Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Chapter 05 Sample QsDokument3 SeitenChapter 05 Sample QsSourovNoch keine Bewertungen

- CH 03 Sample QsDokument6 SeitenCH 03 Sample QsSourovNoch keine Bewertungen

- Appendix-B (Answers To End-Of-Chapter Problems)Dokument7 SeitenAppendix-B (Answers To End-Of-Chapter Problems)SourovNoch keine Bewertungen

- C - 8: T A C M: Hapter HE Nalysis of Ompetitive ArketsDokument18 SeitenC - 8: T A C M: Hapter HE Nalysis of Ompetitive ArketsSourovNoch keine Bewertungen

- Journal of Business Research: Wei Zheng, Baiyin Yang, Gary N. McleanDokument9 SeitenJournal of Business Research: Wei Zheng, Baiyin Yang, Gary N. McleanSourovNoch keine Bewertungen

- August: Monday Wednesday Thursday Friday Saturday Sunday MondayDokument12 SeitenAugust: Monday Wednesday Thursday Friday Saturday Sunday MondaySourovNoch keine Bewertungen

- US AppealDokument1 SeiteUS AppealSourovNoch keine Bewertungen

- Sample Data Table: Transaction Type Date Category AmountDokument11 SeitenSample Data Table: Transaction Type Date Category AmountSourovNoch keine Bewertungen

- August: Monday Wednesday Thursday Friday Saturday Sunday MondayDokument12 SeitenAugust: Monday Wednesday Thursday Friday Saturday Sunday MondaySourovNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Joint ArrangementsDokument3 SeitenJoint ArrangementsCha EsguerraNoch keine Bewertungen

- Insurance LectureDokument4 SeitenInsurance LectureDenardConwiBesaNoch keine Bewertungen

- Midterm Exam On AUDIT PROBLEMS PPE AND INVESTMENTSDokument28 SeitenMidterm Exam On AUDIT PROBLEMS PPE AND INVESTMENTSReginald ValenciaNoch keine Bewertungen

- Account Transactions: Winnie VillanuevaDokument14 SeitenAccount Transactions: Winnie VillanuevaPaula Bautista100% (7)

- Premium Prize BondDokument2 SeitenPremium Prize BondTariq Mehmood6530% (1)

- BergerDokument39 SeitenBergerABHAY KUMAR SINGHNoch keine Bewertungen

- Chapter 2 - Advanced AccDokument15 SeitenChapter 2 - Advanced AccAsad KhadarNoch keine Bewertungen

- DRHP AimlDokument636 SeitenDRHP AimlSubscriptionNoch keine Bewertungen

- Amaia Land Corp. Amaia Steps Alabang Sample Computation OnlyDokument1 SeiteAmaia Land Corp. Amaia Steps Alabang Sample Computation OnlyDarNumNoch keine Bewertungen

- Loan Pricing 916Dokument22 SeitenLoan Pricing 916Gonçalo MadalenoNoch keine Bewertungen

- Cambridge Assessment International Education: Accounting 9706/21 October/November 2018Dokument11 SeitenCambridge Assessment International Education: Accounting 9706/21 October/November 2018Takudzwa GudoNoch keine Bewertungen

- CIMB Islamic Sukuk Fund: Fund Objective Investment VolatilityDokument2 SeitenCIMB Islamic Sukuk Fund: Fund Objective Investment VolatilityMaria haneffNoch keine Bewertungen

- Institute and Faculty of Actuaries: Subject SA3 - General Insurance Specialist AdvancedDokument5 SeitenInstitute and Faculty of Actuaries: Subject SA3 - General Insurance Specialist AdvancedbaidshryansNoch keine Bewertungen

- Schedule IagoDokument8 SeitenSchedule IagoIago MartinsNoch keine Bewertungen

- Level III of CFA Program Mock Exam 1 - Solutions (PM)Dokument46 SeitenLevel III of CFA Program Mock Exam 1 - Solutions (PM)Lê Chấn PhongNoch keine Bewertungen

- Corporate Finance 3rd Edition by Berk DeMarzo ISBN Test BankDokument38 SeitenCorporate Finance 3rd Edition by Berk DeMarzo ISBN Test Bankcarl100% (24)

- P3 Pertemuan 3Dokument8 SeitenP3 Pertemuan 3Ahsan FirdausNoch keine Bewertungen

- Quiz 03. Operating Segments, NCA Held For SaleDokument4 SeitenQuiz 03. Operating Segments, NCA Held For SaleEstilo100% (1)

- Syndicate Assignment: Case Study: Letting Go of Lehman BrothersDokument6 SeitenSyndicate Assignment: Case Study: Letting Go of Lehman BrothersJane Tito100% (1)

- Job Costing AssignmentDokument6 SeitenJob Costing AssignmentKwason TaylorNoch keine Bewertungen

- Mutual Funds in India A Comparative Study of Select Public Sector and Private Sector CompaniesDokument13 SeitenMutual Funds in India A Comparative Study of Select Public Sector and Private Sector Companiesarcherselevators0% (1)

- London Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelDokument16 SeitenLondon Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelFarbeen Satira MirzaNoch keine Bewertungen

- Internship-Report On An Appraisal of The Activities of Al-Arafah Islami Bank LTDDokument52 SeitenInternship-Report On An Appraisal of The Activities of Al-Arafah Islami Bank LTDSamia TazinNoch keine Bewertungen

- Financial Report and ControlDokument22 SeitenFinancial Report and ControlRonggo SaputroNoch keine Bewertungen

- Chapter 16 Advacc2Dokument60 SeitenChapter 16 Advacc2AnneShannenBambaDabuNoch keine Bewertungen

- ACFAR 3134 Intermediate Accounting 3 Third Year: First SemesterDokument38 SeitenACFAR 3134 Intermediate Accounting 3 Third Year: First SemesterchxrlttxNoch keine Bewertungen

- Worsksheet #1Dokument4 SeitenWorsksheet #1Sharmin ReulaNoch keine Bewertungen

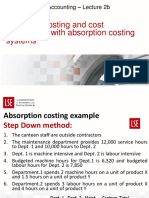

- Job-Order Costing and Cost Assignment With Absorption Costing SystemsDokument50 SeitenJob-Order Costing and Cost Assignment With Absorption Costing SystemsAnh Quan NguyenNoch keine Bewertungen

- Sector PE 28.12.2023Dokument19 SeitenSector PE 28.12.2023zawadulhkNoch keine Bewertungen

- Saving Secure Account V6Dokument20 SeitenSaving Secure Account V6Jei ChanNoch keine Bewertungen