UpplagaOscar Ubeda SegmarNoch keine Bewertungen

- 470 Capsim NotesDokument2 Seiten470 Capsim NoteschomkaNoch keine Bewertungen

- MR DiyDokument2 SeitenMR DiySyamala 29Noch keine Bewertungen

- Oil Special Report - A Post-Sanctions WorldDokument15 SeitenOil Special Report - A Post-Sanctions WorldasaNoch keine Bewertungen

- 16 Volatility SmilesDokument15 Seiten16 Volatility SmilesGDFGDFererreerNoch keine Bewertungen

- M3 Business Engine Data Model IntroductionDokument58 SeitenM3 Business Engine Data Model IntroductionVINEETH100% (2)

- Confusion Is Not Radical v2Dokument29 SeitenConfusion Is Not Radical v2LudovicoNoch keine Bewertungen

- Apollo TyresDokument37 SeitenApollo TyresBandaru NarendrababuNoch keine Bewertungen

- 8-Inventory EstimationDokument5 Seiten8-Inventory EstimationYulrir Alesteyr HiroshiNoch keine Bewertungen

- AdEspresso The DOs and DONTs of Facebook Ads 2017Dokument37 SeitenAdEspresso The DOs and DONTs of Facebook Ads 2017Soumil KuraniNoch keine Bewertungen

- Comparative Analysis of Retail Value Proposition of Caprese and BaggitDokument18 SeitenComparative Analysis of Retail Value Proposition of Caprese and Baggitshona75Noch keine Bewertungen

- Ranara Vs Los AngelesDokument2 SeitenRanara Vs Los Angelesjef comendadorNoch keine Bewertungen

- Merger StrategyDokument23 SeitenMerger Strategypurple0123Noch keine Bewertungen

- Bacostmx-3tay2021-Quiz 2Dokument9 SeitenBacostmx-3tay2021-Quiz 2Marjorie NepomucenoNoch keine Bewertungen

- IFRS 15 (Questions)Dokument9 SeitenIFRS 15 (Questions)adeelkacaNoch keine Bewertungen

- Kinked Demand Curve and Keynesian TheoryDokument7 SeitenKinked Demand Curve and Keynesian TheoryAnshita GargNoch keine Bewertungen

- Price Action Part 2Dokument41 SeitenPrice Action Part 2imad ali100% (1)

- Managerial Accounting - Assignment (1) - Model AnswerDokument3 SeitenManagerial Accounting - Assignment (1) - Model AnswerHaytham NasefNoch keine Bewertungen

- Chapter # 22Dokument46 SeitenChapter # 22Adil AliNoch keine Bewertungen