Das könnte Ihnen auch gefallen

- Here are the journal entries for Complex Company for 2015 and 2016:JOURNAL ENTRIESDokument20 SeitenHere are the journal entries for Complex Company for 2015 and 2016:JOURNAL ENTRIESJudith Gabutero100% (2)

- 1k PaypalDokument110 Seiten1k PaypalMariana FuentesNoch keine Bewertungen

- Case Assignment 8 - Diamond Energy Resources PDFDokument3 SeitenCase Assignment 8 - Diamond Energy Resources PDFAudrey Ang100% (1)

- Twenty4: How To Ace Four of The Toughest Job Interview QuestionsDokument2 SeitenTwenty4: How To Ace Four of The Toughest Job Interview QuestionsAlliant Credit UnionNoch keine Bewertungen

- Request LetterDokument2 SeitenRequest LetterprahladjoshiNoch keine Bewertungen

- Fast-Track Tax Reform: Lessons from the MaldivesVon EverandFast-Track Tax Reform: Lessons from the MaldivesNoch keine Bewertungen

- Impairment of Loans and Receivable FinancingDokument17 SeitenImpairment of Loans and Receivable FinancingGelyn CruzNoch keine Bewertungen

- Cio FMCGDokument608 SeitenCio FMCGshreya lakshminarayananNoch keine Bewertungen

- Is It Worth It UAE Qatar Expenses Vs PackageDokument29 SeitenIs It Worth It UAE Qatar Expenses Vs Packageandruta1978Noch keine Bewertungen

- OpTransactionHistoryUX324 01 2020 PDFDokument4 SeitenOpTransactionHistoryUX324 01 2020 PDFHimavanth ReddyNoch keine Bewertungen

- IMFPA CHINA MT IRENE - ALFRED..doc - 0.odtDokument7 SeitenIMFPA CHINA MT IRENE - ALFRED..doc - 0.odtAnonymous HQhmctG100% (2)

- FSCM PPTDokument34 SeitenFSCM PPTManohar G Shankar100% (1)

- BPIDokument36 SeitenBPIApril BoreresNoch keine Bewertungen

- Sales Case Digest - DoublesalesDokument12 SeitenSales Case Digest - DoublesalesMichael JoffNoch keine Bewertungen

- Class Work & Home Work Question of Final Account of Banking Conpany 22-23Dokument23 SeitenClass Work & Home Work Question of Final Account of Banking Conpany 22-23DARK KING GamersNoch keine Bewertungen

- 19 - Ch4 Weekly QuestionsDokument10 Seiten19 - Ch4 Weekly QuestionsCamilo ToroNoch keine Bewertungen

- A) Date Description Debit $ Credit $Dokument5 SeitenA) Date Description Debit $ Credit $simranNoch keine Bewertungen

- BHM307 Financial Management ExamDokument4 SeitenBHM307 Financial Management ExamAmit Mondal0% (1)

- 12 Redemption of DebenturesDokument13 Seiten12 Redemption of DebenturesRohith KumarNoch keine Bewertungen

- IAS 23 Borrowing Costs (ICAP C6 A10) : Based On Number of Months)Dokument2 SeitenIAS 23 Borrowing Costs (ICAP C6 A10) : Based On Number of Months)Ashura ShaibNoch keine Bewertungen

- Basic Principle of AccountingDokument3 SeitenBasic Principle of Accounting22ba045Noch keine Bewertungen

- Government Grant ActivitiesDokument5 SeitenGovernment Grant Activitiesjoong wanNoch keine Bewertungen

- BUMDES Financial Records 2018Dokument7 SeitenBUMDES Financial Records 2018Batosai RasidinNoch keine Bewertungen

- Aidcom Financial Accounting AnalysisDokument17 SeitenAidcom Financial Accounting AnalysisAjmal K HussainNoch keine Bewertungen

- ACW1120-Practice Questions: Page 1 of 5Dokument5 SeitenACW1120-Practice Questions: Page 1 of 5Gan ZhengweiNoch keine Bewertungen

- Master of Business Administration Semester - I Subject Code& Name - Mba104 & Financial and Management Accounting AssignmentDokument8 SeitenMaster of Business Administration Semester - I Subject Code& Name - Mba104 & Financial and Management Accounting AssignmentÑýì Ñýì ÑâìñgNoch keine Bewertungen

- Final Paper 2Dokument258 SeitenFinal Paper 2chandresh0% (1)

- FSSP Q22 Progress Report Dec 2015-Loan (Reviewed 16feb 2016)Dokument9 SeitenFSSP Q22 Progress Report Dec 2015-Loan (Reviewed 16feb 2016)Wikileaks2024Noch keine Bewertungen

- School Update Feb09 - TOWNHALLDokument18 SeitenSchool Update Feb09 - TOWNHALLanthony.restar1251Noch keine Bewertungen

- Commerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Dokument12 SeitenCommerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Ashok dore Ashok doreNoch keine Bewertungen

- AFA End Examination 2021-2022Dokument6 SeitenAFA End Examination 2021-2022sebastian mlingwaNoch keine Bewertungen

- Tutorial 8 - AnswersDokument6 SeitenTutorial 8 - AnswersBoby Kristanto ChandraNoch keine Bewertungen

- Depreciation ExplainedDokument9 SeitenDepreciation ExplainedPriyank JainNoch keine Bewertungen

- Cash Flow Statement XYZ LtdDokument2 SeitenCash Flow Statement XYZ LtdSuvam PatelNoch keine Bewertungen

- Report On Financial Structure of Maruti Suzuki India LimitedDokument6 SeitenReport On Financial Structure of Maruti Suzuki India LimitedSabab ZamanNoch keine Bewertungen

- Lecture 4 Islamic Banking Operations - DepositDokument44 SeitenLecture 4 Islamic Banking Operations - DepositborhansetiNoch keine Bewertungen

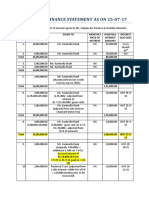

- Kalpana Financial Statement - Updated As On 25-07-17Dokument5 SeitenKalpana Financial Statement - Updated As On 25-07-17Nelapudi SureshNoch keine Bewertungen

- FinAct ARDokument12 SeitenFinAct ARNMCartNoch keine Bewertungen

- Question 3: Ias 23 Borrowing CostsDokument2 SeitenQuestion 3: Ias 23 Borrowing CostsAbdul Sami100% (3)

- Accounting for Receivables in BCSVDokument6 SeitenAccounting for Receivables in BCSVJerric CristobalNoch keine Bewertungen

- Apply for Sanchay Public Deposit SchemeDokument6 SeitenApply for Sanchay Public Deposit SchemeDwiref VoraNoch keine Bewertungen

- 3rd Week Cash Flow AnalysisDokument19 Seiten3rd Week Cash Flow AnalysisCj TolentinoNoch keine Bewertungen

- Calculation of Rebate: Particular Dr. CRDokument12 SeitenCalculation of Rebate: Particular Dr. CRDennis BijuNoch keine Bewertungen

- 07 Loan Receivable MCPDokument4 Seiten07 Loan Receivable MCPkyle mandaresioNoch keine Bewertungen

- Banking Company Final Accounts: Profit, Loss, Assets, LiabilitiesDokument20 SeitenBanking Company Final Accounts: Profit, Loss, Assets, LiabilitiesPaulomi LahaNoch keine Bewertungen

- Tugas Akm 3Dokument1 SeiteTugas Akm 3cindyegaa27Noch keine Bewertungen

- Small Business Enterprise Loan: Ermel O. TagardaDokument18 SeitenSmall Business Enterprise Loan: Ermel O. Tagardaboa1315Noch keine Bewertungen

- Final Exam Sample1Dokument21 SeitenFinal Exam Sample1JiaFengNoch keine Bewertungen

- 1 Investment Options To Retirement MoneyDokument3 Seiten1 Investment Options To Retirement MoneyAMIT SHARMANoch keine Bewertungen

- Topic 3 Lease TutorialDokument9 SeitenTopic 3 Lease TutorialHakim AzmiNoch keine Bewertungen

- Cyntia Amelia Siregar-4b-Lat-9-Pt. Palas Star PlantationDokument8 SeitenCyntia Amelia Siregar-4b-Lat-9-Pt. Palas Star PlantationAmel GpNoch keine Bewertungen

- Ts Grewal Solutions Class 12 Accountancy Volume 2 Chapter 9Dokument6 SeitenTs Grewal Solutions Class 12 Accountancy Volume 2 Chapter 9samuraisurya58Noch keine Bewertungen

- Number Maximum Mark Student Mark 1 17 2 11 3 18 4 10 5 12 6 10 7 12Dokument5 SeitenNumber Maximum Mark Student Mark 1 17 2 11 3 18 4 10 5 12 6 10 7 12pinkyNoch keine Bewertungen

- Sanchay Public Deposit FormDokument6 SeitenSanchay Public Deposit Formmanoj barokaNoch keine Bewertungen

- Alliance - NOD (Amended 1.0)Dokument3 SeitenAlliance - NOD (Amended 1.0)Daniel OthmanNoch keine Bewertungen

- Acf 312Dokument6 SeitenAcf 312Selu Semahle NdlondloNoch keine Bewertungen

- Indonesian Bank Cash and Current AccountsDokument30 SeitenIndonesian Bank Cash and Current AccountsTata Intan Tamara100% (1)

- BSBFIA412 AssessmentDokument10 SeitenBSBFIA412 AssessmentXavar Xan100% (4)

- FR Suggested Dec 2021Dokument36 SeitenFR Suggested Dec 2021Rahul NandurkarNoch keine Bewertungen

- CA Foundation Accounts A MTP 2 Dec 2022Dokument11 SeitenCA Foundation Accounts A MTP 2 Dec 2022shagana212005Noch keine Bewertungen

- JETJET Co Investment ScheduleDokument2 SeitenJETJET Co Investment Schedulehy googleNoch keine Bewertungen

- Calculating Capitalized InterestDokument12 SeitenCalculating Capitalized InterestRamin AminNoch keine Bewertungen

- ConsultaDokument17 SeitenConsultaDQNIELNoch keine Bewertungen

- BANK3011 Week 13 Tutorial QuestionsDokument2 SeitenBANK3011 Week 13 Tutorial QuestionsJamie ChanNoch keine Bewertungen

- 2019 Financial Plan and Proposed Budget UpdateDokument22 Seiten2019 Financial Plan and Proposed Budget UpdateDan RyanNoch keine Bewertungen

- Loan Details Charges: Customer Portal ExperiaDokument4 SeitenLoan Details Charges: Customer Portal ExperiaAlpesh KuleNoch keine Bewertungen

- RTP Dec 2020 QnsDokument13 SeitenRTP Dec 2020 QnsbinuNoch keine Bewertungen

- Chartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalDokument81 SeitenChartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalPrashant Sagar GautamNoch keine Bewertungen

- Kalpana Financial Statement - Updated As On 25-10-18Dokument8 SeitenKalpana Financial Statement - Updated As On 25-10-18Nelapudi SureshNoch keine Bewertungen

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNoch keine Bewertungen

- January CatalogDokument2 SeitenJanuary CatalogterencebctanNoch keine Bewertungen

- Key Timeshare ConceptsDokument35 SeitenKey Timeshare ConceptsterencebctanNoch keine Bewertungen

- Ooi Say Peng - 2021 - SGHC 128Dokument14 SeitenOoi Say Peng - 2021 - SGHC 128terencebctanNoch keine Bewertungen

- [2024] SGHCF 18Dokument9 Seiten[2024] SGHCF 18terencebctanNoch keine Bewertungen

- U.S. Naval Test Pilot School Flight Test Manual: Rotary Wing PerformanceDokument562 SeitenU.S. Naval Test Pilot School Flight Test Manual: Rotary Wing PerformanceterencebctanNoch keine Bewertungen

- Non Resi Handbook PDFDokument180 SeitenNon Resi Handbook PDFterencebctanNoch keine Bewertungen

- Im Skaugen CaseDokument71 SeitenIm Skaugen CaseterencebctanNoch keine Bewertungen

- Solar Power en Data PDFDokument16 SeitenSolar Power en Data PDFterencebctanNoch keine Bewertungen

- ABSD Rates Fact SheetDokument3 SeitenABSD Rates Fact SheetterencebctanNoch keine Bewertungen

- (2020) Sgipos 4Dokument48 Seiten(2020) Sgipos 4terencebctanNoch keine Bewertungen

- Singapore Court of Appeal Case Summary on Undue Influence, UnconscionabilityDokument12 SeitenSingapore Court of Appeal Case Summary on Undue Influence, UnconscionabilityterencebctanNoch keine Bewertungen

- Real Estate Salesperson (Res) Examination Syllabus 2017Dokument30 SeitenReal Estate Salesperson (Res) Examination Syllabus 2017terencebctanNoch keine Bewertungen

- Swatch V Apple (2019) SGIPOS 1 PDFDokument49 SeitenSwatch V Apple (2019) SGIPOS 1 PDFterencebctanNoch keine Bewertungen

- ISCA Insolvency Update 2017Dokument8 SeitenISCA Insolvency Update 2017terencebctanNoch keine Bewertungen

- EJD QuestionairreDokument10 SeitenEJD QuestionairreterencebctanNoch keine Bewertungen

- (2018) SGHC 254 MCST 940 V Lim Florence MajorieDokument27 Seiten(2018) SGHC 254 MCST 940 V Lim Florence MajorieterencebctanNoch keine Bewertungen

- SoS FF8 Hidden Movement Sheet 150 PDFDokument1 SeiteSoS FF8 Hidden Movement Sheet 150 PDFterencebctanNoch keine Bewertungen

- (2019) SGHC 72 PP V Ewe Pang Kooi - CBTDokument42 Seiten(2019) SGHC 72 PP V Ewe Pang Kooi - CBTterencebctan100% (2)

- ARW v Comptroller of Income Tax and another appealDokument26 SeitenARW v Comptroller of Income Tax and another appealterencebctanNoch keine Bewertungen

- ERA Option To PurchaseDokument3 SeitenERA Option To Purchaseterencebctan100% (1)

- (2018) SGHC 259 Re Im SkaugenDokument29 Seiten(2018) SGHC 259 Re Im SkaugenterencebctanNoch keine Bewertungen

- (2010) 11 SAL Ann Rev 476 (Land Law)Dokument18 Seiten(2010) 11 SAL Ann Rev 476 (Land Law)terencebctanNoch keine Bewertungen

- SoS FF4 Hidden Movement Sheet 150Dokument1 SeiteSoS FF4 Hidden Movement Sheet 150terencebctanNoch keine Bewertungen

- State Courts Singapore updates practice directionsDokument11 SeitenState Courts Singapore updates practice directionsterencebctanNoch keine Bewertungen

- Torres - Rule SummaryDokument1 SeiteTorres - Rule SummaryterencebctanNoch keine Bewertungen

- Istanbul Dice Game RulesDokument8 SeitenIstanbul Dice Game RulesterencebctanNoch keine Bewertungen

- Stone Age RulesDokument8 SeitenStone Age RulesterencebctanNoch keine Bewertungen

- SoS FF5 Hidden Movement Sheet 150 PDFDokument1 SeiteSoS FF5 Hidden Movement Sheet 150 PDFterencebctanNoch keine Bewertungen

- Coh Planning Map Atb BWDokument3 SeitenCoh Planning Map Atb BWterencebctanNoch keine Bewertungen

- Functions of RBIDokument8 SeitenFunctions of RBIdchauhan21Noch keine Bewertungen

- Exam DiscussionDokument4 SeitenExam DiscussionChelliah SelvavishnuNoch keine Bewertungen

- Chapter 3. Banker Customer RelationshipDokument38 SeitenChapter 3. Banker Customer RelationshippadminiNoch keine Bewertungen

- Chp8 3edition PDFDokument21 SeitenChp8 3edition PDFAbarajithan RajendranNoch keine Bewertungen

- Analysis of E-Broking Marketing StrategiesDokument45 SeitenAnalysis of E-Broking Marketing StrategiesAbhishekKaushikNoch keine Bewertungen

- Quantitative ToolsDokument14 SeitenQuantitative Tools9439223514pNoch keine Bewertungen

- ch03 Part6Dokument6 Seitench03 Part6Sergio HoffmanNoch keine Bewertungen

- Application For A Vehicle Registration Certificate: For More Information Go ToDokument2 SeitenApplication For A Vehicle Registration Certificate: For More Information Go TogdddNoch keine Bewertungen

- Mr. Wan Mohd Nazri Wan Osman, Central Bank of MalaysiaDokument6 SeitenMr. Wan Mohd Nazri Wan Osman, Central Bank of Malaysiabrendan lanzaNoch keine Bewertungen

- CH 08Dokument52 SeitenCH 08kareem_batista20860% (5)

- Political Factors:: Pestel Analysis of The Wives of Migrant Workers Who Reside in KeralaDokument4 SeitenPolitical Factors:: Pestel Analysis of The Wives of Migrant Workers Who Reside in KeralaShaina DewanNoch keine Bewertungen

- Max Healthcare Institute Limited BSE 539981 Financials Balance SheetDokument3 SeitenMax Healthcare Institute Limited BSE 539981 Financials Balance Sheetakumar4uNoch keine Bewertungen

- Forming Corps & RecognitionDokument3 SeitenForming Corps & RecognitionDiane JulianNoch keine Bewertungen

- Base 24Dokument254 SeitenBase 24sjayaraman79Noch keine Bewertungen

- TAX - IPCC Amendment For Nov, 2013 Attempt (Carocks - Wordpress.com)Dokument84 SeitenTAX - IPCC Amendment For Nov, 2013 Attempt (Carocks - Wordpress.com)Dushyant SinghaniaNoch keine Bewertungen

- Compliance Officers (Brokers) Module Curriculum 1.Dokument2 SeitenCompliance Officers (Brokers) Module Curriculum 1.ambreenkhanamNoch keine Bewertungen

- Internship-Report-on-General-Banking-of-Janata-Bank-Limited 2Dokument35 SeitenInternship-Report-on-General-Banking-of-Janata-Bank-Limited 2Bronson CastroNoch keine Bewertungen

- ALM Policy SummaryDokument9 SeitenALM Policy Summarytreddy249Noch keine Bewertungen

- H Theory of Money SupplyDokument3 SeitenH Theory of Money SupplyShofi R Krishna100% (17)

- Correction of Accounting Errors GuideDokument2 SeitenCorrection of Accounting Errors GuideJean Emanuel100% (1)

![[2024] SGHCF 18](https://imgv2-2-f.scribdassets.com/img/document/725134737/149x198/0111f688a2/1713689118?v=1)