Das könnte Ihnen auch gefallen

- Formula Sheet-2nd QuizDokument6 SeitenFormula Sheet-2nd QuizEge MelihNoch keine Bewertungen

- FormulasDokument20 SeitenFormulasWilliam ZeNoch keine Bewertungen

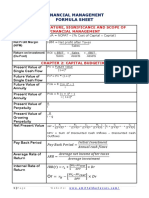

- Financial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementDokument6 SeitenFinancial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementEilen Joyce Bisnar100% (1)

- Meet 328 Module 3Dokument17 SeitenMeet 328 Module 3kimbenedictaguilar19Noch keine Bewertungen

- Công thức IM tự luận- cho finalDokument6 SeitenCông thức IM tự luận- cho finalTuấn NguyễnNoch keine Bewertungen

- Principles of Finance Formulae SheetDokument4 SeitenPrinciples of Finance Formulae SheetAmina SultangaliyevaNoch keine Bewertungen

- FM (Actuary Exam) FormulasDokument15 SeitenFM (Actuary Exam) Formulasmuffinslayers100% (1)

- FMSM FORMULA SHEET-Executive-RevisionDokument8 SeitenFMSM FORMULA SHEET-Executive-RevisionHenrick Ian AmarlesNoch keine Bewertungen

- Exam Cheat Sheet VSJDokument3 SeitenExam Cheat Sheet VSJMinh ANhNoch keine Bewertungen

- FMSM Formula SheetDokument8 SeitenFMSM Formula Sheetjacob michelNoch keine Bewertungen

- AnnuityDokument23 SeitenAnnuityCathleen Ann TorrijosNoch keine Bewertungen

- FINA 1310 - Lecture 3 NotesDokument6 SeitenFINA 1310 - Lecture 3 NotesAayushi ReddyNoch keine Bewertungen

- Lesson 2 - Interest and Money-Time RelationshipDokument8 SeitenLesson 2 - Interest and Money-Time RelationshipExcel MigsNoch keine Bewertungen

- Financial Management Equations Korea UniversityDokument2 SeitenFinancial Management Equations Korea UniversityTom DNoch keine Bewertungen

- Formulas (Weeks 1 To 6)Dokument5 SeitenFormulas (Weeks 1 To 6)Stenley RoyceNoch keine Bewertungen

- List of Corporate Finance FormulasDokument9 SeitenList of Corporate Finance FormulasYoungRedNoch keine Bewertungen

- Module 3Dokument15 SeitenModule 3Bry An CañaresNoch keine Bewertungen

- Simple Annuity DueDokument28 SeitenSimple Annuity DueNimrod CarolinoNoch keine Bewertungen

- The FRM Part I: Formula Guide: Value and Risk ModelsDokument10 SeitenThe FRM Part I: Formula Guide: Value and Risk ModelsJavneet KaurNoch keine Bewertungen

- Chap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtDokument5 SeitenChap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtTRANG NGUYỄN LÊ QUỲNHNoch keine Bewertungen

- Lesson 6 Compound InterestDokument14 SeitenLesson 6 Compound InterestDaniela CaguioaNoch keine Bewertungen

- Finance NoteDokument19 SeitenFinance NoteHui YiNoch keine Bewertungen

- Mba Finance Placement ReadyDokument18 SeitenMba Finance Placement Readyabhishek.abhishek1994Noch keine Bewertungen

- Week 2Dokument25 SeitenWeek 2ziyue wangNoch keine Bewertungen

- Lesson 2 Topic 3 UpdatedDokument6 SeitenLesson 2 Topic 3 UpdatedJAN ERWIN LACUESTANoch keine Bewertungen

- Annuity LectureDokument6 SeitenAnnuity LectureJohn Vincent V MagulianoNoch keine Bewertungen

- ACST252 - Formula SheetDokument5 SeitenACST252 - Formula Sheetyolejosh479Noch keine Bewertungen

- FM FormulasDokument24 SeitenFM FormulasMd. Nafiz ShahrierNoch keine Bewertungen

- NotesDokument5 SeitenNotesfiseco4756Noch keine Bewertungen

- Formula SheetDokument4 SeitenFormula Sheetinspiredbysims4Noch keine Bewertungen

- Finance Formula SheetDokument2 SeitenFinance Formula SheetBrandon RaoNoch keine Bewertungen

- FMSM Formula SheetDokument10 SeitenFMSM Formula SheetRani LohiaNoch keine Bewertungen

- Helpful Formulas For Finance 1Dokument2 SeitenHelpful Formulas For Finance 1Falguni ShomeNoch keine Bewertungen

- 2017 Level I Formula SheetDokument28 Seiten2017 Level I Formula SheetVishal GoriNoch keine Bewertungen

- I. How To Compute Overall Percentage Changes: Compounded M Times Per YearDokument8 SeitenI. How To Compute Overall Percentage Changes: Compounded M Times Per YearTrương Ngọc Trà MyNoch keine Bewertungen

- 2018 Level I Formula Sheet 1 PDFDokument27 Seiten2018 Level I Formula Sheet 1 PDFShamima YesminNoch keine Bewertungen

- Bus Math Grade 11 q2 m2 w1Dokument5 SeitenBus Math Grade 11 q2 m2 w1Ronald AlmagroNoch keine Bewertungen

- Chapter 3Dokument5 SeitenChapter 3Thu Trang VũNoch keine Bewertungen

- Formula Sheet For AFB by - Ambitious - BabaDokument11 SeitenFormula Sheet For AFB by - Ambitious - BabaKiran PatelNoch keine Bewertungen

- PAK CFE Supplemental Formula Sheet (Spring 2023)Dokument49 SeitenPAK CFE Supplemental Formula Sheet (Spring 2023)CalvinNoch keine Bewertungen

- Chapter 11 - Project Analysis and EvaluationDokument11 SeitenChapter 11 - Project Analysis and EvaluationNelson FernandoNoch keine Bewertungen

- Green Electric Energy: Engineering EconomicsDokument45 SeitenGreen Electric Energy: Engineering EconomicsdishantpNoch keine Bewertungen

- Mathematical Finance 1Dokument12 SeitenMathematical Finance 1Brijesh MishraNoch keine Bewertungen

- CH Gen Math 7Dokument18 SeitenCH Gen Math 7Joselito UbaldoNoch keine Bewertungen

- T3 FormulasDokument9 SeitenT3 FormulasmartinNoch keine Bewertungen

- 2022 Level I Key Facts and Formulas SheetDokument13 Seiten2022 Level I Key Facts and Formulas Sheetayesha ansari100% (2)

- 411 Chapter02 66-761520-16911405009257Dokument85 Seiten411 Chapter02 66-761520-16911405009257Ken TheeraNoch keine Bewertungen

- Engineering Economy Module 3Dokument16 SeitenEngineering Economy Module 3Stevenzel Eala Estella100% (1)

- To Find The Interest To Find The Principal To Find The Rate To Find The TimeDokument1 SeiteTo Find The Interest To Find The Principal To Find The Rate To Find The Timebonifacio gianga jrNoch keine Bewertungen

- Eco Formulas 1Dokument7 SeitenEco Formulas 1Leslie Jean ObradorNoch keine Bewertungen

- Finance Mba PlacementDokument14 SeitenFinance Mba Placementabhishek.abhishek1994Noch keine Bewertungen

- Annuities PDFDokument2 SeitenAnnuities PDFKenneth LewisNoch keine Bewertungen

- Hedging Interest Rate RiskDokument14 SeitenHedging Interest Rate RiskVictor ManuelNoch keine Bewertungen

- Formulas and ConceptsDokument7 SeitenFormulas and Conceptscolen.anneNoch keine Bewertungen

- CH 2 LuenbergerDokument10 SeitenCH 2 LuenbergerKym LatoyNoch keine Bewertungen

- Mathematics of Investment FormulasDokument4 SeitenMathematics of Investment FormulasaileeNoch keine Bewertungen

- Sample Level 1 Wiley Formula Sheets PDFDokument10 SeitenSample Level 1 Wiley Formula Sheets PDFMuhammed RafiudeenNoch keine Bewertungen

- Mathematical Formulas for Economics and Business: A Simple IntroductionVon EverandMathematical Formulas for Economics and Business: A Simple IntroductionBewertung: 4 von 5 Sternen4/5 (4)

- Corporate Finance Formulas: A Simple IntroductionVon EverandCorporate Finance Formulas: A Simple IntroductionBewertung: 4 von 5 Sternen4/5 (8)

- A-level Maths Revision: Cheeky Revision ShortcutsVon EverandA-level Maths Revision: Cheeky Revision ShortcutsBewertung: 3.5 von 5 Sternen3.5/5 (8)

- Bloomberg Businessweek USA August 7-13 2017Dokument69 SeitenBloomberg Businessweek USA August 7-13 2017Anh ThànhNoch keine Bewertungen

- Bloomberg Businessweek Middle East 31 January 2018Dokument68 SeitenBloomberg Businessweek Middle East 31 January 2018Anh ThànhNoch keine Bewertungen

- Bloomberg Businessweek USA January 22 2018Dokument76 SeitenBloomberg Businessweek USA January 22 2018Anh ThànhNoch keine Bewertungen

- Bloomberg Businessweek USA September 18 2017Dokument69 SeitenBloomberg Businessweek USA September 18 2017Anh ThànhNoch keine Bewertungen

- Bloomberg Businessweek Europe - March 26 2018Dokument76 SeitenBloomberg Businessweek Europe - March 26 2018Anh ThànhNoch keine Bewertungen

- Bloomberg Businessweek Europe - April 23 2018Dokument76 SeitenBloomberg Businessweek Europe - April 23 2018Anh ThànhNoch keine Bewertungen

- African Business Review December 2017Dokument58 SeitenAfrican Business Review December 2017Anh ThànhNoch keine Bewertungen

- Analyzing Syntax Through Texts: Old, Middle, and Early Modern EnglishDokument222 SeitenAnalyzing Syntax Through Texts: Old, Middle, and Early Modern EnglishAnh Thành100% (1)

- African Review October 2017Dokument70 SeitenAfrican Review October 2017Anh ThànhNoch keine Bewertungen

- Asian Geographic - April 2018Dokument116 SeitenAsian Geographic - April 2018Anh ThànhNoch keine Bewertungen

- Gmail - CFVG, MBA Entrance Examination (April 2018 Session) - Result !Dokument1 SeiteGmail - CFVG, MBA Entrance Examination (April 2018 Session) - Result !Anh ThànhNoch keine Bewertungen

- Module1-MMSS13-CFVG Session 3Dokument70 SeitenModule1-MMSS13-CFVG Session 3Anh ThànhNoch keine Bewertungen

- Module1-MMSS13CFVG The Project PDFDokument10 SeitenModule1-MMSS13CFVG The Project PDFAnh ThànhNoch keine Bewertungen

- BF Tutorial 6 Monopoly PDFDokument5 SeitenBF Tutorial 6 Monopoly PDFAnh ThànhNoch keine Bewertungen

- The Concorde: - A Technological MarvelDokument17 SeitenThe Concorde: - A Technological MarvelAnh ThànhNoch keine Bewertungen

- Module1-MMSS13-CFVG IntroductionDokument22 SeitenModule1-MMSS13-CFVG IntroductionAnh ThànhNoch keine Bewertungen

- BUYER Truck Exercise CFVG BDokument2 SeitenBUYER Truck Exercise CFVG BAnh ThànhNoch keine Bewertungen

- Four Case Studies On CSRDokument24 SeitenFour Case Studies On CSRAnh ThànhNoch keine Bewertungen

- SELLER ROLETruck Exercise CFVGDokument2 SeitenSELLER ROLETruck Exercise CFVGAnh ThànhNoch keine Bewertungen

- BF Tutorial 4 Production and CostsDokument6 SeitenBF Tutorial 4 Production and CostsAnh ThànhNoch keine Bewertungen

- Nike CSR CaseDokument3 SeitenNike CSR CaseAnh ThànhNoch keine Bewertungen

- Unit 1: Financial ManagementDokument20 SeitenUnit 1: Financial ManagementDisha SareenNoch keine Bewertungen

- Stock Market Indices (BBA)Dokument5 SeitenStock Market Indices (BBA)Akshita DhyaniNoch keine Bewertungen

- HDFC Life Brochure-2Dokument7 SeitenHDFC Life Brochure-2Kamal Kannan GNoch keine Bewertungen

- Entrepreneurship Chapter 4 Let The Market Know You BetterDokument82 SeitenEntrepreneurship Chapter 4 Let The Market Know You BetterAhmadNoch keine Bewertungen

- Supply Chain Management: Instruction To CandidatesDokument2 SeitenSupply Chain Management: Instruction To CandidatesAlex MuhweziNoch keine Bewertungen

- Name: Solution Problem: P14-2, Issuance and Retirement of Bonds Course: DateDokument8 SeitenName: Solution Problem: P14-2, Issuance and Retirement of Bonds Course: DateRegina PutriNoch keine Bewertungen

- Chapter 2 - Interest Rates - SDokument117 SeitenChapter 2 - Interest Rates - STuong Vi Nguyen PhanNoch keine Bewertungen

- A Study On Customer Satisfaction Towards Online ShoppingDokument71 SeitenA Study On Customer Satisfaction Towards Online ShoppingAyan Siddiqui100% (1)

- Submitted By: Sumit Mudgil: Course: Digital Business Innovation Project: Hamleys'SDokument7 SeitenSubmitted By: Sumit Mudgil: Course: Digital Business Innovation Project: Hamleys'SSumitNoch keine Bewertungen

- Laudon Traver 3E Chapter2 Final 2Dokument41 SeitenLaudon Traver 3E Chapter2 Final 2নাজমুল হাসান দিনানNoch keine Bewertungen

- The Affective Turn: Political Economy and The Biomediated Body Patricia T. CloughDokument33 SeitenThe Affective Turn: Political Economy and The Biomediated Body Patricia T. CloughtomhamsandwhichNoch keine Bewertungen

- Solution Class 11 - Accountancy Test 1: Cash DiscountDokument4 SeitenSolution Class 11 - Accountancy Test 1: Cash DiscountBHS PRAYAGRAJNoch keine Bewertungen

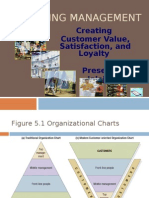

- Customer Value, Satisfaction & LoyaltyDokument27 SeitenCustomer Value, Satisfaction & LoyaltyJalaj Mathur88% (8)

- 2023 HSC Business StudiesDokument22 Seiten2023 HSC Business StudiesSreemoye ChakrabortyNoch keine Bewertungen

- Mamta RSPL Report 2018Dokument96 SeitenMamta RSPL Report 2018nehaNoch keine Bewertungen

- Risk ProfileDokument4 SeitenRisk Profileapi-26441337Noch keine Bewertungen

- Investor Presentation Aug 15 v1Dokument25 SeitenInvestor Presentation Aug 15 v1Bogdan DemkoNoch keine Bewertungen

- Marketing Education Handling Questions Concerns Assessments Answer KeyDokument3 SeitenMarketing Education Handling Questions Concerns Assessments Answer Keykaruna karun100% (1)

- 2021 Global Islamic Fintech Report 2021Dokument56 Seiten2021 Global Islamic Fintech Report 2021Slamet PrayitnoNoch keine Bewertungen

- MCX and Exchange Market For, Chana Palm Oil and Copper:: Presented by - Group 5Dokument18 SeitenMCX and Exchange Market For, Chana Palm Oil and Copper:: Presented by - Group 5Alisha AshishNoch keine Bewertungen

- Inb 372 Sme Case PDFDokument2 SeitenInb 372 Sme Case PDFNameera AlamNoch keine Bewertungen

- Marginal CostingDokument14 SeitenMarginal CostingbrightyNoch keine Bewertungen

- ch17 InvestmentsDokument38 Seitench17 InvestmentsKristine Wali0% (1)

- PROJECT: Joining The Market: Required ResourcesDokument5 SeitenPROJECT: Joining The Market: Required ResourcesAngel Enamorado0% (1)

- Rubber MatDokument1 SeiteRubber MatSUNIL PATELNoch keine Bewertungen

- Engineering Economy: Break-Even AnalysisDokument6 SeitenEngineering Economy: Break-Even AnalysisSheena PascualNoch keine Bewertungen

- Dubey ParleDokument9 SeitenDubey ParleUlhasNoch keine Bewertungen

- Overview of International Business FunctionsDokument54 SeitenOverview of International Business Functionsapi-3727758100% (3)

- VAE (Livestock Economics, Marketing & Bussiness Management TANUVAS)Dokument276 SeitenVAE (Livestock Economics, Marketing & Bussiness Management TANUVAS)Deepak SuraNoch keine Bewertungen

- Cooperative Administration - It Says That For Manufacturer The Effectiveness ofDokument7 SeitenCooperative Administration - It Says That For Manufacturer The Effectiveness ofChristine BrusasNoch keine Bewertungen