Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- MT103Dokument2 SeitenMT103Vikrant Singh100% (4)

- Project Report On Indian Banking SystemDokument61 SeitenProject Report On Indian Banking Systemhjghjghj75% (172)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Data Pelaku Pengelolaan InvestasiDokument1.961 SeitenData Pelaku Pengelolaan InvestasiTata Ketet0% (2)

- Geojit Financial Services LTD.,: Pay Slip - July 2019Dokument1 SeiteGeojit Financial Services LTD.,: Pay Slip - July 2019sanjit deyNoch keine Bewertungen

- A Comparative Analysis Between LIC and Private Insurance CompaniesDokument30 SeitenA Comparative Analysis Between LIC and Private Insurance CompaniesDivya Priya60% (15)

- Exam Frequently Asked QuestionsDokument3 SeitenExam Frequently Asked QuestionsArun PrakashNoch keine Bewertungen

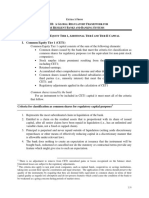

- B Iii: A G R F M R B B S: Common Shares Issued by The BankDokument6 SeitenB Iii: A G R F M R B B S: Common Shares Issued by The BankArun PrakashNoch keine Bewertungen

- RECALLED QUESTIONS (2016-18) : (Ibps Different Banks Promotion Test)Dokument11 SeitenRECALLED QUESTIONS (2016-18) : (Ibps Different Banks Promotion Test)Arun PrakashNoch keine Bewertungen

- University: (Karunya Institute of Technology & Sciences)Dokument5 SeitenUniversity: (Karunya Institute of Technology & Sciences)Arun PrakashNoch keine Bewertungen

- WJR - Walajah Road Junction (2) Railway Station - Today's Train Arrival Timings - India Rail Info - A Busy Junction For Travellers & Rail EnthusiastsDokument2 SeitenWJR - Walajah Road Junction (2) Railway Station - Today's Train Arrival Timings - India Rail Info - A Busy Junction For Travellers & Rail EnthusiastsArun PrakashNoch keine Bewertungen

- GATE 2014 Exam Admit Card: Examination Centre (7071)Dokument1 SeiteGATE 2014 Exam Admit Card: Examination Centre (7071)Arun PrakashNoch keine Bewertungen

- Boorrnn Ttoo Wiinn::: Id Deeaass Ffoorr Wiinnnniinngg Tthhee Ga Am Mee Ooff L LiiffeeDokument4 SeitenBoorrnn Ttoo Wiinn::: Id Deeaass Ffoorr Wiinnnniinngg Tthhee Ga Am Mee Ooff L LiiffeeArun PrakashNoch keine Bewertungen

- A After A Nerve or Muscle Fires During The: Short Period Cell Cannot Respond To Additional StimulationDokument6 SeitenA After A Nerve or Muscle Fires During The: Short Period Cell Cannot Respond To Additional StimulationArun PrakashNoch keine Bewertungen

- State Bank of Travancore Recruitment 2013 1030 Peon Posts Apply OnlineDokument6 SeitenState Bank of Travancore Recruitment 2013 1030 Peon Posts Apply OnlinemalaarunNoch keine Bewertungen

- Banking and InsuranceDokument13 SeitenBanking and InsuranceKiran Kumar50% (2)

- Capital Source 2011 Form 10-KDokument212 SeitenCapital Source 2011 Form 10-KrgaragiolaNoch keine Bewertungen

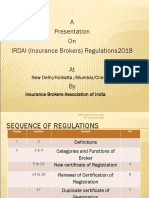

- Brokerregulation 01mar18Dokument79 SeitenBrokerregulation 01mar18Tosheef Allen KropenskiNoch keine Bewertungen

- 51198bos40905 cp4 PDFDokument41 Seiten51198bos40905 cp4 PDFShubham VyasNoch keine Bewertungen

- FORM16Dokument5 SeitenFORM16sunnyjain19900% (1)

- BancassuranceDokument18 SeitenBancassuranceMahipal GadhaviNoch keine Bewertungen

- Research Report On Electronic Banking E-Banking ManagementDokument5 SeitenResearch Report On Electronic Banking E-Banking ManagementshivkmrchauhanNoch keine Bewertungen

- Vicente Go v. Metropolitan Bank and Trust CoDokument3 SeitenVicente Go v. Metropolitan Bank and Trust CoBeatriz VillafuerteNoch keine Bewertungen

- 43 Indian - Capital - MarketDokument40 Seiten43 Indian - Capital - MarketNiladri MondalNoch keine Bewertungen

- Audit of Cash On Hand and in BankDokument2 SeitenAudit of Cash On Hand and in Bankdidiaen100% (1)

- Cooperative SocietyDokument5 SeitenCooperative SocietyGuruprasad PatelNoch keine Bewertungen

- PDFDokument374 SeitenPDFSimbuNoch keine Bewertungen

- Investment Operations Analyst in Chicago IL Resume Michael FreasDokument1 SeiteInvestment Operations Analyst in Chicago IL Resume Michael FreasMichaelFreasNoch keine Bewertungen

- Citi Subsidiarys 2010 Exhibit 21-01Dokument4 SeitenCiti Subsidiarys 2010 Exhibit 21-01CarrieonicNoch keine Bewertungen

- The Recto LawDokument12 SeitenThe Recto LawBrian MannNoch keine Bewertungen

- CM Unit 1.c.2 TYPES of Credit FacilitiesDokument8 SeitenCM Unit 1.c.2 TYPES of Credit Facilitiesabdullahi shafiuNoch keine Bewertungen

- 01 Pob Mock Test 1 Cce EditedDokument19 Seiten01 Pob Mock Test 1 Cce EditedShaik MunnaNoch keine Bewertungen

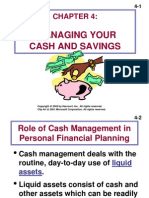

- Managing Your Cash and SavingsDokument11 SeitenManaging Your Cash and SavingsMoi WarheadNoch keine Bewertungen

- TTTDokument6 SeitenTTTAngelika BalmeoNoch keine Bewertungen

- Future GainDokument9 SeitenFuture GainSantosh DasNoch keine Bewertungen

- GR 109666, Republic of The PhilippinesDokument9 SeitenGR 109666, Republic of The PhilippinesIan Lemuel CahindeNoch keine Bewertungen

- IBBL Internship OpportunityDokument6 SeitenIBBL Internship OpportunityTakia FerdousNoch keine Bewertungen

- Your Payment ReceiptDokument1 SeiteYour Payment ReceiptRajat ReddyNoch keine Bewertungen

- New York Times - Looking Back at The Crash of 1929Dokument73 SeitenNew York Times - Looking Back at The Crash of 1929cdromuserNoch keine Bewertungen