Das könnte Ihnen auch gefallen

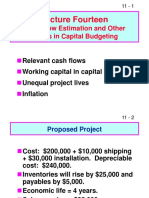

- Lecture Fourteen: Cash Flow Estimation and Other Topics in Capital BudgetingDokument38 SeitenLecture Fourteen: Cash Flow Estimation and Other Topics in Capital BudgetingHồng KhánhNoch keine Bewertungen

- Isna Wirda Lutfiyah - 17 - 4-17Dokument10 SeitenIsna Wirda Lutfiyah - 17 - 4-17DewaSatriaNoch keine Bewertungen

- Year Revenue Cogs Depreciation S&A Taxable Income After-Tax Operating IncomeDokument6 SeitenYear Revenue Cogs Depreciation S&A Taxable Income After-Tax Operating IncomeSpandana AchantaNoch keine Bewertungen

- Essay QuestionsDokument16 SeitenEssay QuestionssheldonNoch keine Bewertungen

- EE - Assignment Chapter 9-10 SolutionDokument11 SeitenEE - Assignment Chapter 9-10 SolutionXuân ThànhNoch keine Bewertungen

- Solution Assignment Chapter 9 10 1Dokument14 SeitenSolution Assignment Chapter 9 10 1Huynh Ng Quynh NhuNoch keine Bewertungen

- Fundamentals of Corporate Finance 7Th Edition Brealey Solutions Manual Full Chapter PDFDokument38 SeitenFundamentals of Corporate Finance 7Th Edition Brealey Solutions Manual Full Chapter PDFcolonizeverseaat100% (10)

- Chapter 12Dokument14 SeitenChapter 12Naimmul FahimNoch keine Bewertungen

- Corporate Finance Solution Chapter 6Dokument9 SeitenCorporate Finance Solution Chapter 6Kunal KumarNoch keine Bewertungen

- SneakerDokument8 SeitenSneakerFelicity YuanNoch keine Bewertungen

- Solution: Year Cash Inflows Present Value Factor Present Value $ @10% $Dokument10 SeitenSolution: Year Cash Inflows Present Value Factor Present Value $ @10% $Waylee CheroNoch keine Bewertungen

- Corporate Finance: Capital BudgetingDokument29 SeitenCorporate Finance: Capital BudgetingPigeons LoftNoch keine Bewertungen

- Dewa Satria Rachman LubisDokument13 SeitenDewa Satria Rachman LubisDewaSatriaNoch keine Bewertungen

- Financial Management 1 CatDokument9 SeitenFinancial Management 1 CatcyrusNoch keine Bewertungen

- Solutions For Capital Budgeting QuestionsDokument7 SeitenSolutions For Capital Budgeting QuestionscaroNoch keine Bewertungen

- Lec 3 After Mid TermDokument11 SeitenLec 3 After Mid TermsherygafaarNoch keine Bewertungen

- GSLC Session 16: Javier Noel Claudio 2301949040 Accounting Technology Corporate Financial Management LB90Dokument6 SeitenGSLC Session 16: Javier Noel Claudio 2301949040 Accounting Technology Corporate Financial Management LB90Javier Noel ClaudioNoch keine Bewertungen

- Tugas GSLC Corp Finance Session 16Dokument6 SeitenTugas GSLC Corp Finance Session 16Javier Noel ClaudioNoch keine Bewertungen

- GSLC Session 16: Javier Noel Claudio 2301949040 Accounting Technology Corporate Financial Management LB90Dokument6 SeitenGSLC Session 16: Javier Noel Claudio 2301949040 Accounting Technology Corporate Financial Management LB90salsabilla rpNoch keine Bewertungen

- Solution CF Cash Flow Practice Problem 2Dokument12 SeitenSolution CF Cash Flow Practice Problem 2Zarieq EricNoch keine Bewertungen

- FM II Assignment 17 Solution 19Dokument3 SeitenFM II Assignment 17 Solution 19RaaziaNoch keine Bewertungen

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions ManualDokument26 SeitenFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manualmisentrynotal6ip1lp100% (16)

- PaybackDokument14 SeitenPaybackHema LathaNoch keine Bewertungen

- Example 5.7Dokument7 SeitenExample 5.7Omar KhalilNoch keine Bewertungen

- Fin Strategy Ass 1Dokument3 SeitenFin Strategy Ass 1mqondisi nkabindeNoch keine Bewertungen

- Solutions To Chapter 8 Using Discounted Cash-Flow Analysis To Make Investment DecisionsDokument12 SeitenSolutions To Chapter 8 Using Discounted Cash-Flow Analysis To Make Investment Decisionshung TranNoch keine Bewertungen

- Cash Flow Brigham SolutionDokument14 SeitenCash Flow Brigham SolutionShahid Mehmood100% (4)

- Solutions To Chapter 9 Using Discounted Cash-Flow Analysis To Make Investment DecisionsDokument16 SeitenSolutions To Chapter 9 Using Discounted Cash-Flow Analysis To Make Investment Decisionsmuhammad ihtishamNoch keine Bewertungen

- CVP Analysis Class Exercise SolutionsDokument4 SeitenCVP Analysis Class Exercise Solutionsaryan bhandariNoch keine Bewertungen

- Corporate Finance Canadian 7th Edition Jaffe Solutions ManualDokument16 SeitenCorporate Finance Canadian 7th Edition Jaffe Solutions Manualtaylorhughesrfnaebgxyk100% (27)

- Capital Budgeting - SolutionDokument5 SeitenCapital Budgeting - SolutionAnchit JassalNoch keine Bewertungen

- PracticeDokument5 SeitenPracticearif khanNoch keine Bewertungen

- Dewa Satria Rachman Lubis - 11 - 4-17Dokument15 SeitenDewa Satria Rachman Lubis - 11 - 4-17DewaSatriaNoch keine Bewertungen

- Topic 8 - Inv App 1 Ans 2019-20Dokument4 SeitenTopic 8 - Inv App 1 Ans 2019-20Gaba RieleNoch keine Bewertungen

- Afm AssignmentDokument17 SeitenAfm AssignmentHabtamuNoch keine Bewertungen

- Acct 3503 Test 2 Format, Instuctions and Review Section A FridayDokument22 SeitenAcct 3503 Test 2 Format, Instuctions and Review Section A Fridayyahye ahmedNoch keine Bewertungen

- FFM 9 Im 12Dokument31 SeitenFFM 9 Im 12Mariel CorderoNoch keine Bewertungen

- Chapter 23Dokument8 SeitenChapter 23Matahari PagiNoch keine Bewertungen

- Handouts 5-6 - Review - Exercises and SolutionsDokument6 SeitenHandouts 5-6 - Review - Exercises and Solutions6kb4nm24vjNoch keine Bewertungen

- Solution ManualDokument12 SeitenSolution ManualReyna BaculioNoch keine Bewertungen

- FM Assaignment Second SemisterDokument9 SeitenFM Assaignment Second SemisterMotuma Abebe100% (1)

- Magsino Hannah Florence Activity 5 Discounted Cash FlowsDokument36 SeitenMagsino Hannah Florence Activity 5 Discounted Cash FlowsKathyrine Claire Edrolin100% (2)

- P1. PRO O.L Solution CMA September 2022 ExaminationDokument6 SeitenP1. PRO O.L Solution CMA September 2022 ExaminationAwal ShekNoch keine Bewertungen

- Financial Management Assignment NotesDokument3 SeitenFinancial Management Assignment NotesDaniyal AliNoch keine Bewertungen

- Chapter 11Dokument10 SeitenChapter 11Syed Sheraz AliNoch keine Bewertungen

- Problem Set 6 (Group 2) Evaluating A Single Project: Guerrero, Leigh Francis - Gc21Dokument5 SeitenProblem Set 6 (Group 2) Evaluating A Single Project: Guerrero, Leigh Francis - Gc21Alexander P Belka0% (1)

- Practice Problems Ch12 PDFDokument57 SeitenPractice Problems Ch12 PDFzoeyNoch keine Bewertungen

- Solution To CVP ProblemsDokument8 SeitenSolution To CVP ProblemsGizachew NadewNoch keine Bewertungen

- Tarea 9.1 Problemas Evaluación Proyectos 1 Loera CoronadoDokument12 SeitenTarea 9.1 Problemas Evaluación Proyectos 1 Loera CoronadoBrandon LoeraNoch keine Bewertungen

- Practice Problems Ch12Dokument57 SeitenPractice Problems Ch12Kevin Baconga100% (2)

- Assignment 3Dokument8 SeitenAssignment 3octoNoch keine Bewertungen

- Cpa Review School of The Philippines: Management Advisory Services AGE OFDokument9 SeitenCpa Review School of The Philippines: Management Advisory Services AGE OFJohn Carlo CruzNoch keine Bewertungen

- Quiz 3Dokument14 SeitenQuiz 3K L YEONoch keine Bewertungen

- Unit 5, 6 & 7 Capital Budgeting 1Dokument14 SeitenUnit 5, 6 & 7 Capital Budgeting 1ankit mehtaNoch keine Bewertungen

- Capital BudgetingDokument14 SeitenCapital BudgetingbhaskkarNoch keine Bewertungen

- Chapter 2 Financial Statements Cash Flow and TaxesDokument7 SeitenChapter 2 Financial Statements Cash Flow and TaxesM. HasanNoch keine Bewertungen

- Econ S-190 Introduction To Financial and Managerial Economics Mock Final Examination 2021 Question #1Dokument6 SeitenEcon S-190 Introduction To Financial and Managerial Economics Mock Final Examination 2021 Question #1ADITYA MUNOTNoch keine Bewertungen

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsVon EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNoch keine Bewertungen

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeVon EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNoch keine Bewertungen

- T10 - Financial Reporting QualityDokument30 SeitenT10 - Financial Reporting QualityJhonatan Perez VillanuevaNoch keine Bewertungen

- Chapter One Cost-Volume-Profit Relationship Variable and Fixed Cost Behavior and PatternsDokument12 SeitenChapter One Cost-Volume-Profit Relationship Variable and Fixed Cost Behavior and PatternsEid AwilNoch keine Bewertungen

- LoanDokument4 SeitenLoanRichard Chinyama Chikeji NjolombaNoch keine Bewertungen

- Prashant Kankal Synopisis FinalDokument12 SeitenPrashant Kankal Synopisis FinalPrashant KankalNoch keine Bewertungen

- Cebu Technological University: Main CampusDokument2 SeitenCebu Technological University: Main CampusLeonard Patrick Faunillan BaynoNoch keine Bewertungen

- Pearson Recommended LinkDokument3 SeitenPearson Recommended LinkHằng ĐỗNoch keine Bewertungen

- Accounting Cycle of A Service BusinessDokument17 SeitenAccounting Cycle of A Service BusinessAmie Jane Miranda100% (1)

- The Philippine IT BPM Industry Roadmap Executive Summary CompressedDokument55 SeitenThe Philippine IT BPM Industry Roadmap Executive Summary Compressedpavanbagade27Noch keine Bewertungen

- BL Portfolio 17.03.2024Dokument12 SeitenBL Portfolio 17.03.2024mjason1Noch keine Bewertungen

- RegistrationDokument9 SeitenRegistrationusman soomroNoch keine Bewertungen

- Silang2018 Audit Report PDFDokument113 SeitenSilang2018 Audit Report PDFLomo LomoNoch keine Bewertungen

- Script - Opportunities in A RecessionDokument4 SeitenScript - Opportunities in A RecessionMayumi AmponNoch keine Bewertungen

- Indonesia Jakarta Rental Apartment Q1 2021Dokument2 SeitenIndonesia Jakarta Rental Apartment Q1 2021Grace SaragihNoch keine Bewertungen

- Undertake Self-Assessment Tests To Discover Your Entrepreneurial TraitsDokument3 SeitenUndertake Self-Assessment Tests To Discover Your Entrepreneurial TraitsTech info MVNoch keine Bewertungen

- Startegic Managemnt Assignment 1Dokument16 SeitenStartegic Managemnt Assignment 1Syeda ZehraNoch keine Bewertungen

- BPO Philippines - Sample Case Study PDFDokument59 SeitenBPO Philippines - Sample Case Study PDFAir0% (1)

- GAP Model On Mac Donald's: Presented by Group No: 3Dokument20 SeitenGAP Model On Mac Donald's: Presented by Group No: 3Dipesh KotechaNoch keine Bewertungen

- GST - Configuration For Vendor Returns ProcessDokument4 SeitenGST - Configuration For Vendor Returns ProcessAnand PrakashNoch keine Bewertungen

- Case TiktokDokument12 SeitenCase TiktokvdrtNoch keine Bewertungen

- Acc206 e ExamDokument8 SeitenAcc206 e Examm2kxcg4gsxNoch keine Bewertungen

- Specification Checklist: Aqa A Level BusinessDokument4 SeitenSpecification Checklist: Aqa A Level BusinessZayna Amelia Khan100% (1)

- Chapter 3 International Financial MarketsDokument93 SeitenChapter 3 International Financial Marketsธชพร พรหมสีดาNoch keine Bewertungen

- James - Internal AuditDokument13 SeitenJames - Internal Auditveblen07Noch keine Bewertungen

- Pre-Test B Course Speaking Lesson 4: Part 1: MarketsDokument9 SeitenPre-Test B Course Speaking Lesson 4: Part 1: MarketsHoàng TùngNoch keine Bewertungen

- Ministry of ICT Strategic-Plan-2023-2027Dokument80 SeitenMinistry of ICT Strategic-Plan-2023-2027Marvin nduko bosireNoch keine Bewertungen

- I. Definition of Agency Cases: Caram v. Laureta, GR No L-28740, 24 February 1981Dokument22 SeitenI. Definition of Agency Cases: Caram v. Laureta, GR No L-28740, 24 February 1981QUEEN NATALIE TUASONNoch keine Bewertungen

- Elemental Realty - Top 10 Real Estate Entrepreneurs - 2020' - Mr. Arun Kumar Aleti, CEODokument1 SeiteElemental Realty - Top 10 Real Estate Entrepreneurs - 2020' - Mr. Arun Kumar Aleti, CEOAkhila AdusumilliNoch keine Bewertungen

- Green Buying Behavior Among Mauritian Consumers: Extending The TPB ModelDokument19 SeitenGreen Buying Behavior Among Mauritian Consumers: Extending The TPB ModelGlobal Research and Development ServicesNoch keine Bewertungen

- Annual ReportDokument42 SeitenAnnual ReportAbdu MohammedNoch keine Bewertungen

- FMR August 2023 Shariah CompliantDokument14 SeitenFMR August 2023 Shariah CompliantAniqa AsgharNoch keine Bewertungen