Das könnte Ihnen auch gefallen

- Leave and License AgreementDokument5 SeitenLeave and License AgreementmohitNoch keine Bewertungen

- Rent Agreement PDFDokument12 SeitenRent Agreement PDFAshish MajithiaNoch keine Bewertungen

- Term & ConditionsDokument2 SeitenTerm & ConditionsRajeev SrivastavaNoch keine Bewertungen

- LLP Incorporation ProcedureDokument3 SeitenLLP Incorporation ProcedureCorproNoch keine Bewertungen

- Financial Results 201920Dokument26 SeitenFinancial Results 201920Ankush AgrawalNoch keine Bewertungen

- GSTN: 19AADFP9388F1ZO Partners DetailsDokument20 SeitenGSTN: 19AADFP9388F1ZO Partners DetailsSOURAV GUPTANoch keine Bewertungen

- GAP AffidavitDokument1 SeiteGAP AffidavitJaidev BhoomreddyNoch keine Bewertungen

- General Terms and ConditionsDokument5 SeitenGeneral Terms and ConditionsAmicus CuriaeNoch keine Bewertungen

- Compliances by Trusts Under MPT ActDokument3 SeitenCompliances by Trusts Under MPT ActCA Nealesh KelkarNoch keine Bewertungen

- GAP CertificateDokument1 SeiteGAP CertificatePratik VaradeNoch keine Bewertungen

- Super Distributor MOU AgreementDokument3 SeitenSuper Distributor MOU AgreementMalay ThakerNoch keine Bewertungen

- Transfer Deed BuilderDokument6 SeitenTransfer Deed BuilderShantanu YewaleNoch keine Bewertungen

- Form B VXL Realtors Pvt. Ltd.Dokument8 SeitenForm B VXL Realtors Pvt. Ltd.Vikram Singh BaidNoch keine Bewertungen

- Axis BK Nri GpaDokument8 SeitenAxis BK Nri Gpashaky1978Noch keine Bewertungen

- Leave and License Agreement-IndiseDokument14 SeitenLeave and License Agreement-Indiserajupuspharaj0Noch keine Bewertungen

- Relinquishment DeedDokument4 SeitenRelinquishment DeedSudesh GoyalNoch keine Bewertungen

- Arihant Associates .: Submitted OnlineDokument7 SeitenArihant Associates .: Submitted OnlineMausam MeshramNoch keine Bewertungen

- Authorization LetterDokument1 SeiteAuthorization LetterEdronn LeeNoch keine Bewertungen

- Final Exam 2009 SolutionsDokument10 SeitenFinal Exam 2009 SolutionsJerryCheungNoch keine Bewertungen

- S. Majumdar & Co.: Patent&Tradcmank AttormcxsDokument14 SeitenS. Majumdar & Co.: Patent&Tradcmank Attormcxsjags jainNoch keine Bewertungen

- Letter of Authorization - TESDADokument2 SeitenLetter of Authorization - TESDARommel Tipaklong CorpuzNoch keine Bewertungen

- PawanDokument8 SeitenPawanindushekharthakurNoch keine Bewertungen

- Agreement For Distributorship MDH DistributorshipDokument5 SeitenAgreement For Distributorship MDH DistributorshipDrv LimtedNoch keine Bewertungen

- My Right To A Funeral (Janazah) by DR Saleh As SalehDokument14 SeitenMy Right To A Funeral (Janazah) by DR Saleh As SalehMountainofknowledgeNoch keine Bewertungen

- Sexual HarassmentDokument31 SeitenSexual HarassmentMegha KochharNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Preventing and Responding To Sexual Harassment at WorkDokument62 SeitenPreventing and Responding To Sexual Harassment at WorkPriyanka JuneNoch keine Bewertungen

- L 22 Hierarchy of Court in IndiaDokument15 SeitenL 22 Hierarchy of Court in IndiaAbhinav JainNoch keine Bewertungen

- Proforma Affidavit App FormDokument9 SeitenProforma Affidavit App Formsamplc2011Noch keine Bewertungen

- Indemnity Cum Declaration Undertaking NOC For PA ClaimsDokument1 SeiteIndemnity Cum Declaration Undertaking NOC For PA Claimssaurav96Noch keine Bewertungen

- Bombay Rent ActDokument101 SeitenBombay Rent ActHANIF S. MULIANoch keine Bewertungen

- Undertaking To Submit Noc, Share Cert., Sale DeedDokument7 SeitenUndertaking To Submit Noc, Share Cert., Sale Deedehsanix31Noch keine Bewertungen

- Statutory Compliance TrackerDokument6 SeitenStatutory Compliance TrackerHemanth KanakamedalaNoch keine Bewertungen

- In The Court of Hon'Ble I Addl. District Judge Ranga Reddy District::At L.B. NagarDokument4 SeitenIn The Court of Hon'Ble I Addl. District Judge Ranga Reddy District::At L.B. NagarJ. Ramu PawarNoch keine Bewertungen

- 1 Draft Hinjewadi Leave and License Agreement 1Dokument14 Seiten1 Draft Hinjewadi Leave and License Agreement 1Anirudh SanNoch keine Bewertungen

- Murtuza Ali Rajkotwala - Court Decision About Bhindibazar RedevelopmentDokument3 SeitenMurtuza Ali Rajkotwala - Court Decision About Bhindibazar RedevelopmentMurtuza Ali RajkotwalaNoch keine Bewertungen

- Minutes of The Third Board Meeting of Aatapi Seva Foundation Held On FridayDokument10 SeitenMinutes of The Third Board Meeting of Aatapi Seva Foundation Held On FridayhirenzNoch keine Bewertungen

- 11 MTHS Leave and License AgreementDokument7 Seiten11 MTHS Leave and License AgreementSherman CarvalhoNoch keine Bewertungen

- Edited - Nestaway Family Agreement PDF - SD-59765 PDFDokument11 SeitenEdited - Nestaway Family Agreement PDF - SD-59765 PDFRajan S PrasadNoch keine Bewertungen

- Declaration Cum UndertakingDokument4 SeitenDeclaration Cum UndertakingMritunjai SinghNoch keine Bewertungen

- Last Will and Testament: OF - SS#Dokument8 SeitenLast Will and Testament: OF - SS#Abdul Jabbar QuraishiNoch keine Bewertungen

- Format of Experience CertificateDokument1 SeiteFormat of Experience CertificateKushal DaimaryNoch keine Bewertungen

- Inter Office MemoDokument2 SeitenInter Office MemoOm BissaNoch keine Bewertungen

- Islamic Last Will and Testament: in The Name of Allah, The Most Gracious, The Most MercifulDokument4 SeitenIslamic Last Will and Testament: in The Name of Allah, The Most Gracious, The Most Mercifulnancyg868Noch keine Bewertungen

- Prohibition of Sexual Harassment at The Workplace - MudsDokument37 SeitenProhibition of Sexual Harassment at The Workplace - MudsShubham RohillaNoch keine Bewertungen

- No: TMR/DELHI/EXM/2020/: Search ReportDokument2 SeitenNo: TMR/DELHI/EXM/2020/: Search ReportRaman MalhotraNoch keine Bewertungen

- LEAVE and License AgreementDokument3 SeitenLEAVE and License Agreementmahesh_rampalliNoch keine Bewertungen

- Contract Advance Payment Guarantee No.Dokument3 SeitenContract Advance Payment Guarantee No.Siddharth Pandey0% (1)

- WILL Tution ShettyDokument4 SeitenWILL Tution ShettyMuni ReddyNoch keine Bewertungen

- Inter-Office MemoDokument1 SeiteInter-Office MemoseeejaneNoch keine Bewertungen

- Agreement For Sale of FlatDokument18 SeitenAgreement For Sale of FlatSamudra MajumderNoch keine Bewertungen

- Checklist of Compliance-Related Actions Under POSH Act-1595431858Dokument5 SeitenChecklist of Compliance-Related Actions Under POSH Act-1595431858Anubhab MukherjeeNoch keine Bewertungen

- Relieving LetterDokument2 SeitenRelieving Letterజయ సింహ కసిరెడ్డి100% (1)

- Leave and License AgreementDokument3 SeitenLeave and License AgreementAjoy Sharma100% (1)

- Good Experience and Reformat For Experiance Leterlieving CertificateDokument3 SeitenGood Experience and Reformat For Experiance Leterlieving CertificateAdoc ConsultancyNoch keine Bewertungen

- DTC Agreement Between China and United KingdomDokument23 SeitenDTC Agreement Between China and United KingdomOECD: Organisation for Economic Co-operation and Development0% (1)

- SLP 33377 of 2012-Nivedita SharmaDokument4 SeitenSLP 33377 of 2012-Nivedita Sharmaaditya singhNoch keine Bewertungen

- Will in Favour of Wife and ChildrenDokument2 SeitenWill in Favour of Wife and Childrenshreya bhattacharjeeNoch keine Bewertungen

- Chapter - 4 Insurance SectorDokument14 SeitenChapter - 4 Insurance SectorMohammad FaizanNoch keine Bewertungen

- Reliance Personal Loan Care Insurance Policy - 2013-2014Dokument24 SeitenReliance Personal Loan Care Insurance Policy - 2013-2014pankhuri.singhNoch keine Bewertungen

- FINAL - Layer Poultry Estate-OrissaDokument5 SeitenFINAL - Layer Poultry Estate-Orissasohalsingh1Noch keine Bewertungen

- Scheme For The Establishment of Backyard Poultry Units For The Year 2018-19Dokument5 SeitenScheme For The Establishment of Backyard Poultry Units For The Year 2018-19sohalsingh1Noch keine Bewertungen

- Networked Backyard Poultry EnterprisesDokument11 SeitenNetworked Backyard Poultry Enterprisessohalsingh1Noch keine Bewertungen

- Networked Backyard Poultry EnterprisesDokument11 SeitenNetworked Backyard Poultry Enterprisessohalsingh1Noch keine Bewertungen

- 2017041117mini Hatcher S. StoryDokument7 Seiten2017041117mini Hatcher S. Storysohalsingh1Noch keine Bewertungen

- Poultry Management GuideDokument7 SeitenPoultry Management Guidesohalsingh1100% (1)

- APICOLDokument1 SeiteAPICOLsohalsingh1Noch keine Bewertungen

- South Sector: Ig/Ss HQ ChennaiDokument11 SeitenSouth Sector: Ig/Ss HQ Chennaisohalsingh1Noch keine Bewertungen

- NABARD Broiler Farming ProjectDokument10 SeitenNABARD Broiler Farming ProjectGrowel Agrovet Private Limited.Noch keine Bewertungen

- Training SectorDokument2 SeitenTraining Sectorsohalsingh1Noch keine Bewertungen

- North East SectorDokument6 SeitenNorth East Sectorsohalsingh1Noch keine Bewertungen

- E-Commerce in India: Legal, Tax and Regulatory AnalysisDokument42 SeitenE-Commerce in India: Legal, Tax and Regulatory Analysissohalsingh1Noch keine Bewertungen

- FINAL - Layer Poultry Estate-OrissaDokument14 SeitenFINAL - Layer Poultry Estate-OrissaSrinivas RaoNoch keine Bewertungen

- Western Sector: 1 Res - Bn. BarwahaDokument9 SeitenWestern Sector: 1 Res - Bn. Barwahasohalsingh1100% (1)

- Melia - Dubia - Konda VepaDokument8 SeitenMelia - Dubia - Konda VepaHeemanshu ShahNoch keine Bewertungen

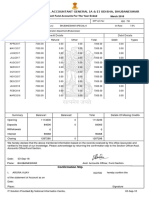

- Office of The Principal Accountant General (A & E) Odisha, BhubaneswarDokument2 SeitenOffice of The Principal Accountant General (A & E) Odisha, Bhubaneswarsohalsingh1Noch keine Bewertungen

- Health Check UpDokument3 SeitenHealth Check Upsohalsingh1Noch keine Bewertungen

- Regional Office, Bhubaneswar: FOR Group Mediclaim Policy FOR Employees OF Psus Under Govt. of OdishaDokument14 SeitenRegional Office, Bhubaneswar: FOR Group Mediclaim Policy FOR Employees OF Psus Under Govt. of Odishasohalsingh1Noch keine Bewertungen

- Registration of Insurance CompanyDokument2 SeitenRegistration of Insurance Companysohalsingh1Noch keine Bewertungen

- Advisory PDFDokument7 SeitenAdvisory PDFsohalsingh1Noch keine Bewertungen

- E-Commerce: A New Tool in Tax EvasionDokument8 SeitenE-Commerce: A New Tool in Tax Evasionsohalsingh1Noch keine Bewertungen

- Heritage StatusDokument1 SeiteHeritage Statussohalsingh1Noch keine Bewertungen

- Nursery Propagation Technique of BagalungaDokument11 SeitenNursery Propagation Technique of Bagalungasohalsingh1Noch keine Bewertungen

- Cyber Law: Bangladesh Perspective: BY: MD Amran Hossain Emcs, Jahangirnagar UniversityDokument7 SeitenCyber Law: Bangladesh Perspective: BY: MD Amran Hossain Emcs, Jahangirnagar Universitysohalsingh1Noch keine Bewertungen

- Beyond Bitcoin: Exploring The Blockchain: Industry Applications and Legal PerspectivesDokument35 SeitenBeyond Bitcoin: Exploring The Blockchain: Industry Applications and Legal Perspectivesshanky22Noch keine Bewertungen

- Sample Letterhead TemplateDokument1 SeiteSample Letterhead Templatebds6Noch keine Bewertungen

- Statement - I Cost of Project Particulars Sl. No. Ref. Annex Total CostDokument15 SeitenStatement - I Cost of Project Particulars Sl. No. Ref. Annex Total Costsohalsingh1Noch keine Bewertungen

- CGHS Rates 2014 - Bhubaneshwar1Dokument44 SeitenCGHS Rates 2014 - Bhubaneshwar1sohalsingh1Noch keine Bewertungen

- Ppe L IstDokument4 SeitenPpe L IstbharatNoch keine Bewertungen

- 1 PDFDokument3 Seiten1 PDFdrzana78Noch keine Bewertungen

- ART Review Interim ReportDokument168 SeitenART Review Interim ReportJill HennessyNoch keine Bewertungen

- Association of Etonogestrel-Releasing Contraceptive Implant With Reduced Weight Gain in An Exclusively Breastfed Infant: Report and Literature ReviewDokument4 SeitenAssociation of Etonogestrel-Releasing Contraceptive Implant With Reduced Weight Gain in An Exclusively Breastfed Infant: Report and Literature ReviewFian FebriantoNoch keine Bewertungen

- Bangalore DR ListDokument11 SeitenBangalore DR Listkrisveli76% (42)

- Daftar PustakaDokument2 SeitenDaftar PustakahaseosamaNoch keine Bewertungen

- Intestinal Obstruction in Pediatric PatientsDokument25 SeitenIntestinal Obstruction in Pediatric PatientsHaryo Priambodo100% (1)

- Complete OPD Schedule For AIIMS RISHIKESH...Dokument5 SeitenComplete OPD Schedule For AIIMS RISHIKESH...Razat Saini100% (2)

- Emergency RadiologyDokument231 SeitenEmergency RadiologyNina Amelia60% (5)

- Medical Terms (Prefixes Suffixes Roots)Dokument5 SeitenMedical Terms (Prefixes Suffixes Roots)David Donovan ManuelNoch keine Bewertungen

- Bibliography For Ch. "Ophthalmology": Last Updated: May 9, 2019Dokument2 SeitenBibliography For Ch. "Ophthalmology": Last Updated: May 9, 2019Okami PNoch keine Bewertungen

- Cross-Covering The Well Baby Nursery and Pedi-Med Service: Intensive Care Nursery House Staff ManualDokument5 SeitenCross-Covering The Well Baby Nursery and Pedi-Med Service: Intensive Care Nursery House Staff ManualSedaka DonaldsonNoch keine Bewertungen

- Facial (Sex Act)Dokument5 SeitenFacial (Sex Act)nathanNoch keine Bewertungen

- Biometry by Suryakant Jha and Wangchuk Doma PDFDokument5 SeitenBiometry by Suryakant Jha and Wangchuk Doma PDFJavier Andrés Pinochet SantoroNoch keine Bewertungen

- Mineralocorticoids: Shajeer. SDokument42 SeitenMineralocorticoids: Shajeer. SShajeer SalimNoch keine Bewertungen

- Jurnal Internasional PDFDokument7 SeitenJurnal Internasional PDFShella GustiawatiNoch keine Bewertungen

- Mayo ClinicDokument338 SeitenMayo Clinicrajkumarss87Noch keine Bewertungen

- Nle - High-Risk PregnancyDokument113 SeitenNle - High-Risk Pregnancytachycardia01Noch keine Bewertungen

- Diagnosing Anemia in Neonates An Evidence-Based ApproachDokument13 SeitenDiagnosing Anemia in Neonates An Evidence-Based Approacharmando salvador100% (1)

- Final Quiz PHI6 PDFDokument5 SeitenFinal Quiz PHI6 PDFKenneth DayritNoch keine Bewertungen

- HypospadiasDokument12 SeitenHypospadiasLeni LukmanNoch keine Bewertungen

- HIPEC ProtocolDokument7 SeitenHIPEC ProtocolMariaNoch keine Bewertungen

- Management of Second-Stage LaborDokument34 SeitenManagement of Second-Stage LaborAshwini TirkeyNoch keine Bewertungen

- Supersize Me EssayDokument5 SeitenSupersize Me EssayBrooke Cohn0% (1)

- PG Prospectus July 2013 PDFDokument45 SeitenPG Prospectus July 2013 PDFSoman PillaiNoch keine Bewertungen

- Semester 2 MLT Log BookDokument10 SeitenSemester 2 MLT Log Bookzeeshizeeshe0% (2)

- Medical Terminology: Liliana SugihartoDokument10 SeitenMedical Terminology: Liliana SugihartointanwidaNoch keine Bewertungen

- Eng Philosophy and Model of Midwifery CareDokument4 SeitenEng Philosophy and Model of Midwifery CareJefrioSuyantoNoch keine Bewertungen

- Pharmacology Iii PracticalDokument16 SeitenPharmacology Iii Practicaldoremon nobitaNoch keine Bewertungen

- Ashley Odenbach Resume 9-2019Dokument2 SeitenAshley Odenbach Resume 9-2019api-491453387Noch keine Bewertungen