Das könnte Ihnen auch gefallen

- Sneaker 2013Dokument6 SeitenSneaker 2013Shivam Bose67% (3)

- Sneakers 2013Dokument5 SeitenSneakers 2013priyaa0364% (11)

- Npv Analysis Of New Product LaunchDokument8 SeitenNpv Analysis Of New Product LaunchFelicity YuanNoch keine Bewertungen

- Universiti Utara Malaysia Bwff2043 Advanced Financial Management (Group A) SECOND SEMESTER SESSION 2019/2020 (A192)Dokument10 SeitenUniversiti Utara Malaysia Bwff2043 Advanced Financial Management (Group A) SECOND SEMESTER SESSION 2019/2020 (A192)Hirosha VejianNoch keine Bewertungen

- Sneaker SolutionDokument19 SeitenSneaker SolutionSuperGuyNoch keine Bewertungen

- Sneaker 2013Dokument13 SeitenSneaker 2013Hirosha Vejian100% (2)

- PPTXDokument8 SeitenPPTXWriters Wing100% (2)

- Global Athletic Footwear Market AnalysisDokument7 SeitenGlobal Athletic Footwear Market AnalysisMNoch keine Bewertungen

- Sneakers 2013Dokument5 SeitenSneakers 2013Felicia FrancisNoch keine Bewertungen

- New Balance Sneakers 2013 vs Persistence Project AnalysisDokument4 SeitenNew Balance Sneakers 2013 vs Persistence Project AnalysisMehwish Pervaiz100% (2)

- Sneakers SolutionDokument7 SeitenSneakers SolutionRamesh Singh100% (1)

- Sneaker 2013 ExcelDokument8 SeitenSneaker 2013 ExcelMehwish Pervaiz67% (6)

- Robertson Tool Company Financial AnalysisDokument17 SeitenRobertson Tool Company Financial AnalysisWasp_007_007Noch keine Bewertungen

- Income Statements and Balance Sheets for Flash Memory, Inc. (2007-2009Dokument25 SeitenIncome Statements and Balance Sheets for Flash Memory, Inc. (2007-2009Theicon420Noch keine Bewertungen

- Momouth Case Study PresentationDokument18 SeitenMomouth Case Study PresentationSven Mueller100% (5)

- New Heritage Doll Company Financial AnalysisDokument31 SeitenNew Heritage Doll Company Financial AnalysisSoundarya AbiramiNoch keine Bewertungen

- Sneaker Excel Sheet For Risk AnalysisDokument11 SeitenSneaker Excel Sheet For Risk AnalysisSuperGuyNoch keine Bewertungen

- TN-1 TN-2 Financials Cost CapitalDokument9 SeitenTN-1 TN-2 Financials Cost Capitalxcmalsk100% (1)

- Flash - Memory - Inc From Website 0515Dokument8 SeitenFlash - Memory - Inc From Website 0515竹本口木子100% (1)

- NHDC Solution EditedDokument5 SeitenNHDC Solution EditedShreesh ChandraNoch keine Bewertungen

- Flash Memory CaseDokument6 SeitenFlash Memory Casechitu199233% (3)

- Hallstead Jewelers Strategy to Reverse LossesDokument10 SeitenHallstead Jewelers Strategy to Reverse LossesAshley Winters100% (1)

- Flash Memory Case Study SolutionDokument8 SeitenFlash Memory Case Study SolutionRohit Parnerkar57% (7)

- Flash MemoryDokument9 SeitenFlash MemoryJeffery KaoNoch keine Bewertungen

- New Heritage Doll CaseDokument9 SeitenNew Heritage Doll Caseapi-30934141185% (13)

- Clarkson Lumber Cash Flows and Pro FormaDokument6 SeitenClarkson Lumber Cash Flows and Pro FormaArmaan ChandnaniNoch keine Bewertungen

- Economy Shipping Co Case SolutionDokument7 SeitenEconomy Shipping Co Case SolutionPaco Colín100% (2)

- Hallstead Jewelers PDFDokument9 SeitenHallstead Jewelers PDFRaghav JainNoch keine Bewertungen

- Financial PerformanceDokument7 SeitenFinancial PerformanceJustin Ho100% (1)

- Halstead JewlersDokument8 SeitenHalstead JewlersZeeshan Ali100% (1)

- Gilbert Lumber LC ExcelDokument3 SeitenGilbert Lumber LC ExcelEvelyn De de Leon100% (3)

- Monmouth CaseDokument8 SeitenMonmouth CaseFrank Rotella100% (2)

- Flash Memory AnalysisDokument25 SeitenFlash Memory AnalysisaamirNoch keine Bewertungen

- Reparations 2Dokument2 SeitenReparations 2rahulNoch keine Bewertungen

- New Heritage Doll CompanDokument9 SeitenNew Heritage Doll CompanArima ChatterjeeNoch keine Bewertungen

- New Heritage Doll - SolutionDokument4 SeitenNew Heritage Doll - Solutionrath347775% (4)

- Case - Flash Memory, Inc. - SolutionDokument11 SeitenCase - Flash Memory, Inc. - SolutionBryan Meza71% (38)

- Case AnalysisDokument11 SeitenCase AnalysisSagar Bansal50% (2)

- Economy Shipping Case AnswersDokument72 SeitenEconomy Shipping Case Answersreduay67% (3)

- New Heritage ExhibitsDokument4 SeitenNew Heritage ExhibitsBRobbins12100% (16)

- FlashMemory Beta NPVDokument7 SeitenFlashMemory Beta NPVShubham Bhatia100% (1)

- Case Hansson Private LabelDokument15 SeitenCase Hansson Private Labelpaul57% (7)

- Monmouth Case SolutionDokument19 SeitenMonmouth Case SolutionAkshat Nayer40% (10)

- Heritage CaseDokument3 SeitenHeritage CaseGregory ChengNoch keine Bewertungen

- Analysis of Fastener Manufacturing Costs and ProfitsDokument13 SeitenAnalysis of Fastener Manufacturing Costs and ProfitsKaran Oberoi33% (6)

- Flash Memory, Inc.Dokument2 SeitenFlash Memory, Inc.Stella Zukhbaia0% (5)

- Proforma Cash Flow Analysis and Recommendations for Chemalite IncDokument8 SeitenProforma Cash Flow Analysis and Recommendations for Chemalite IncHàMềmNoch keine Bewertungen

- MonmouthDokument16 SeitenMonmouthjamn1979100% (1)

- Valuation Analysis For Robertson ToolDokument5 SeitenValuation Analysis For Robertson ToolPedro José ZapataNoch keine Bewertungen

- Monmouth CaseDokument6 SeitenMonmouth CaseMohammed Akhtab Ul HudaNoch keine Bewertungen

- New Heritage DollDokument8 SeitenNew Heritage DollJITESH GUPTANoch keine Bewertungen

- Case 5Dokument12 SeitenCase 5JIAXUAN WANGNoch keine Bewertungen

- Financing Daycare CenterDokument3 SeitenFinancing Daycare CenterAngel CastilloNoch keine Bewertungen

- Making Capital Investment DecisionsDokument48 SeitenMaking Capital Investment DecisionsJerico ClarosNoch keine Bewertungen

- Simdora Manufacturing Private LTD: Project Report OnDokument14 SeitenSimdora Manufacturing Private LTD: Project Report OnShivam DashottarNoch keine Bewertungen

- NPV and IRR Analysis of Equipment Replacement and Project SelectionDokument16 SeitenNPV and IRR Analysis of Equipment Replacement and Project SelectionsheldonNoch keine Bewertungen

- Expansion Project Example: Dr. C. Bulent AybarDokument10 SeitenExpansion Project Example: Dr. C. Bulent AybarTricia Mae PetalverNoch keine Bewertungen

- Acctg110 FinalsDokument21 SeitenAcctg110 FinalsRoman Dominic LlanoNoch keine Bewertungen

- Vertical BfsDokument4 SeitenVertical BfsKrüpãl MãñgrùlêNoch keine Bewertungen

- Analysis of Project Cash FlowsDokument16 SeitenAnalysis of Project Cash FlowsTanmaye KapurNoch keine Bewertungen

- Income Statement: End of WorksheetDokument2 SeitenIncome Statement: End of WorksheetChetan DasguptaNoch keine Bewertungen

- Undergrad Guide TorDokument68 SeitenUndergrad Guide TorAman MehtaNoch keine Bewertungen

- 5G FactsDokument6 Seiten5G FactsChetan DasguptaNoch keine Bewertungen

- Presentation MaloDokument65 SeitenPresentation Malor_somnathNoch keine Bewertungen

- How To Create Google Meetings PDFDokument3 SeitenHow To Create Google Meetings PDFChetan DasguptaNoch keine Bewertungen

- How To Join Google MeetingDokument1 SeiteHow To Join Google MeetingChetan DasguptaNoch keine Bewertungen

- 1 - Alt BykesDokument12 Seiten1 - Alt BykesChetan DasguptaNoch keine Bewertungen

- How To Create Google Meetings PDFDokument3 SeitenHow To Create Google Meetings PDFChetan DasguptaNoch keine Bewertungen

- Service CharacteristicsDokument8 SeitenService CharacteristicsMAHENDRA SHIVAJI DHENAK79% (14)

- Right To Be Forthright: NtroductionDokument2 SeitenRight To Be Forthright: NtroductionChetan DasguptaNoch keine Bewertungen

- OmnichannelDokument11 SeitenOmnichannelChetan DasguptaNoch keine Bewertungen

- How Dogs Communicate Stress and DiscomfortDokument2 SeitenHow Dogs Communicate Stress and DiscomfortChetan DasguptaNoch keine Bewertungen

- How Dogs Communicate Stress and DiscomfortDokument2 SeitenHow Dogs Communicate Stress and DiscomfortChetan DasguptaNoch keine Bewertungen

- Milford Industries CaseDokument1 SeiteMilford Industries CaseChetan DasguptaNoch keine Bewertungen

- OmnichannelDokument11 SeitenOmnichannelChetan DasguptaNoch keine Bewertungen

- Executive SumaryDokument1 SeiteExecutive SumaryChetan DasguptaNoch keine Bewertungen

- Henry Tam and The Mgi TeamDokument7 SeitenHenry Tam and The Mgi TeamPreeti MachharNoch keine Bewertungen

- Personality Type PDFDokument35 SeitenPersonality Type PDFChetan DasguptaNoch keine Bewertungen

- 1 Executive Summary: Business PlanDokument1 Seite1 Executive Summary: Business PlanChetan DasguptaNoch keine Bewertungen

- Copyright CaseDokument7 SeitenCopyright CaseChetan DasguptaNoch keine Bewertungen

- Self Determination TheoryDokument11 SeitenSelf Determination TheoryChetan Dasgupta100% (1)

- Bajaj Leadership TeamDokument5 SeitenBajaj Leadership TeamChetan DasguptaNoch keine Bewertungen

- Government Expenditures and Economic Growth: Lessons for UkraineDokument56 SeitenGovernment Expenditures and Economic Growth: Lessons for UkraineChetan DasguptaNoch keine Bewertungen

- Sections of A Business PlanDokument1 SeiteSections of A Business PlanChetan DasguptaNoch keine Bewertungen

- Emami vs Patanjali Industrial Design DisputeDokument5 SeitenEmami vs Patanjali Industrial Design DisputeChetan DasguptaNoch keine Bewertungen

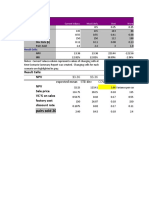

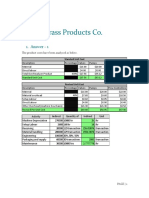

- Destin Brass Products Co.: 1. Answer - 1Dokument5 SeitenDestin Brass Products Co.: 1. Answer - 1Chetan DasguptaNoch keine Bewertungen

- Microsoft'S Financial Reporting Strategy Case Study: Individual AssignmentDokument6 SeitenMicrosoft'S Financial Reporting Strategy Case Study: Individual AssignmentchetandasguptaNoch keine Bewertungen

- Clarkson Lumbar CompanyDokument41 SeitenClarkson Lumbar CompanyTheOxyCleanGuyNoch keine Bewertungen

- Henry Tam and The Mgi TeamDokument7 SeitenHenry Tam and The Mgi TeamPreeti MachharNoch keine Bewertungen

- LTD Samplex - Serrano NotesDokument3 SeitenLTD Samplex - Serrano NotesMariam BautistaNoch keine Bewertungen

- Supply Chain AssignmentDokument29 SeitenSupply Chain AssignmentHisham JackNoch keine Bewertungen

- KT 1 Ky Nang Tong Hop 2-ThươngDokument4 SeitenKT 1 Ky Nang Tong Hop 2-ThươngLệ ThứcNoch keine Bewertungen

- Strategies To Promote ConcordanceDokument4 SeitenStrategies To Promote ConcordanceDem BertoNoch keine Bewertungen

- Amway Health CareDokument7 SeitenAmway Health CareChowduru Venkat Sasidhar SharmaNoch keine Bewertungen

- MiQ Programmatic Media Intern RoleDokument4 SeitenMiQ Programmatic Media Intern Role124 SHAIL SINGHNoch keine Bewertungen

- Skin Yale University Protein: Where Does Collagen Come From?Dokument2 SeitenSkin Yale University Protein: Where Does Collagen Come From?Ellaine Pearl AlmillaNoch keine Bewertungen

- Exámenes Trinity C1 Ejemplos - Modelo Completos de Examen PDFDokument6 SeitenExámenes Trinity C1 Ejemplos - Modelo Completos de Examen PDFM AngelesNoch keine Bewertungen

- Tanroads KilimanjaroDokument10 SeitenTanroads KilimanjaroElisha WankogereNoch keine Bewertungen

- Page 17 - Word Connection, LiaisonsDokument2 SeitenPage 17 - Word Connection, Liaisonsstarskyhutch0% (1)

- Mastering ArpeggiosDokument58 SeitenMastering Arpeggiospeterd87Noch keine Bewertungen

- Opportunity, Not Threat: Crypto AssetsDokument9 SeitenOpportunity, Not Threat: Crypto AssetsTrophy NcNoch keine Bewertungen

- Astrology - House SignificationDokument4 SeitenAstrology - House SignificationsunilkumardubeyNoch keine Bewertungen

- MVD1000 Series Catalogue PDFDokument20 SeitenMVD1000 Series Catalogue PDFEvandro PavesiNoch keine Bewertungen

- The Effects of Cabergoline Compared To Dienogest in Women With Symptomatic EndometriomaDokument6 SeitenThe Effects of Cabergoline Compared To Dienogest in Women With Symptomatic EndometriomaAnna ReznorNoch keine Bewertungen

- Advanced VLSI Architecture Design For Emerging Digital SystemsDokument78 SeitenAdvanced VLSI Architecture Design For Emerging Digital Systemsgangavinodc123Noch keine Bewertungen

- EAPP Q2 Module 2Dokument24 SeitenEAPP Q2 Module 2archiviansfilesNoch keine Bewertungen

- All Forms of Gerunds and InfinitivesDokument4 SeitenAll Forms of Gerunds and InfinitivesNagimaNoch keine Bewertungen

- Step-By-Step Guide To Essay WritingDokument14 SeitenStep-By-Step Guide To Essay WritingKelpie Alejandria De OzNoch keine Bewertungen

- Will You Be There? Song ActivitiesDokument3 SeitenWill You Be There? Song ActivitieszelindaaNoch keine Bewertungen

- Revolutionizing Via RoboticsDokument7 SeitenRevolutionizing Via RoboticsSiddhi DoshiNoch keine Bewertungen

- Sigma Chi Foundation - 2016 Annual ReportDokument35 SeitenSigma Chi Foundation - 2016 Annual ReportWes HoltsclawNoch keine Bewertungen

- What Blockchain Could Mean For MarketingDokument2 SeitenWhat Blockchain Could Mean For MarketingRitika JhaNoch keine Bewertungen

- Nazi UFOs - Another View On The MatterDokument4 SeitenNazi UFOs - Another View On The Mattermoderatemammal100% (3)

- Vegan Banana Bread Pancakes With Chocolate Chunks Recipe + VideoDokument33 SeitenVegan Banana Bread Pancakes With Chocolate Chunks Recipe + VideoGiuliana FloresNoch keine Bewertungen

- Md. Raju Ahmed RonyDokument13 SeitenMd. Raju Ahmed RonyCar UseNoch keine Bewertungen

- Developments in ESP: A Multi-Disciplinary ApproachDokument12 SeitenDevelopments in ESP: A Multi-Disciplinary ApproachDragana Lorelai JankovicNoch keine Bewertungen

- Casey at The BatDokument2 SeitenCasey at The BatGab SorianoNoch keine Bewertungen

- B2 WBLFFDokument10 SeitenB2 WBLFFflickrboneNoch keine Bewertungen

- Complicated Grief Treatment Instruction ManualDokument276 SeitenComplicated Grief Treatment Instruction ManualFrancisco Matías Ponce Miranda100% (3)