Das könnte Ihnen auch gefallen

- Supply Chain Management and Business Performance: The VASC ModelVon EverandSupply Chain Management and Business Performance: The VASC ModelNoch keine Bewertungen

- Lillo Imperial Lecture3Dokument90 SeitenLillo Imperial Lecture3BrettCoburnNoch keine Bewertungen

- Order Flow Analysis of Cryptocurrency Markets - Ed Silantyev - MediumDokument12 SeitenOrder Flow Analysis of Cryptocurrency Markets - Ed Silantyev - MediumJames LiuNoch keine Bewertungen

- LSE Warrant RulesDokument11 SeitenLSE Warrant RulesDawei ZhangNoch keine Bewertungen

- 02 Micronotes 070907Dokument21 Seiten02 Micronotes 070907Arash MojahedNoch keine Bewertungen

- International Evidence On Algorithmic TradingDokument46 SeitenInternational Evidence On Algorithmic TradingmattNoch keine Bewertungen

- 212 (FINAL) 財務金融學刊Dokument42 Seiten212 (FINAL) 財務金融學刊Wei TeNoch keine Bewertungen

- Volume 29, Issue 3: Profitability of The On-Balance Volume IndicatorDokument8 SeitenVolume 29, Issue 3: Profitability of The On-Balance Volume IndicatorRavikumar GandlaNoch keine Bewertungen

- Abergel - HF LEad LagDokument40 SeitenAbergel - HF LEad LagsmysonaNoch keine Bewertungen

- The Forecasting Power of The Volatility Index in Emerging Markets: Evidence From The Taiwan Stock MarketDokument15 SeitenThe Forecasting Power of The Volatility Index in Emerging Markets: Evidence From The Taiwan Stock MarketasrshsNoch keine Bewertungen

- 10.4324 9781003095354-2 ChapterpdfDokument20 Seiten10.4324 9781003095354-2 Chapterpdfnguyenlena.cs2Noch keine Bewertungen

- J.P.Morgan: JanuaryDokument33 SeitenJ.P.Morgan: JanuaryMarketsWikiNoch keine Bewertungen

- Trade Duration and Market ImpactDokument10 SeitenTrade Duration and Market Impactluminous blueNoch keine Bewertungen

- Jurnal 8Dokument11 SeitenJurnal 8nellymhdr25Noch keine Bewertungen

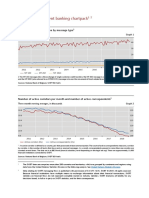

- CPMI Correspondent Banking Chartpack: Monthly Transaction Volume by Message TypeDokument33 SeitenCPMI Correspondent Banking Chartpack: Monthly Transaction Volume by Message TypeHenry Omar Espinal VasquezNoch keine Bewertungen

- Determinants of The Trading FragmentationDokument13 SeitenDeterminants of The Trading FragmentationThe IjbmtNoch keine Bewertungen

- Retracements With TMV: Trade Breakouts andDokument7 SeitenRetracements With TMV: Trade Breakouts andDevang Varma100% (1)

- Price Discovery in NSE Spot and Futures Markets of India: Evidence From Selected IT IndustriesDokument12 SeitenPrice Discovery in NSE Spot and Futures Markets of India: Evidence From Selected IT Industriesvasantham_praneethNoch keine Bewertungen

- DD-SS FrameworkDokument24 SeitenDD-SS FrameworkFausto Da GamaNoch keine Bewertungen

- The Nature of Price2Dokument17 SeitenThe Nature of Price2Khalil Antoine DayriNoch keine Bewertungen

- Abergel LecturesDokument105 SeitenAbergel LecturesBolbo NaNoch keine Bewertungen

- Time Series AnalysisDokument35 SeitenTime Series AnalysisAditya JunejaNoch keine Bewertungen

- High Frequency Automated TradingDokument4 SeitenHigh Frequency Automated TradingSumente YoNoch keine Bewertungen

- Research ProposalDokument18 SeitenResearch ProposalArjun KohliNoch keine Bewertungen

- Transaction 1Dokument29 SeitenTransaction 1fkkfoxNoch keine Bewertungen

- Proposal 155Dokument7 SeitenProposal 155Udaya KumarNoch keine Bewertungen

- 75 Fed. Reg. 75208 (Dec. 2, 2010) (The "SEC Proposal") - 75 Fed. Reg. 76140 (Dec. 7, 2010) (The "CFTC Proposal" And, Together With The SEC Proposal, The "Proposed Rules")Dokument23 Seiten75 Fed. Reg. 75208 (Dec. 2, 2010) (The "SEC Proposal") - 75 Fed. Reg. 76140 (Dec. 7, 2010) (The "CFTC Proposal" And, Together With The SEC Proposal, The "Proposed Rules")MarketsWikiNoch keine Bewertungen

- JPM Flows Liquidity 2016-10-07 2145906Dokument18 SeitenJPM Flows Liquidity 2016-10-07 2145906chaotic_pandemoniumNoch keine Bewertungen

- Cespa TickSizeSurveyv2Dokument36 SeitenCespa TickSizeSurveyv2bnjangale13Noch keine Bewertungen

- Trend Thrust IndicatorDokument6 SeitenTrend Thrust IndicatorNo NameNoch keine Bewertungen

- How To Enhance Market Liquidity by Nicholas Economides EC-94-03 January 1994Dokument13 SeitenHow To Enhance Market Liquidity by Nicholas Economides EC-94-03 January 1994Fjäll RävenNoch keine Bewertungen

- 2-2: Volksmaschine: Kevin: 32 Sumegh: 28 Atul: 04 Sanjay: 17 Gayatri: 25Dokument19 Seiten2-2: Volksmaschine: Kevin: 32 Sumegh: 28 Atul: 04 Sanjay: 17 Gayatri: 25Sanjay GhodadraNoch keine Bewertungen

- Could A Trader Using Only "Old" Technical Indicator Be Successful at The Forex Market?Dokument8 SeitenCould A Trader Using Only "Old" Technical Indicator Be Successful at The Forex Market?HaichuNoch keine Bewertungen

- CHAPTER II-Applied EconomicsDokument8 SeitenCHAPTER II-Applied EconomicsAllyn BalabatNoch keine Bewertungen

- High Frequency Trading: Price Dynamics Models and Market Making StrategiesDokument40 SeitenHigh Frequency Trading: Price Dynamics Models and Market Making StrategiesSeyyed Mohammad Hossein SherafatNoch keine Bewertungen

- Anomalous Price Impact and The Critical Nature of Liquidity in Financial MarketsDokument16 SeitenAnomalous Price Impact and The Critical Nature of Liquidity in Financial MarketsnalyatNoch keine Bewertungen

- Why Does Ipo Volume Fluctuate So MuchDokument38 SeitenWhy Does Ipo Volume Fluctuate So MuchéricNoch keine Bewertungen

- Shan PHD F2014Dokument120 SeitenShan PHD F2014Irina AlexandraNoch keine Bewertungen

- Term PaperDokument21 SeitenTerm PaperNoush NazmiNoch keine Bewertungen

- 1 s2.0 S1386418121000173 MainDokument22 Seiten1 s2.0 S1386418121000173 MainAshwin KurupNoch keine Bewertungen

- Volume Spikes & Index Reversals - The Technical Analyst, May 2004Dokument4 SeitenVolume Spikes & Index Reversals - The Technical Analyst, May 2004Steffen L. Norgren100% (1)

- Tungsong Et Al-2011-SSRN Electronic JournalDokument37 SeitenTungsong Et Al-2011-SSRN Electronic JournalLucas WeeNoch keine Bewertungen

- Active Trader Magazine - The TUT SpreadDokument4 SeitenActive Trader Magazine - The TUT Spreadgneyman100% (1)

- Cross-Correlations in Warsaw Stock Exchange: A B A, B BDokument9 SeitenCross-Correlations in Warsaw Stock Exchange: A B A, B BMorglodos MorglodosNoch keine Bewertungen

- Day Trading With Canlestick and Moving Averages - Stephen BigalowDokument3 SeitenDay Trading With Canlestick and Moving Averages - Stephen Bigalowarashiro100% (2)

- ITG TCA - Koscom Seminar March 2013Dokument32 SeitenITG TCA - Koscom Seminar March 2013smallakeNoch keine Bewertungen

- 10 1108 - Jcefts 11 2016 0031Dokument19 Seiten10 1108 - Jcefts 11 2016 0031SITI MADHIHAH OTHMANNoch keine Bewertungen

- OTC MarketsDokument7 SeitenOTC MarketsMiguel NetoNoch keine Bewertungen

- Judgement Day Algorithmic Trading Around The Swiss Franc Cap RemovalDokument30 SeitenJudgement Day Algorithmic Trading Around The Swiss Franc Cap RemovalTorVikNoch keine Bewertungen

- The Value of A Millisecond - Full StudyDokument46 SeitenThe Value of A Millisecond - Full StudytabbforumNoch keine Bewertungen

- Financial Markets and Institutions Course Outline - SINDHUDokument4 SeitenFinancial Markets and Institutions Course Outline - SINDHUNajia SiddiquiNoch keine Bewertungen

- Edge Ratio of Nifty For Last 15 Years On Donchian ChannelDokument8 SeitenEdge Ratio of Nifty For Last 15 Years On Donchian ChannelthesijNoch keine Bewertungen

- Competition in Nyse-Listed Stocks: Do Investors Benefit From Highly Competitive Markets?Dokument33 SeitenCompetition in Nyse-Listed Stocks: Do Investors Benefit From Highly Competitive Markets?Alexandru ZipișiNoch keine Bewertungen

- Market Impact of Small Orders: Oleh Danyliv Usoft Hti Inc 9 January 2022Dokument10 SeitenMarket Impact of Small Orders: Oleh Danyliv Usoft Hti Inc 9 January 2022icosahedron_manNoch keine Bewertungen

- W 24648Dokument54 SeitenW 24648ghalibNoch keine Bewertungen

- PPD1041 Sem1 2023 LU5 AssignmentDokument9 SeitenPPD1041 Sem1 2023 LU5 Assignmentchunkit033Noch keine Bewertungen

- The Journal of Finance - 2022 - CHERNOV - Pricing Currency RisksDokument38 SeitenThe Journal of Finance - 2022 - CHERNOV - Pricing Currency RisksAshraf KhanNoch keine Bewertungen

- Uncovering The Trend Following StrategyDokument10 SeitenUncovering The Trend Following StrategyRikers11Noch keine Bewertungen

- Yieldbook LMM Term ModelDokument20 SeitenYieldbook LMM Term Modelphilline2009100% (1)

- John Denver Take Me Home Country Roads REUPLOADDokument16 SeitenJohn Denver Take Me Home Country Roads REUPLOADJeffrey Yan75% (4)

- An Introduction To Intertask Transfer For Reinforcement LearningDokument20 SeitenAn Introduction To Intertask Transfer For Reinforcement LearningJeffrey YanNoch keine Bewertungen

- 1 OverviewDokument18 Seiten1 OverviewJeffrey YanNoch keine Bewertungen

- Poetry: Jeffrey Yan 7th PeriodDokument1 SeitePoetry: Jeffrey Yan 7th PeriodJeffrey YanNoch keine Bewertungen

- Forecasting With Dummy Variables: Group 6 Evin Whittington Travis MennDokument9 SeitenForecasting With Dummy Variables: Group 6 Evin Whittington Travis MennMila Grace Lavilla PacienteNoch keine Bewertungen

- 3.2.2 Predicting Satisfaction From Avoidance, Anxiety, Commitment and ConflictDokument3 Seiten3.2.2 Predicting Satisfaction From Avoidance, Anxiety, Commitment and ConflictKaren PinterNoch keine Bewertungen

- Paper 1Dokument34 SeitenPaper 1Juana Montes GaddaNoch keine Bewertungen

- Turan 2015 HF MethodsDokument8 SeitenTuran 2015 HF Methodsirem emine demirNoch keine Bewertungen

- A Comparison Between Semi-Theoretical and Empirical Modeling of Cross-FlowDokument12 SeitenA Comparison Between Semi-Theoretical and Empirical Modeling of Cross-Flowmadadi moradNoch keine Bewertungen

- Salma Fathiya Ma'arifa ) Iwan Budiyono )Dokument15 SeitenSalma Fathiya Ma'arifa ) Iwan Budiyono )indahNoch keine Bewertungen

- Ekonomika Vol 10 No 2 Juni 2023 Hal 94-104Dokument11 SeitenEkonomika Vol 10 No 2 Juni 2023 Hal 94-104piraaaja12Noch keine Bewertungen

- Kristen Marrinan-American Beauty StandardsDokument32 SeitenKristen Marrinan-American Beauty StandardsMaria RomeroNoch keine Bewertungen

- A. Persamaan RegresiDokument10 SeitenA. Persamaan RegresiCindy Nur OktavianiNoch keine Bewertungen

- PGP Dsba BrochureDokument12 SeitenPGP Dsba BrochureSam Sep A SixtyoneNoch keine Bewertungen

- Monitoring and Alarming Wear MetalsDokument8 SeitenMonitoring and Alarming Wear MetalsJeefNoch keine Bewertungen

- Study On Competency MappingDokument56 SeitenStudy On Competency Mappingdkdineshece100% (1)

- Class Exercises Topic 2 Solutions: Jordi Blanes I Vidal Econometrics: Theory and ApplicationsDokument12 SeitenClass Exercises Topic 2 Solutions: Jordi Blanes I Vidal Econometrics: Theory and ApplicationsCartieNoch keine Bewertungen

- The Appraisal of The Real Estate 14th Edition-401-600Dokument200 SeitenThe Appraisal of The Real Estate 14th Edition-401-600AIDIL SAPUTRANoch keine Bewertungen

- State and Trait GratitudeDokument10 SeitenState and Trait GratitudeDiana MarianaNoch keine Bewertungen

- Impact of Microfinance On Women's Empowerment: A Case Study On Two Microfinance Institutions in Sri LankaDokument11 SeitenImpact of Microfinance On Women's Empowerment: A Case Study On Two Microfinance Institutions in Sri Lankamandala jyoshnaNoch keine Bewertungen

- Final Term Paper 3Dokument21 SeitenFinal Term Paper 3Stanley NgacheNoch keine Bewertungen

- Activities Midterm PC1 - PROF1 Financial Management PDFDokument5 SeitenActivities Midterm PC1 - PROF1 Financial Management PDFMarienell YuNoch keine Bewertungen

- Factors Influencing The Bank Profitability - Empirical Evidence From AlbaniaDokument13 SeitenFactors Influencing The Bank Profitability - Empirical Evidence From AlbaniaaiNoch keine Bewertungen

- The Step Construction of Penalized Spline in Electrical Power Load DataDokument10 SeitenThe Step Construction of Penalized Spline in Electrical Power Load DataAnya NieveNoch keine Bewertungen

- Studi Kasus: Identifikasi Komponen Penciri Akreditasi Sekolah/Madrasah Pada Tingkat SD/MI Di Provinsi Kalimantan Timur Tahun 2015Dokument8 SeitenStudi Kasus: Identifikasi Komponen Penciri Akreditasi Sekolah/Madrasah Pada Tingkat SD/MI Di Provinsi Kalimantan Timur Tahun 2015Tika MijayantiNoch keine Bewertungen

- Grammar Mastery and Vocabulary On The Students' English Speaing Skill MasrupiDokument16 SeitenGrammar Mastery and Vocabulary On The Students' English Speaing Skill MasrupiVido TriantamaNoch keine Bewertungen

- Dividen 1Dokument3 SeitenDividen 1Lucyana Maria MagdalenaNoch keine Bewertungen

- Estadística Clase 7Dokument24 SeitenEstadística Clase 7Andres GaortNoch keine Bewertungen

- Educational Attainment and Drug UseDokument30 SeitenEducational Attainment and Drug UseKayla WysockiNoch keine Bewertungen

- Statistics For Data Science - Le - James D. MillerDokument456 SeitenStatistics For Data Science - Le - James D. MillerWilliam Rojas100% (9)

- Stock ReturnDokument7 SeitenStock ReturnHans Surya Candra DiwiryaNoch keine Bewertungen

- Saravanan BaskaranDokument7 SeitenSaravanan BaskaranSuhanthi ManiNoch keine Bewertungen

- Predicting Probability of Debt Default A Study of Corporate Debt Market in India and Other CountriesDokument321 SeitenPredicting Probability of Debt Default A Study of Corporate Debt Market in India and Other CountriesPrerna RanjanNoch keine Bewertungen

- Intelligence and Educational AchievementDokument10 SeitenIntelligence and Educational AchievementucanNoch keine Bewertungen