Das könnte Ihnen auch gefallen

- Wake Up and Smell The CoffeeDokument6 SeitenWake Up and Smell The CoffeeAeyNoch keine Bewertungen

- Principles of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryDokument7 SeitenPrinciples of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryWarriach WarriachNoch keine Bewertungen

- Additional Mathemarics Project Work 3 2010Dokument6 SeitenAdditional Mathemarics Project Work 3 2010PeNgHoOi0% (1)

- UntitledDokument7 SeitenUntitledlulu luvelyNoch keine Bewertungen

- Which Annuity Is Better To Receive at 9% Pa Interest? Time A1 A2 A3 t1 100 50 150 t2 100 50 150 t3 100 50 t4 50 t5 50 t6 50Dokument22 SeitenWhich Annuity Is Better To Receive at 9% Pa Interest? Time A1 A2 A3 t1 100 50 150 t2 100 50 150 t3 100 50 t4 50 t5 50 t6 50shashank jaiswalNoch keine Bewertungen

- Activity 2Dokument6 SeitenActivity 2Jeanette AndoNoch keine Bewertungen

- BTDokument6 SeitenBTthanhlong2692000Noch keine Bewertungen

- Mock Test SolutionsDokument11 SeitenMock Test SolutionsMyraNoch keine Bewertungen

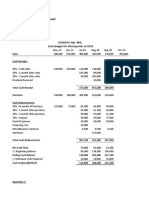

- Q3a. Capital Budget AssignmentDokument1 SeiteQ3a. Capital Budget AssignmentMorgan MunyoroNoch keine Bewertungen

- Benefits. by of Sales: 2020. SuperannuationDokument1 SeiteBenefits. by of Sales: 2020. SuperannuationArya RoshanNoch keine Bewertungen

- ParCor Chapter 3 - Hernandez - BSA 1-1 PDFDokument11 SeitenParCor Chapter 3 - Hernandez - BSA 1-1 PDFBSA 1-1Noch keine Bewertungen

- Module 8 - Answer KeyDokument3 SeitenModule 8 - Answer KeyFiona MiralpesNoch keine Bewertungen

- Chapter 9 Taxation of CorporationsDokument4 SeitenChapter 9 Taxation of CorporationsElizabethNoch keine Bewertungen

- M12 Tax ActivityDokument6 SeitenM12 Tax ActivityJanna RodriguezNoch keine Bewertungen

- BONDS explainedDokument14 SeitenBONDS explainedAlie Dys100% (1)

- Test 1 (2019672728) (NBF2D)Dokument5 SeitenTest 1 (2019672728) (NBF2D)Masnur Aina Md RajehNoch keine Bewertungen

- PROBLEM SOLUTIONSDokument6 SeitenPROBLEM SOLUTIONSLovenia M. FerrerNoch keine Bewertungen

- Taxation Income From SalaryDokument13 SeitenTaxation Income From SalarySajid AhmedNoch keine Bewertungen

- Taxation of Income of Partnership-1 - 034114Dokument6 SeitenTaxation of Income of Partnership-1 - 034114temiladeadeyemi11Noch keine Bewertungen

- St. Paul University Surigao: Engineering EconomyDokument8 SeitenSt. Paul University Surigao: Engineering EconomyMa.Elizabeth HernandezNoch keine Bewertungen

- Corrections: Suggested SolutionDokument5 SeitenCorrections: Suggested SolutionZairah FranciscoNoch keine Bewertungen

- AnnuityDokument5 SeitenAnnuityApril Joy Obedoza100% (1)

- 1.1.1 Tax On Income From Employment / Personal Income Tax: Direct TaxesDokument6 Seiten1.1.1 Tax On Income From Employment / Personal Income Tax: Direct TaxesGetu WeyessaNoch keine Bewertungen

- Financial Management 1Dokument8 SeitenFinancial Management 1KaranNoch keine Bewertungen

- IA-2-FINAL-EXAM-ANSWER-KEYDokument17 SeitenIA-2-FINAL-EXAM-ANSWER-KEYIrene Grace Edralin AdenaNoch keine Bewertungen

- AssignmentDokument9 SeitenAssignmentBaekhunnie ByunNoch keine Bewertungen

- SSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077Dokument29 SeitenSSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077samNoch keine Bewertungen

- Note On Tax Rebate On Takaful Contribution 2019 20 Other Than SalariedDokument1 SeiteNote On Tax Rebate On Takaful Contribution 2019 20 Other Than Salariedsyed aamir shahNoch keine Bewertungen

- Discussions Updated 24.03Dokument28 SeitenDiscussions Updated 24.03rajawatswadheentaNoch keine Bewertungen

- Solution SalariesDokument16 SeitenSolution SalariesAniket AgrawalNoch keine Bewertungen

- Income Taxes SolutionsDokument1 SeiteIncome Taxes SolutionsSleepy marshmallowNoch keine Bewertungen

- Chapter 8: Leases Part II: Problem 4: Multiple Choice - Computational 1. D 2. BDokument7 SeitenChapter 8: Leases Part II: Problem 4: Multiple Choice - Computational 1. D 2. Bmarriette joy abadNoch keine Bewertungen

- Tutorial 9 PIT1 Summer 2023 Sample AnswerDokument6 SeitenTutorial 9 PIT1 Summer 2023 Sample Answernewgen2173Noch keine Bewertungen

- Finman Chapter 7Dokument6 SeitenFinman Chapter 7Maria Kathreena Andrea AdevaNoch keine Bewertungen

- Chapter 8 Time Value of Money - SolutionDokument7 SeitenChapter 8 Time Value of Money - SolutionanjaliNoch keine Bewertungen

- Chapter 17 Intacc Post Employment BenefitDokument16 SeitenChapter 17 Intacc Post Employment BenefitKyle MariéNoch keine Bewertungen

- Problem Set 6 (Group 2) Evaluating A Single Project: Guerrero, Leigh Francis - Gc21Dokument5 SeitenProblem Set 6 (Group 2) Evaluating A Single Project: Guerrero, Leigh Francis - Gc21Alexander P Belka0% (1)

- 93 - Final Preaboard AFAR SolutionsDokument11 Seiten93 - Final Preaboard AFAR SolutionsLeiNoch keine Bewertungen

- Impusto A La Renta 2022 P. N. V Cat.Dokument18 SeitenImpusto A La Renta 2022 P. N. V Cat.STEFANIA ANGGIE ALVAREZ SILESNoch keine Bewertungen

- 02 FAR02-answersDokument18 Seiten02 FAR02-answersBea GarciaNoch keine Bewertungen

- Exercises Module 8 For UploadDokument16 SeitenExercises Module 8 For UploadjpNoch keine Bewertungen

- Solution of Tutorial 6Dokument4 SeitenSolution of Tutorial 6Richard MidgleyNoch keine Bewertungen

- Simple Interest: I PV X I X NDokument4 SeitenSimple Interest: I PV X I X NLorrianne RosanaNoch keine Bewertungen

- Accounting and Financial ManagementDokument7 SeitenAccounting and Financial ManagementMelokuhle MhlongoNoch keine Bewertungen

- Liability recognition and journal entries for warranty contractsDokument33 SeitenLiability recognition and journal entries for warranty contractsBella De LiañoNoch keine Bewertungen

- Fin420.540 Jan 2018 Q2-5Dokument8 SeitenFin420.540 Jan 2018 Q2-5Amar AzuanNoch keine Bewertungen

- Techniques of Capital Budgeting SumsDokument15 SeitenTechniques of Capital Budgeting Sumshardika jadavNoch keine Bewertungen

- Activity 1 Engineering Economy: I PRTDokument5 SeitenActivity 1 Engineering Economy: I PRTtaliya cocoNoch keine Bewertungen

- Financial AspectDokument13 SeitenFinancial AspectGElla BarRete ReQuilloNoch keine Bewertungen

- Individuals Assign3Dokument7 SeitenIndividuals Assign3jdNoch keine Bewertungen

- TUTORIAL BKAT2013 (288748)Dokument3 SeitenTUTORIAL BKAT2013 (288748)Hafizzudin ZolkifelyNoch keine Bewertungen

- Question OneDokument16 SeitenQuestion OneShesha Nimna GamageNoch keine Bewertungen

- Ace Oct8 BFDokument4 SeitenAce Oct8 BFAce ClarkNoch keine Bewertungen

- BFF2341 Tri A 2020 Mini Test 2 SolutionDokument3 SeitenBFF2341 Tri A 2020 Mini Test 2 SolutionDuankai LinNoch keine Bewertungen

- Finman Case 1Dokument9 SeitenFinman Case 1Jastine Sosa100% (1)

- XYZ Company flexible budget and variance analysisDokument15 SeitenXYZ Company flexible budget and variance analysisTanvir OnifNoch keine Bewertungen

- 01 Hire Purchase PQ SolDokument14 Seiten01 Hire Purchase PQ Solshubhamsingh143deepNoch keine Bewertungen

- Accounting for revenue from franchise agreementsDokument18 SeitenAccounting for revenue from franchise agreementsNicoleNoch keine Bewertungen

- NOTES AND INVENTORIES KEY CONCEPTSDokument10 SeitenNOTES AND INVENTORIES KEY CONCEPTSAlizah Lariosa BucotNoch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- WEEK 13 Financial ControlDokument13 SeitenWEEK 13 Financial ControlChuah Chong AnnNoch keine Bewertungen

- Merger and Acquisition StrategiesDokument34 SeitenMerger and Acquisition StrategiesHananie NanieNoch keine Bewertungen

- Week 9 - BenchmarkingDokument1 SeiteWeek 9 - BenchmarkingChuah Chong AnnNoch keine Bewertungen

- Management Accounting: Information That Creates ValueDokument101 SeitenManagement Accounting: Information That Creates ValueChuah Chong Ann100% (1)

- Lecture Exercise - Chapter 4Dokument2 SeitenLecture Exercise - Chapter 4Chuah Chong AnnNoch keine Bewertungen

- M Frs 8 ChecklistDokument33 SeitenM Frs 8 ChecklistChuah Chong AnnNoch keine Bewertungen

- Topic 4 (Responding To Primary Stakeholders) : Stockholder Rights and Corporate GovernanceDokument27 SeitenTopic 4 (Responding To Primary Stakeholders) : Stockholder Rights and Corporate GovernanceChuah Chong AnnNoch keine Bewertungen

- Lesson 2: Relevant Costs For Decision MakingDokument41 SeitenLesson 2: Relevant Costs For Decision MakingChuah Chong AnnNoch keine Bewertungen

- Barriers to Implementing Performance Measurement SystemsDokument1 SeiteBarriers to Implementing Performance Measurement SystemsChuah Chong AnnNoch keine Bewertungen

- Part I: Government Election: April 2017Dokument4 SeitenPart I: Government Election: April 2017Chuah Chong AnnNoch keine Bewertungen

- WEO DataDokument20 SeitenWEO DataChuah Chong AnnNoch keine Bewertungen

- Corporate Finance DataDokument24 SeitenCorporate Finance DataChuah Chong Ann100% (1)

- Lecture 11 - Audit in Public SectorDokument56 SeitenLecture 11 - Audit in Public SectorChuah Chong Ann100% (2)

- Macro Environment Analysis Combined v2Dokument9 SeitenMacro Environment Analysis Combined v2Chuah Chong AnnNoch keine Bewertungen

- UK Corporate Finance Tutorial Investment AppraisalDokument9 SeitenUK Corporate Finance Tutorial Investment AppraisalChuah Chong AnnNoch keine Bewertungen

- Tutorial 7 Q1 and Q2 ConsolidationDokument12 SeitenTutorial 7 Q1 and Q2 ConsolidationChuah Chong AnnNoch keine Bewertungen

- Lecture 6 - Performance Management in Public SectorDokument4 SeitenLecture 6 - Performance Management in Public SectorChuah Chong AnnNoch keine Bewertungen

- Assigment Checklist Jan2019 - Updated 1Dokument33 SeitenAssigment Checklist Jan2019 - Updated 1Chuah Chong AnnNoch keine Bewertungen

- MUET July 2013 WritingDokument19 SeitenMUET July 2013 WritingChuah Chong Ann67% (3)

- PFP Group Assignment - 17032019Dokument38 SeitenPFP Group Assignment - 17032019Chuah Chong AnnNoch keine Bewertungen

- Acc101 RevCh1 3 PDFDokument29 SeitenAcc101 RevCh1 3 PDFWaqar AliNoch keine Bewertungen

- Solutions To End-of-Chapter Three ProblemsDokument13 SeitenSolutions To End-of-Chapter Three ProblemsAn HoàiNoch keine Bewertungen

- International Taxation of Hybrid EntitiesDokument11 SeitenInternational Taxation of Hybrid EntitiesNilormi MukherjeeNoch keine Bewertungen

- Preqin Latin America Report 2021Dokument35 SeitenPreqin Latin America Report 2021Carlos ArangoNoch keine Bewertungen

- Dwnload Full Essentials of Corporate Finance 7th Edition Ross Test Bank PDFDokument35 SeitenDwnload Full Essentials of Corporate Finance 7th Edition Ross Test Bank PDFoutlying.pedantry.85yc100% (12)

- EF2A1 HDT Budget Upto Direct Taxes PCB4 1629376359978Dokument30 SeitenEF2A1 HDT Budget Upto Direct Taxes PCB4 1629376359978Mamta Patel100% (1)

- Solution 1Dokument5 SeitenSolution 1frq qqrNoch keine Bewertungen

- MACROECONOMICS MADE SIMPLEDokument19 SeitenMACROECONOMICS MADE SIMPLEnorleen.sarmientoNoch keine Bewertungen

- EAE0516 - 2022 - Slides 15Dokument25 SeitenEAE0516 - 2022 - Slides 15Nicholas WhittakerNoch keine Bewertungen

- CREATE Bill Impact on Philippine Company TaxesDokument8 SeitenCREATE Bill Impact on Philippine Company TaxesHanee Ruth BlueNoch keine Bewertungen

- IFC Promotes Private Sector Growth in Developing NationsDokument7 SeitenIFC Promotes Private Sector Growth in Developing NationsJawad Ali RaiNoch keine Bewertungen

- Portfolio Selection and Management Using Power BIDokument37 SeitenPortfolio Selection and Management Using Power BIKomal SharmaNoch keine Bewertungen

- Cost Sheet FormatDokument5 SeitenCost Sheet Formatvicky3230Noch keine Bewertungen

- Mobile Money International Sdn Bhd Company ProfileDokument1 SeiteMobile Money International Sdn Bhd Company ProfileLee Chee SoonNoch keine Bewertungen

- C11 Principles and Practice of InsuranceDokument9 SeitenC11 Principles and Practice of InsuranceAnonymous y3E7ia100% (2)

- Power of Attorney (General)Dokument3 SeitenPower of Attorney (General)champakNoch keine Bewertungen

- KYC checklist for filling formDokument35 SeitenKYC checklist for filling formAjay Kumar MattupalliNoch keine Bewertungen

- Cmfas M 9: OduleDokument23 SeitenCmfas M 9: Odulezihan.pohNoch keine Bewertungen

- Daily Current Affairs: 20 January 2024Dokument17 SeitenDaily Current Affairs: 20 January 2024YASH PANDEYNoch keine Bewertungen

- Investment Management Analysis: Your Company NameDokument70 SeitenInvestment Management Analysis: Your Company NameJojoMagnoNoch keine Bewertungen

- Capital Structure and Firm Efficiency: Dimitris Margaritis and Maria PsillakiDokument23 SeitenCapital Structure and Firm Efficiency: Dimitris Margaritis and Maria PsillakiRafael G. MaciasNoch keine Bewertungen

- ProblemsDokument28 SeitenProblemsKevin NguyenNoch keine Bewertungen

- Quiz Test 2 KMB FM 05Dokument1 SeiteQuiz Test 2 KMB FM 05Vivek Singh RanaNoch keine Bewertungen

- Mitsui OSK Lines Vs Orient Ship AgencyDokument108 SeitenMitsui OSK Lines Vs Orient Ship Agencyvallury chaitanya RaoNoch keine Bewertungen

- Implementing Your Business PlanDokument10 SeitenImplementing Your Business PlanGian Carlo Devera71% (7)

- Paper 5-Financial Accounting: Answer To MTP - Intermediate - Syllabus 2012 - Dec2015 - Set 2Dokument22 SeitenPaper 5-Financial Accounting: Answer To MTP - Intermediate - Syllabus 2012 - Dec2015 - Set 2AK Aru ShettyNoch keine Bewertungen

- Flame I - Jaideep FinalDokument23 SeitenFlame I - Jaideep FinalShreya TalujaNoch keine Bewertungen

- Accounting For Cash and Cash TransactionDokument63 SeitenAccounting For Cash and Cash TransactionAura Angela SeradaNoch keine Bewertungen

- Residual Valuations & Development AppraisalsDokument16 SeitenResidual Valuations & Development Appraisalscky20252838100% (1)

- 01 Basilan Estate V CIRDokument2 Seiten01 Basilan Estate V CIRBasil MaguigadNoch keine Bewertungen