Das könnte Ihnen auch gefallen

- Financial Accounting Theory and Practice Vol 1Dokument1 SeiteFinancial Accounting Theory and Practice Vol 1Jessa BasarteNoch keine Bewertungen

- 16 Standard Costingx PDFDokument92 Seiten16 Standard Costingx PDFJessa Basarte40% (5)

- PSA-620 Using The Work of An Auditor's ExpertDokument19 SeitenPSA-620 Using The Work of An Auditor's ExpertcolleenyuNoch keine Bewertungen

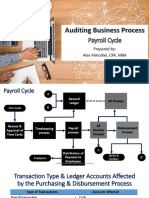

- Auditing Payroll Process PDFDokument12 SeitenAuditing Payroll Process PDFJessa BasarteNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Cambridge Latin Course Book I Vocabulary Stage 1 Stage 2Dokument3 SeitenCambridge Latin Course Book I Vocabulary Stage 1 Stage 2Aden BanksNoch keine Bewertungen

- Leverage My PptsDokument34 SeitenLeverage My PptsMadhuram SharmaNoch keine Bewertungen

- Flexural Design of Fiber-Reinforced Concrete Soranakom Mobasher 106-m52Dokument10 SeitenFlexural Design of Fiber-Reinforced Concrete Soranakom Mobasher 106-m52Premalatha JeyaramNoch keine Bewertungen

- Fouts Federal LawsuitDokument28 SeitenFouts Federal LawsuitWXYZ-TV DetroitNoch keine Bewertungen

- A Guide To Conducting A Systematic Literature Review ofDokument51 SeitenA Guide To Conducting A Systematic Literature Review ofDarryl WallaceNoch keine Bewertungen

- Khutbah About The QuranDokument3 SeitenKhutbah About The QurantakwaniaNoch keine Bewertungen

- Overpressure Prediction From PS Seismic DataDokument10 SeitenOverpressure Prediction From PS Seismic DataSevinj HumbatovaNoch keine Bewertungen

- Meditation On God's WordDokument26 SeitenMeditation On God's WordBeghin BoseNoch keine Bewertungen

- G.R. No. 201354 September 21, 2016Dokument11 SeitenG.R. No. 201354 September 21, 2016Winston YutaNoch keine Bewertungen

- AMBROSE PINTO-Caste - Discrimination - and - UNDokument3 SeitenAMBROSE PINTO-Caste - Discrimination - and - UNKlv SwamyNoch keine Bewertungen

- Failure of Composite Materials PDFDokument2 SeitenFailure of Composite Materials PDFPatrickNoch keine Bewertungen

- Chapter 101-160Dokument297 SeitenChapter 101-160Dipankar BoruahNoch keine Bewertungen

- Marriage and Divorce Conflicts in The International PerspectiveDokument33 SeitenMarriage and Divorce Conflicts in The International PerspectiveAnjani kumarNoch keine Bewertungen

- Case Study Method: Dr. Rana Singh MBA (Gold Medalist), Ph. D. 98 11 828 987Dokument33 SeitenCase Study Method: Dr. Rana Singh MBA (Gold Medalist), Ph. D. 98 11 828 987Belur BaxiNoch keine Bewertungen

- Rousseau NotesDokument4 SeitenRousseau NotesAkhilesh IssurNoch keine Bewertungen

- Noorul Islam Centre For Higher Education Noorul Islam University, Kumaracoil M.E. Biomedical Instrumentation Curriculum & Syllabus Semester IDokument26 SeitenNoorul Islam Centre For Higher Education Noorul Islam University, Kumaracoil M.E. Biomedical Instrumentation Curriculum & Syllabus Semester Iisaac RNoch keine Bewertungen

- ElectionDokument127 SeitenElectionRaviKumar50% (2)

- LESSON 6 Perfect TensesDokument4 SeitenLESSON 6 Perfect TensesAULINO JÚLIONoch keine Bewertungen

- 17PME328E: Process Planning and Cost EstimationDokument48 Seiten17PME328E: Process Planning and Cost EstimationDeepak MisraNoch keine Bewertungen

- Kuo SzuYu 2014 PHD ThesisDokument261 SeitenKuo SzuYu 2014 PHD ThesiskatandeNoch keine Bewertungen

- Clayton Parks and Recreation: Youth Soccer Coaching ManualDokument19 SeitenClayton Parks and Recreation: Youth Soccer Coaching ManualFranklin Justniano VacaNoch keine Bewertungen

- BASICS of Process ControlDokument31 SeitenBASICS of Process ControlMallikarjun ManjunathNoch keine Bewertungen

- PREETI and RahulDokument22 SeitenPREETI and Rahulnitinkhandelwal2911Noch keine Bewertungen

- Checkpoint PhysicsDokument12 SeitenCheckpoint PhysicsRishika Bafna100% (1)

- Educational Psychology EDU-202 Spring - 2022 Dr. Fouad Yehya: Fyehya@aust - Edu.lbDokument31 SeitenEducational Psychology EDU-202 Spring - 2022 Dr. Fouad Yehya: Fyehya@aust - Edu.lbLayla Al KhatibNoch keine Bewertungen

- FP010CALL Trabajo CO Ardila Jaime Molina PiñeyroDokument12 SeitenFP010CALL Trabajo CO Ardila Jaime Molina PiñeyroRomina Paola PiñeyroNoch keine Bewertungen

- Subculture of Football HooligansDokument9 SeitenSubculture of Football HooligansCristi BerdeaNoch keine Bewertungen

- Effect of Boron Content On Hot Ductility and Hot Cracking TIG 316L SSDokument10 SeitenEffect of Boron Content On Hot Ductility and Hot Cracking TIG 316L SSafnene1Noch keine Bewertungen

- LP.-Habitat-of-Animals Lesson PlanDokument4 SeitenLP.-Habitat-of-Animals Lesson PlanL LawlietNoch keine Bewertungen

- Iver Brevik, Olesya Gorbunova and Diego Saez-Gomez - Casimir Effects Near The Big Rip Singularity in Viscous CosmologyDokument7 SeitenIver Brevik, Olesya Gorbunova and Diego Saez-Gomez - Casimir Effects Near The Big Rip Singularity in Viscous CosmologyDex30KMNoch keine Bewertungen