Das könnte Ihnen auch gefallen

- Global Currency Reset - Revaluation of Currencies - Historical OverviewDokument20 SeitenGlobal Currency Reset - Revaluation of Currencies - Historical Overviewenerchi111196% (28)

- Chapter 7 Stockholers Equity FinalDokument77 SeitenChapter 7 Stockholers Equity FinalSampanna ShresthaNoch keine Bewertungen

- Iridium WriteupDokument5 SeitenIridium WriteupDaniel Medeiros100% (1)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideVon EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNoch keine Bewertungen

- Statement of Changes in Equity and The Balance SheetDokument19 SeitenStatement of Changes in Equity and The Balance SheetJaspreet GillNoch keine Bewertungen

- Adv Acct CH 6 HoyleDokument76 SeitenAdv Acct CH 6 Hoylewaverider750% (2)

- Dividend Investing 101 Create Long Term Income from DividendsVon EverandDividend Investing 101 Create Long Term Income from DividendsNoch keine Bewertungen

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementVon EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNoch keine Bewertungen

- Problem Set Mod 1Dokument4 SeitenProblem Set Mod 1Lindsay MadeloNoch keine Bewertungen

- 1 ULO 1 To 3 Week 1 To 3 SHE Activities (AK)Dokument10 Seiten1 ULO 1 To 3 Week 1 To 3 SHE Activities (AK)Margaux Phoenix KimilatNoch keine Bewertungen

- Chapter 10 Corporations - Retained Earnings Exercises T3AY2021Dokument6 SeitenChapter 10 Corporations - Retained Earnings Exercises T3AY2021Carl Vincent BarituaNoch keine Bewertungen

- BU8201 Tutorial 1Dokument17 SeitenBU8201 Tutorial 1Li Hui83% (6)

- Final Exam - FA2 (Shareholders Equity) With QuestionsDokument10 SeitenFinal Exam - FA2 (Shareholders Equity) With Questionsjanus lopezNoch keine Bewertungen

- Civil Law Uribe Notes Civ Rev 2Dokument74 SeitenCivil Law Uribe Notes Civ Rev 2Chilzia RojasNoch keine Bewertungen

- Adv Acct CH 6 HoyleDokument76 SeitenAdv Acct CH 6 HoyleFatima AL-SayedNoch keine Bewertungen

- Retained EarningsDokument18 SeitenRetained EarningsAngelie Bancale100% (1)

- Accounting 4 - EPS Title Under 40 CharactersDokument4 SeitenAccounting 4 - EPS Title Under 40 Charactersmaria evangelistaNoch keine Bewertungen

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownVon EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNoch keine Bewertungen

- Accounting for Corporation: Shareholder’s Equity and Retained EarningsDokument9 SeitenAccounting for Corporation: Shareholder’s Equity and Retained EarningsJonalyn Lastimado0% (1)

- Accounting For Intercompany Transactions - FinalDokument15 SeitenAccounting For Intercompany Transactions - FinalEunice WongNoch keine Bewertungen

- Contributed CapitalDokument3 SeitenContributed CapitalCharize YebanNoch keine Bewertungen

- Accounting Chapter 9Dokument7 SeitenAccounting Chapter 9Angelica Faye DuroNoch keine Bewertungen

- CH 11Dokument4 SeitenCH 11pablozhang1226Noch keine Bewertungen

- امتحان الكفاءة الجامعي.شركاتDokument13 Seitenامتحان الكفاءة الجامعي.شركاتديـنـا عادلNoch keine Bewertungen

- Corporate Finance - Fall 2020 - Chapter 19 Practice ProblemsDokument12 SeitenCorporate Finance - Fall 2020 - Chapter 19 Practice ProblemsNgọc Anh HoàngNoch keine Bewertungen

- Chapter 13Dokument11 SeitenChapter 13Maya HamdyNoch keine Bewertungen

- Chapter 17 1Dokument26 SeitenChapter 17 1Diệu Linh NguyễnNoch keine Bewertungen

- Dividends ERDokument11 SeitenDividends ERMarian Salinas DacuroNoch keine Bewertungen

- Statement of Changes in Equity and Balance SheetDokument82 SeitenStatement of Changes in Equity and Balance SheetnicoNoch keine Bewertungen

- Chapter 13 Corporations and Stockholders' EquityDokument23 SeitenChapter 13 Corporations and Stockholders' EquityKiri SorianoNoch keine Bewertungen

- Dividends - and - Share - Repurchases - Basics - SlidesDokument19 SeitenDividends - and - Share - Repurchases - Basics - Slideszaheer9287Noch keine Bewertungen

- Chapter 13 14 Review QuestionsDokument6 SeitenChapter 13 14 Review QuestionsHERSINoch keine Bewertungen

- Michelle G. Miranda Multiple Choice-Dividends and Dividend PolicyDokument4 SeitenMichelle G. Miranda Multiple Choice-Dividends and Dividend PolicyMichelle MirandaNoch keine Bewertungen

- Introduction To Accounting 2 Organization and Capital Stock TransactionsDokument17 SeitenIntroduction To Accounting 2 Organization and Capital Stock Transactionsalice horanNoch keine Bewertungen

- Q2Dokument37 SeitenQ2Hilario, Jana Rizzette C.Noch keine Bewertungen

- Chapter 18 Shareholders Equity - Docx-1Dokument14 SeitenChapter 18 Shareholders Equity - Docx-1kanroji1923Noch keine Bewertungen

- Accounting Capital+Stock+TransactionsDokument17 SeitenAccounting Capital+Stock+TransactionsOckouri BarnesNoch keine Bewertungen

- CFAB Accounting Chapter 11. Company Financial StatementsDokument43 SeitenCFAB Accounting Chapter 11. Company Financial StatementsHuy NguyenNoch keine Bewertungen

- Financial Accounting A Business Process Approach 3Rd Edition Reimers Solutions Manual Full Chapter PDFDokument67 SeitenFinancial Accounting A Business Process Approach 3Rd Edition Reimers Solutions Manual Full Chapter PDFKristieKelleyenfm100% (10)

- Fundamentals of Advanced Accounting 5Th Edition Hoyle Test Bank Full Chapter PDFDokument52 SeitenFundamentals of Advanced Accounting 5Th Edition Hoyle Test Bank Full Chapter PDFDaisyHillyowek100% (10)

- Chapter 18 Shareholders' Equity: Paid-In Capital Fundamental Share RightsDokument9 SeitenChapter 18 Shareholders' Equity: Paid-In Capital Fundamental Share RightsSteeeeeeeephNoch keine Bewertungen

- C450 - Shareholder's Equity - Lecture NotesDokument13 SeitenC450 - Shareholder's Equity - Lecture NotesFreelansirNoch keine Bewertungen

- Libby 4ce Solutions Manual - Ch12Dokument43 SeitenLibby 4ce Solutions Manual - Ch127595522Noch keine Bewertungen

- Fa ch09Dokument47 SeitenFa ch09joannmacalaNoch keine Bewertungen

- Lecture - 9 - Income - and - Equity - NUS ACC1002 2020 SpringDokument43 SeitenLecture - 9 - Income - and - Equity - NUS ACC1002 2020 SpringZenyuiNoch keine Bewertungen

- Chapter 13Dokument13 SeitenChapter 13Mondy MondyNoch keine Bewertungen

- Chapter 15 ExrecisesDokument7 SeitenChapter 15 ExrecisesZain MajaliNoch keine Bewertungen

- Chapter 13 SolutionsDokument45 SeitenChapter 13 Solutionsaboodyuae2000Noch keine Bewertungen

- Acct C.H.10Dokument6 SeitenAcct C.H.10j8noelNoch keine Bewertungen

- Week 05-06-Ch13 Accounting For Corporation-Old PPT-latest UpdateDokument55 SeitenWeek 05-06-Ch13 Accounting For Corporation-Old PPT-latest UpdateziqingyeNoch keine Bewertungen

- Chapter 10 Equity Part 2Dokument27 SeitenChapter 10 Equity Part 2LEE WEI LONGNoch keine Bewertungen

- Principles of Accounting Needles 12th Edition Solutions ManualDokument49 SeitenPrinciples of Accounting Needles 12th Edition Solutions ManualJosephWoodsdbjt100% (40)

- Partial Text 2Dokument7 SeitenPartial Text 2Spring000Noch keine Bewertungen

- AC 306 Class Notes Chapter 15 (Solutions)Dokument13 SeitenAC 306 Class Notes Chapter 15 (Solutions)needforschoolNoch keine Bewertungen

- Stockholders Equity MCQ QuizDokument10 SeitenStockholders Equity MCQ QuizEricka AlimNoch keine Bewertungen

- 1 Which of The Following Are Attributes of A LiabilityDokument1 Seite1 Which of The Following Are Attributes of A LiabilityM Bilal SaleemNoch keine Bewertungen

- TBchap 014Dokument96 SeitenTBchap 014DemianNoch keine Bewertungen

- Final Exams PArCOr 2020Dokument4 SeitenFinal Exams PArCOr 2020John Alfred CastinoNoch keine Bewertungen

- Chapter 1 - Exercises Part ADokument9 SeitenChapter 1 - Exercises Part AHECTOR ORTEGANoch keine Bewertungen

- Accounting For Equity - UpdatedDokument6 SeitenAccounting For Equity - UpdatedLoice MutetiNoch keine Bewertungen

- Corporations CH 12 Lecture 1Dokument18 SeitenCorporations CH 12 Lecture 1Faisal SiddiquiNoch keine Bewertungen

- CFA® Level I - Corporate Finance: Dividends and Share Repurchases: BasicsDokument18 SeitenCFA® Level I - Corporate Finance: Dividends and Share Repurchases: BasicsAbhishek GuptaNoch keine Bewertungen

- Partnership Corp. - Chapter 7Dokument12 SeitenPartnership Corp. - Chapter 7deniseanne clementeNoch keine Bewertungen

- Ch15 UpdatedDokument90 SeitenCh15 Updatedkokmunwai717Noch keine Bewertungen

- Ch15 UpdatedDokument94 SeitenCh15 Updatedkokmunwai717Noch keine Bewertungen

- Bac Elims: Effortless RoundDokument3 SeitenBac Elims: Effortless RoundTracy Miranda BognotNoch keine Bewertungen

- Financial AnalysisDokument12 SeitenFinancial AnalysisShubham BansalNoch keine Bewertungen

- Propertree - Pitch DeckDokument10 SeitenPropertree - Pitch DeckAndi Alfi SyahrinNoch keine Bewertungen

- Life Cycle of A LoanDokument12 SeitenLife Cycle of A LoanSyed Noman AhmedNoch keine Bewertungen

- 2Dokument3 Seiten2Ruth TenajerosNoch keine Bewertungen

- Lazy Lagoon Sarovar Portico Suites: Hotel Confirmation VoucherDokument2 SeitenLazy Lagoon Sarovar Portico Suites: Hotel Confirmation VoucherHimanshu WadaskarNoch keine Bewertungen

- Vizco, Krizia Mae H.Dokument11 SeitenVizco, Krizia Mae H.Meng VizcoNoch keine Bewertungen

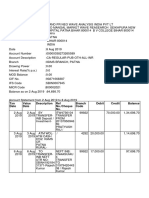

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDokument3 SeitenTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNoch keine Bewertungen

- LMGTRAN Negotiable InstrumentsDokument36 SeitenLMGTRAN Negotiable InstrumentsNastassja Marie DelaCruzNoch keine Bewertungen

- Accounting Principles Question Paper, Answers and Examiners CommentsDokument24 SeitenAccounting Principles Question Paper, Answers and Examiners CommentsRyanNoch keine Bewertungen

- Adding Value in Construction Design Management by Using Simulation ApproachDokument22 SeitenAdding Value in Construction Design Management by Using Simulation ApproachkrmchariNoch keine Bewertungen

- Chapter 6 Mental AccountingDokument6 SeitenChapter 6 Mental AccountingAbdulNoch keine Bewertungen

- Offset Agreement - Wikipedia, The Free EncyclopediaDokument20 SeitenOffset Agreement - Wikipedia, The Free EncyclopedianeerajscribdNoch keine Bewertungen

- Diminishing MusharakahDokument45 SeitenDiminishing MusharakahIbn Bashir Ar-Raisi0% (1)

- Salary, Wage, Income: Business MathematicsDokument20 SeitenSalary, Wage, Income: Business MathematicsNatasha Dela PeñaNoch keine Bewertungen

- Fin QnaDokument4 SeitenFin QnaMayur AgrawalNoch keine Bewertungen

- Advanced Accounting Jeter 5th Edition Solutions ManualDokument37 SeitenAdvanced Accounting Jeter 5th Edition Solutions Manualgordonswansonepe0q100% (9)

- ProjectDokument79 SeitenProjectvishwajit bhoir100% (1)

- Final HBL PresentationDokument75 SeitenFinal HBL PresentationShehzaib Sunny100% (4)

- To Prosperity: From DEBTDokument112 SeitenTo Prosperity: From DEBTمحمد عبدﷲNoch keine Bewertungen

- Elliott WaveDokument7 SeitenElliott WavePetchiramNoch keine Bewertungen

- New Form No 15GDokument4 SeitenNew Form No 15GDevang PatelNoch keine Bewertungen

- M.B.a - Retail ManagementDokument22 SeitenM.B.a - Retail ManagementaarthiNoch keine Bewertungen

- Carolyn Chiu - ResumeDokument2 SeitenCarolyn Chiu - Resumeapi-445104074Noch keine Bewertungen