Das könnte Ihnen auch gefallen

- Asian Development Outlook 2015: Financing Asia’s Future GrowthVon EverandAsian Development Outlook 2015: Financing Asia’s Future GrowthNoch keine Bewertungen

- Economic Highlights - Business Conditions and Consumer Sentiment - 16/7/2010Dokument2 SeitenEconomic Highlights - Business Conditions and Consumer Sentiment - 16/7/2010Rhb InvestNoch keine Bewertungen

- Rising US Government Debt: What To Watch? Treasury Auctions, Rating Agencies, and The Term PremiumDokument51 SeitenRising US Government Debt: What To Watch? Treasury Auctions, Rating Agencies, and The Term PremiumZerohedge100% (1)

- Document 1083870621Dokument5 SeitenDocument 1083870621Okan AladağNoch keine Bewertungen

- Economic Highlights - Leading Index Rebounded in March, Pointing To A Resilient Economic Growth in 2H 2010 - 17/5/2010Dokument2 SeitenEconomic Highlights - Leading Index Rebounded in March, Pointing To A Resilient Economic Growth in 2H 2010 - 17/5/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Leading Index Slowed Down in May, Pointing To A More Moderate Economic Growth in 2H 2010 - 19/7/2010Dokument2 SeitenEconomic Highlights - Leading Index Slowed Down in May, Pointing To A More Moderate Economic Growth in 2H 2010 - 19/7/2010Rhb InvestNoch keine Bewertungen

- Chris Fraser, Sirius Minerals - Argus Europe Fertilizer 2017Dokument28 SeitenChris Fraser, Sirius Minerals - Argus Europe Fertilizer 2017vzgscribdNoch keine Bewertungen

- Economic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Dokument2 SeitenEconomic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Rose To US$100.7bn As at 30 September - 08/10/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Rose To US$100.7bn As at 30 September - 08/10/2010Rhb InvestNoch keine Bewertungen

- Bwa M 03272018Dokument8 SeitenBwa M 03272018asdf100% (1)

- Economic Highlights :leading Index Slowed Down in April, Pointing To A More Moderate Economic Growth in 2H 2010-21/06/2010Dokument2 SeitenEconomic Highlights :leading Index Slowed Down in April, Pointing To A More Moderate Economic Growth in 2H 2010-21/06/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights: Foreign Exchange Reserves Inched Up To US$95.3bn at End-August-07/09/2010Dokument2 SeitenEconomic Highlights: Foreign Exchange Reserves Inched Up To US$95.3bn at End-August-07/09/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Inched Up Marginally To US$95.0bn As at 30 July - 09/08/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Inched Up Marginally To US$95.0bn As at 30 July - 09/08/2010Rhb InvestNoch keine Bewertungen

- SVAR PaperDokument15 SeitenSVAR PaperImtiaz HussainNoch keine Bewertungen

- Economic Highlights :foreign Exchange Reserves Fell To US$94.8bn As at 30 June - 07/07/2010Dokument2 SeitenEconomic Highlights :foreign Exchange Reserves Fell To US$94.8bn As at 30 June - 07/07/2010Rhb InvestNoch keine Bewertungen

- Cash Budget FIN242 PYQDokument7 SeitenCash Budget FIN242 PYQNurafiqah Muddin100% (1)

- COVID-19 Pandemic: Financial Stability Implications and Policy Measures TakenDokument14 SeitenCOVID-19 Pandemic: Financial Stability Implications and Policy Measures Takendesta yolandaNoch keine Bewertungen

- Economic Highlights: Leading Index Eased in February, Pointing To A More Moderate Economic Growth in 2H 2010 - 23/04/2010Dokument2 SeitenEconomic Highlights: Leading Index Eased in February, Pointing To A More Moderate Economic Growth in 2H 2010 - 23/04/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Inched Up To US$96.0bn - 10/5/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Inched Up To US$96.0bn - 10/5/2010Rhb InvestNoch keine Bewertungen

- QuestionsDokument2 SeitenQuestionsApoorv SharmaNoch keine Bewertungen

- Economic Highlights: Foreign Exchange Reserves Rose To US$95.7bn As at 15 April - 23/04/2010Dokument2 SeitenEconomic Highlights: Foreign Exchange Reserves Rose To US$95.7bn As at 15 April - 23/04/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights: Leading Index Eased in January, Points To A More Moderate Economic Growth in 2H 2010 - 22/03/2010Dokument2 SeitenEconomic Highlights: Leading Index Eased in January, Points To A More Moderate Economic Growth in 2H 2010 - 22/03/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Remained Relatively - 23/07/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Remained Relatively - 23/07/2010Rhb InvestNoch keine Bewertungen

- Client: Taiwan Semiconductor Manufacturing Co., Ltd. (NYSE: TSM / TSE: 2330) Auditor: Deloitte (1) Understanding of The ClientDokument8 SeitenClient: Taiwan Semiconductor Manufacturing Co., Ltd. (NYSE: TSM / TSE: 2330) Auditor: Deloitte (1) Understanding of The ClientDuong Trinh MinhNoch keine Bewertungen

- Maturity Profile of Schemes (Cash Flow Projections) Basis Portfolio Holdings As On May 15, 2020Dokument2 SeitenMaturity Profile of Schemes (Cash Flow Projections) Basis Portfolio Holdings As On May 15, 2020venkivlrNoch keine Bewertungen

- 2 Charts Show How Much The World Depends On Taiwan For: Revenue RecognitionDokument5 Seiten2 Charts Show How Much The World Depends On Taiwan For: Revenue RecognitionDuong Trinh MinhNoch keine Bewertungen

- RT Half Year Results 2020 SlidesDokument52 SeitenRT Half Year Results 2020 SlidesВасилий ВеликийNoch keine Bewertungen

- BIS Bulletin: Effects of Covid-19 On The Banking Sector: The Market's AssessmentDokument9 SeitenBIS Bulletin: Effects of Covid-19 On The Banking Sector: The Market's Assessmentsoumedy curpenNoch keine Bewertungen

- RT BoA Conference 2022 SlidesDokument8 SeitenRT BoA Conference 2022 SlidesJacob Jack YoshaNoch keine Bewertungen

- Suominen Nordea 10012023Dokument4 SeitenSuominen Nordea 10012023Wilhelm StjernvallNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Rose To US$96.1bn As at - 23/6/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Rose To US$96.1bn As at - 23/6/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights: Foreign Exchange Reserves Fell Marginally To US$96.9bn As at 25 February - 05/03/2010Dokument2 SeitenEconomic Highlights: Foreign Exchange Reserves Fell Marginally To US$96.9bn As at 25 February - 05/03/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights: Foreign Exchange Reserves Inched Up To US$96.1bn As at 14 May - 21/05/2010Dokument2 SeitenEconomic Highlights: Foreign Exchange Reserves Inched Up To US$96.1bn As at 14 May - 21/05/2010Rhb InvestNoch keine Bewertungen

- FX Daily: Enjoy The Lifestyle While It LastsDokument7 SeitenFX Daily: Enjoy The Lifestyle While It LastscaxapNoch keine Bewertungen

- HDFC Bank Research Presentation April 2020Dokument41 SeitenHDFC Bank Research Presentation April 2020MohitNoch keine Bewertungen

- Security Analysis & Portfolio Management: Mirae Asset Emerging Blue Chip Fund - (Regular Growth)Dokument12 SeitenSecurity Analysis & Portfolio Management: Mirae Asset Emerging Blue Chip Fund - (Regular Growth)Deepanshu VermaNoch keine Bewertungen

- Prudential BSN Takaful Berhad Investment-Linked Plan IllustrationDokument19 SeitenPrudential BSN Takaful Berhad Investment-Linked Plan IllustrationhilmiyaidinNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Fell To US$95.5bn As at 31 May - 8/6/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Fell To US$95.5bn As at 31 May - 8/6/2010Rhb InvestNoch keine Bewertungen

- (Kotak) Economy, May 08, 2020Dokument8 Seiten(Kotak) Economy, May 08, 2020abhinavsingh4uNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Rose To US$95.9bn As - 22/09/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Rose To US$95.9bn As - 22/09/2010Rhb InvestNoch keine Bewertungen

- FMR - Aug 2010Dokument10 SeitenFMR - Aug 2010Salman ArshadNoch keine Bewertungen

- FM II Case Study For ValuationsDokument2 SeitenFM II Case Study For Valuationssiddhant kohliNoch keine Bewertungen

- Ku 2023 09 PM Geschaeftsklima enDokument4 SeitenKu 2023 09 PM Geschaeftsklima enRafael BorgesNoch keine Bewertungen

- Corporate Presentation Performance Report Q4 2020Dokument37 SeitenCorporate Presentation Performance Report Q4 2020FIQIH FATHUR ROCHIMNoch keine Bewertungen

- Time To Notice Corporate Pension Plans?: Indexed Values From 8.50 Composite Corporate Funded Status of 78%Dokument4 SeitenTime To Notice Corporate Pension Plans?: Indexed Values From 8.50 Composite Corporate Funded Status of 78%Ang Wei ZouNoch keine Bewertungen

- The Lost Decade of JapanDokument31 SeitenThe Lost Decade of Japanrandy052380Noch keine Bewertungen

- State Bank of India: Play On Economic Recovery Buy MaintainedDokument4 SeitenState Bank of India: Play On Economic Recovery Buy MaintainedPaul GeorgeNoch keine Bewertungen

- Income Tax 2008-09Dokument10 SeitenIncome Tax 2008-09mohan9813032985@yahoo.com100% (16)

- PIATAFDokument1 SeitePIATAFEileen LauNoch keine Bewertungen

- Fund Manager Report18Dokument22 SeitenFund Manager Report18atharishratNoch keine Bewertungen

- Spiva Us Mid Year 2021Dokument36 SeitenSpiva Us Mid Year 2021Gábor ZsédelyNoch keine Bewertungen

- Tata Motors Limited: Capital Structure AnalysisDokument11 SeitenTata Motors Limited: Capital Structure AnalysisAjinkya YadavNoch keine Bewertungen

- Corporate CFRA ASSIGNMENTDokument11 SeitenCorporate CFRA ASSIGNMENTHimanshu NagvaniNoch keine Bewertungen

- SodapdfDokument13 SeitenSodapdfvithacitra engineeringNoch keine Bewertungen

- A10 Ipsas - 01Dokument60 SeitenA10 Ipsas - 01Marius SteffyNoch keine Bewertungen

- Chap 3Dokument19 SeitenChap 3Nagina MemonNoch keine Bewertungen

- BV Cia 3Dokument27 SeitenBV Cia 3Jobin JohnNoch keine Bewertungen

- Presentation - 1st Half 2010 ResultsDokument10 SeitenPresentation - 1st Half 2010 ResultsPiaggiogroupNoch keine Bewertungen

- ACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVDokument6 SeitenACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVmy VinayNoch keine Bewertungen

- Financial PlanDokument16 SeitenFinancial PlanSenpai Kun0% (1)

- Incred Financial Services Limited Press+ReleaseDokument7 SeitenIncred Financial Services Limited Press+ReleaseGautam MehtaNoch keine Bewertungen

- Compliance RBI Circulars Jan'22-Jun'22Dokument46 SeitenCompliance RBI Circulars Jan'22-Jun'22Gautam MehtaNoch keine Bewertungen

- Satellite Aarambh Automated - BrochureDokument4 SeitenSatellite Aarambh Automated - BrochureGautam MehtaNoch keine Bewertungen

- Vision September 2022 FinalDokument8 SeitenVision September 2022 FinalGautam MehtaNoch keine Bewertungen

- Trade RepositoryDokument57 SeitenTrade RepositoryGautam MehtaNoch keine Bewertungen

- Lenders+Deck+Mar'23 IFSDokument18 SeitenLenders+Deck+Mar'23 IFSGautam MehtaNoch keine Bewertungen

- Position Description: Primary Functions and Essential ResponsibilitiesDokument2 SeitenPosition Description: Primary Functions and Essential ResponsibilitiesGautam MehtaNoch keine Bewertungen

- FINAL MFI Directory 19 11 14 PDFDokument304 SeitenFINAL MFI Directory 19 11 14 PDFMohitNoch keine Bewertungen

- 2point2 Capital - Investor Update Q2 FY21 PDFDokument6 Seiten2point2 Capital - Investor Update Q2 FY21 PDFshahavNoch keine Bewertungen

- Stock Reco 10122019 CCDokument5 SeitenStock Reco 10122019 CCGautam MehtaNoch keine Bewertungen

- CRISIL Ratings India Top 50 MfisDokument68 SeitenCRISIL Ratings India Top 50 MfisDavid Raju GollapudiNoch keine Bewertungen

- 2point2 Capital - Investor Update Q2 FY21 PDFDokument6 Seiten2point2 Capital - Investor Update Q2 FY21 PDFshahavNoch keine Bewertungen

- Checklist of DocsDokument2 SeitenChecklist of DocsGautam MehtaNoch keine Bewertungen

- December 2019Dokument30 SeitenDecember 2019Gautam MehtaNoch keine Bewertungen

- Time Value of Money: CFA Level 1 2006 - Formula SheetDokument18 SeitenTime Value of Money: CFA Level 1 2006 - Formula SheetGautam MehtaNoch keine Bewertungen

- 21 Tools PrintoutDokument23 Seiten21 Tools PrintoutGautam MehtaNoch keine Bewertungen

- RBI's Monetary Policy: Vivriti ViewDokument1 SeiteRBI's Monetary Policy: Vivriti ViewGautam MehtaNoch keine Bewertungen

- Letter Appointment MR - Aditya SapruDokument5 SeitenLetter Appointment MR - Aditya SapruGautam MehtaNoch keine Bewertungen

- Corporate Performance Q3 FY19Dokument12 SeitenCorporate Performance Q3 FY19Gautam MehtaNoch keine Bewertungen

- JRL Money - GuideDokument16 SeitenJRL Money - GuideGautam MehtaNoch keine Bewertungen

- A Highway To Debt: "He Who Promises Runs in Debt." - The TalmudDokument6 SeitenA Highway To Debt: "He Who Promises Runs in Debt." - The TalmudGautam MehtaNoch keine Bewertungen

- FaltuDokument1 SeiteFaltuGautam MehtaNoch keine Bewertungen

- 1 B Ed RevisedSyllabusDokument97 Seiten1 B Ed RevisedSyllabusdharmranoliaNoch keine Bewertungen

- PE VC Funding An OverviewDokument20 SeitenPE VC Funding An OverviewGautam MehtaNoch keine Bewertungen

- Dave Landry Discretionary RulesDokument8 SeitenDave Landry Discretionary RulesJack Jensen0% (1)

- Marketing MCQs 1Dokument29 SeitenMarketing MCQs 1Manish SoniNoch keine Bewertungen

- Free Cash Flow TheoryDokument57 SeitenFree Cash Flow Theoryprashantgupta84Noch keine Bewertungen

- Tweeter Etc CaseDokument3 SeitenTweeter Etc CaseSupratik DattaNoch keine Bewertungen

- Customer LoyaltyDokument16 SeitenCustomer LoyaltySiddharth TrivediNoch keine Bewertungen

- FINAL Examination: Basic Finance: Money, Banking and CreditDokument5 SeitenFINAL Examination: Basic Finance: Money, Banking and CreditHoward UntalanNoch keine Bewertungen

- CM3-CU11 Financial ManagementDokument6 SeitenCM3-CU11 Financial ManagementKEZIA GERONIMONoch keine Bewertungen

- Difference Between Vertical and Horizontal MarketDokument3 SeitenDifference Between Vertical and Horizontal Marketkristoffer_dawisNoch keine Bewertungen

- ENT 430 International Business IIDokument329 SeitenENT 430 International Business IIEmeka Ken NwosuNoch keine Bewertungen

- Week Five:: Reporting andDokument38 SeitenWeek Five:: Reporting andIzham ShabdeanNoch keine Bewertungen

- ACCT 323 - Stockholder's Equity Project - 100 Points Due April 27 at Midnight ESTDokument2 SeitenACCT 323 - Stockholder's Equity Project - 100 Points Due April 27 at Midnight ESTAhmed AdamjeeNoch keine Bewertungen

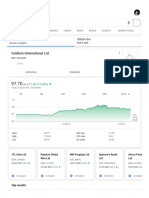

- Goldiam Share - Google SearchDokument5 SeitenGoldiam Share - Google SearchDudheshwar SinghNoch keine Bewertungen

- Mercury QuestionsDokument6 SeitenMercury Questionsapi-239586293Noch keine Bewertungen

- Parle and BritanniaLDokument35 SeitenParle and BritanniaLDristiNoch keine Bewertungen

- Half Yearly Portfolio Statement For Period Ended 31 Mar 2021Dokument398 SeitenHalf Yearly Portfolio Statement For Period Ended 31 Mar 2021Chaitra KamalakarNoch keine Bewertungen

- Chapter 3 - : Product Design & Process SelectionDokument36 SeitenChapter 3 - : Product Design & Process SelectionTejal1212Noch keine Bewertungen

- Infosys Consulting in 2006Dokument8 SeitenInfosys Consulting in 2006parvathyjoy90Noch keine Bewertungen

- Coverage HSBCDokument21 SeitenCoverage HSBCBill LeeNoch keine Bewertungen

- Chapter 5-Agricultural PricesDokument37 SeitenChapter 5-Agricultural PricesMina GuillerminaNoch keine Bewertungen

- Stock Market Project VaibhavDokument71 SeitenStock Market Project VaibhavVaibhav DhayeNoch keine Bewertungen

- Chapter3 4Dokument24 SeitenChapter3 4kakolalamamaNoch keine Bewertungen

- Advertising and Sales ManagementDokument123 SeitenAdvertising and Sales ManagementNidhisha P MNoch keine Bewertungen

- Investing: When and How To Start?Dokument2 SeitenInvesting: When and How To Start?Avni GuptaNoch keine Bewertungen

- Sparkline Venture CapitalDokument17 SeitenSparkline Venture CapitallycancapitalNoch keine Bewertungen

- Essentials of Investments 11th Edition Bodie Test BankDokument47 SeitenEssentials of Investments 11th Edition Bodie Test Banksportfulscenefulzb3nh100% (33)

- Marketing Plan TemplateDokument5 SeitenMarketing Plan TemplateMuhammad ShanNoch keine Bewertungen

- Managerial Economics An Analysis of Business IssuesDokument25 SeitenManagerial Economics An Analysis of Business Issueslinda zyongweNoch keine Bewertungen

- Petrobras of Brazil and The CostDokument3 SeitenPetrobras of Brazil and The CostIoana PunctNoch keine Bewertungen

- Malinowski in Oaxaca: Implications of An Unfinished Project in Economic Anthropology, Part IDokument28 SeitenMalinowski in Oaxaca: Implications of An Unfinished Project in Economic Anthropology, Part IAgustinaPutriNoch keine Bewertungen

- Module 1 DBA Econ HonorsDokument3 SeitenModule 1 DBA Econ HonorsREESE ABRAHAMOFFNoch keine Bewertungen